FATCA XML Schema v2.0 User Guide

2

Table of Contents

What’s New .................................................................................................................. 6

1 Introduction ............................................................................................................ 7

About FATCA ................................................................................................................................ 7 1.1

Special Rules for Non-GIIN Filers ................................................................................................. 8 1.2

HCTA Filers ................................................................................................................................... 8 1.3

Purpose ......................................................................................................................................... 9 1.4

2 FATCA XML Schema Overview .......................................................................... 10

Schema Versions ........................................................................................................................ 12 2.1

Schema Validation ...................................................................................................................... 13 2.2

2.2.1 Creating New Reports using Schema v2.0 ......................................................................... 13

2.2.2 Corrected, Void and Amended Reports using Schema v2.0 .............................................. 13

Prohibited and Restricted Characters ......................................................................................... 14 2.3

Namespace ................................................................................................................................. 15 2.4

Reciprocal Exchange .................................................................................................................. 15 2.5

2.5.1 Competent Authority Requests (CAR) ................................................................................ 16

Data Preparation and Naming Conventions ............................................................................... 16 2.6

System Testing ............................................................................................................................ 16 2.7

Other Resources ......................................................................................................................... 17 2.8

3 MessageSpec ...................................................................................................... 18

SendingCompanyIN .................................................................................................................... 19 3.1

TransmittingCountry .................................................................................................................... 19 3.1

ReceivingCountry ........................................................................................................................ 20 3.2

MessageType .............................................................................................................................. 20 3.3

Warning ....................................................................................................................................... 20 3.4

Contact ........................................................................................................................................ 20 3.5

MessageRefId ............................................................................................................................. 20 3.6

CorrMessageRefId ...................................................................................................................... 21 3.7

ReportingPeriod .......................................................................................................................... 21 3.8

Timestamp ................................................................................................................................... 21 3.9

4 FATCA Report Complex Types ........................................................................... 22

MonAmnt_Type ........................................................................................................................... 22 4.1

DocSpec_Type ............................................................................................................................ 23 4.2

4.2.1 DocTypeIndic ...................................................................................................................... 23

FATCA XML Schema v2.0 User Guide

3

4.2.2 DocRefId ............................................................................................................................. 25

4.2.3 CorrMessageRefId .............................................................................................................. 25

4.2.4 CorrDocRefId ...................................................................................................................... 26

Address_Type ............................................................................................................................. 26

4.3

4.3.1 CountryCode ....................................................................................................................... 27

4.3.2 Address Free ....................................................................................................................... 27

4.3.3 AddressFix .......................................................................................................................... 28

PersonParty_Type ....................................................................................................................... 29 4.4

4.4.1 ResCountryCode ................................................................................................................. 29

4.4.2 TIN ....................................................................................................................................... 30

4.4.3 Name ................................................................................................................................... 31

Titles ................................................................................................................................ 32 4.4.3.1

First Name ....................................................................................................................... 32 4.4.3.2

Middle Name ................................................................................................................... 32 4.4.3.3

Last Name ....................................................................................................................... 33 4.4.3.4

4.4.4 Nationality ............................................................................................................................ 33

4.4.5 BirthInfo ............................................................................................................................... 33

BirthDate ......................................................................................................................... 34 4.4.5.1

OrganisationParty_Type .............................................................................................................. 35 4.5

4.5.1 ResCountryCode ................................................................................................................. 35

4.5.2 TIN ....................................................................................................................................... 36

4.5.3 Name ................................................................................................................................... 37

4.5.4 Address ............................................................................................................................... 37

CorrectableReportOrganisation_Type ........................................................................................ 37 4.6

4.6.1 FilerCategory - New ............................................................................................................ 38

4.6.2 DocSpec .............................................................................................................................. 39

5 ReportingFI .......................................................................................................... 40

6 ReportingGroup ................................................................................................... 43

Sponsor ....................................................................................................................................... 43 6.1

Intermediary ................................................................................................................................ 44 6.2

NilReport - New ........................................................................................................................... 45 6.3

6.3.1 DocSpec .............................................................................................................................. 46

6.3.2 NoAccountToReport ............................................................................................................ 46

Account Report ............................................................................................................................ 47 6.4

6.4.1 DocSpec .............................................................................................................................. 48

FATCA XML Schema v2.0 User Guide

4

6.4.2 AccountNumber ................................................................................................................... 48

6.4.3 AccountClosed - New .......................................................................................................... 49

6.4.4 AccountHolder ..................................................................................................................... 50

Individual ......................................................................................................................... 50

6.4.4.1

Organisation .................................................................................................................... 50 6.4.4.2

AcctHolderType - Updated .............................................................................................. 51 6.4.4.3

6.4.5 Substantial Owner - Updated .............................................................................................. 52

Individual and Organization ............................................................................................. 52 6.4.5.1

6.4.6 AccountBalance .................................................................................................................. 53

6.4.7 Payment .............................................................................................................................. 54

Type ................................................................................................................................ 55 6.4.7.1

PaymentTypeDesc - New ............................................................................................... 55 6.4.7.2

PaymentAmt .................................................................................................................... 56 6.4.7.3

6.4.8 CARRef - New (Model 2 IGA Reporting Only) .................................................................... 56

PoolReportReportingFIGIIN ............................................................................................ 57 6.4.8.1

PoolReportMessageRefId ............................................................................................... 57 6.4.8.2

PoolReportDocRefId ....................................................................................................... 57 6.4.8.3

6.4.9 AdditionalData - New .......................................................................................................... 58

AdditionalItem .................................................................................................................. 58 6.4.9.1

Pool Report ................................................................................................................................. 59 6.5

6.5.1 DocSpec .............................................................................................................................. 59

6.5.2 AccountCount - Update ....................................................................................................... 59

6.5.3 AccountPoolReportType - Updated .................................................................................... 60

6.5.4 PoolBalance ........................................................................................................................ 60

7 Correcting, Amending and Voiding Records - New ............................................. 61

Unique MessageRefId and DocRefId ......................................................................................... 61 7.1

How to Correct, Amend or Void Records .................................................................................... 62 7.2

7.2.1 Amend ................................................................................................................................. 63

7.2.2 Void ..................................................................................................................................... 63

7.2.3 Correct ................................................................................................................................. 63

7.2.4 Special Cases to Amend and Correct Records .................................................................. 63

MessageSpec and DocSpec ....................................................................................................... 64 7.3

Appendix A: Glossary of Terms ............................................................................... 66

Appendix B: FATCA XML Schema Overview ........................................................... 71

Appendix C: MessageSpec ..................................................................................... 72

FATCA XML Schema v2.0 User Guide

5

Appendix D: Reporting FI ........................................................................................ 73

Appendix E: Reporting Group ................................................................................. 74

Appendix F: Account Report ................................................................................... 75

Appendix G: Pool Report ......................................................................................... 76

Appendix H: Account Holder ................................................................................... 77

Appendix I: Substantial Owner ............................................................................... 78

Appendix J: Sponsor & Intermediary ...................................................................... 79

Appendix K: Individual or Organization Account Holders ........................................ 80

Appendix L: Person Party Type .............................................................................. 81

Appendix M: Address Type ...................................................................................... 82

Appendix N: OrganisationParty_Type ..................................................................... 83

Appendix O: CorrectableReportOrganisationParty_Type ........................................ 84

Appendix P: DocSpec_Type ................................................................................... 85

FATCA XML Schema v2.0 User Guide

6

What’s New

This section highlights important changes to the Foreign Account Tax Compliance Act (FATCA) XML

Schema v2.0 User Guide. The schema and business rules are explained in detail throughout this

publication. All changes are effective January 17, 2017 and the IRS will communicate the specific

transition date as soon as possible.

Future Updates

The IRS will continue to consult with partners and receive feedback to improve the guide.

Data Elements

Description

AccountClosed

Allows a financial institution to declare the account status as

closed.

Account Holder Type

Update to the FATCA account holder type enumeration

codes.

Account Number Type

Allows a financial institution to declare account number

formats, such as IBAN and OSIN.

AdditionalData

Provides additional text information for an account report.

CARRef

Links account reports submitted in response to a Competent

Authority Request (CAR) to the original pooled report from a

financial institution from a Model 2 IGA jurisdiction.

(For Model 2 reporting only)

FilerCategory

Identifies the filer category code for a reporting financial

institution and/or sponsor.

NilReport

Indicates a reporting financial institution has no accounts to

report.

Payment Type Description

Provides text description for payment types.

Substantial Owner

Allows a filer to name a substantial owner as an entity or

organization.

FATCA XML Schema v2.0 User Guide

7

1 Introduction

About FATCA 1.1

The Foreign Account Tax Compliance Act (FATCA) was enacted as part of the Hire Incentives to Restore

Employment (HIRE) Act in 2010. FATCA was created to address non-reporting of income related to

foreign financial accounts held by US taxpayers. FATCA requires certain foreign financial institutions

(FFIs) to report certain information about its U.S. accounts, accounts held by owner-documented FFIs

(ODFFI), and certain aggregate information concerning accounts held by recalcitrant account holders

and, for 2015 and 2016, accounts held by nonparticipating FFIs. Generally, FFIs will commit to this

reporting requirement by registering with the IRS and signing an agreement with the IRS.

The FATCA regulations also require a withholding agent to deduct and withhold tax equal to 30 percent of

a withholdable payment made to a passive non-financial foreign entity (NFFE) unless the passive NFFE

certifies to the withholding agent that it does not have any substantial U.S. owners or provides certain

identifying information with respect to its substantial U.S. owners. A withholding agent is also required to

report information about substantial U.S. owners of a passive NFFE and specified U.S. persons holding

certain equity or debt interests in a payee that the withholding agent has agreed to treat as an ODFFI.

Payments to NFFEs that report their substantial U.S. owners (or report that they have no substantial U.S.

owners) directly to the IRS (direct reporting NFFEs) are excepted from withholding and reporting by a

withholding agent or an FFI.

To facilitate FATCA implementation for FIs operating in jurisdictions with laws that prevent the FIs from

complying with the terms of the FFI agreement, the Treasury Department developed two alternative

model intergovernmental agreements (IGAs) (Model 1 IGA and Model 2 IGA) that allow FIs operating in

such jurisdictions to perform due diligence and reporting on their account holders to achieve the

objectives of FATCA. FFIs reporting under a Model 1 IGA (reporting Model 1 FFIs) report certain

information about their U.S. reportable accounts and certain payees as required under the applicable IGA

to their respective tax authorities. Reporting Model 1 FFIs do not report directly to the IRS. However,

certain reporting Model 1 FFIs in a “Model 1 Option 2” jurisdiction may use the schema to report to their

tax authorities. FFIs reporting under a Model 2 IGA (Reporting Model 2 FFIs) report directly to the IRS

certain information about their U.S. accounts, and certain aggregate information concerning account

holders who do not waive legal restrictions for the FFI to report this information (non-consenting U.S.

accounts), and, for 2015 and 2016, certain payments made to accounts held by nonparticipating FFIs as

required under the applicable IGA and the regulations.

Trustee-Documented Trusts subject to a Model 2 IGA are reported by the trustee of the Trustee-

Documented Trust. A Sponsoring Entity reports on behalf of Sponsored FFIs and Sponsored Direct

Reporting NFFEs.

For the latest information about legislative and tax law topics covered in this publication, go to

www.irs.gov/FATCA.

FATCA XML Schema v2.0 User Guide

8

Special Rules for Non-GIIN Filers 1.2

An approved financial institution (FI) (other than a limited FFI or a limited branch), direct reporting NFFE,

or sponsoring entity that registers with the IRS under FATCA will receive a global intermediary

identification number (GIIN). There are certain entities that are permitted to use IDES to file on behalf of

others that may not register to obtain a GIIN (non-GIIN filers) such as:

U.S. withholding agents (USWA)

Territory financial institutions (TFI) treated as U.S. persons

Third party preparers

Commercial software vendors

A non-GIIN filer must obtain a FATCA Identification Number (FIN) in order to enroll in the International

Data Exchange Service (IDES) for FATCA reporting.

The GIIN and FIN appear on the FFI list published by the IRS on the first day of each month. As a best

practice, always review the published FFI list before submitting a file. The publication of a FIN on the FFI

list does not change the filer’s status for FATCA purposes, as it does not make the filer an FFI and does

not serve any function related to withholding tax on payments under FATCA. A FIN will be accompanied

by a generic name (e.g., “U.S. Withholding Agents 1”) on the FFI list.. For more information on FINs, go to

the FATCA Identification Number (FIN) enrollment page at

https://www.irs.gov/businesses/corporations/finenrollment-process.

HCTA Filers 1.3

The HCTA of a Model 1 IGA jurisdiction uses the schema to report to the IRS certain information on U.S.

Reportable Accounts (as defined in the applicable IGA) of reporting Model 1 FFIs covered by the IGA

and, for 2015 and 2016, information with respect to nonparticipating FFIs that receive payments from

reporting Model 1 FFIs.

If a Model 1 IGA jurisdiction has elected to allow reporting Model 1 FFIs in its jurisdiction to use IDES to

report to the IRS (“Model 1 Option 2”), the reporting Model 1 FFI transmits data directly to its HCTA using

the schema. The HCTA approves or rejects the reports; if approved, the HCTA releases the data to the

IRS.

FATCA XML Schema v2.0 User Guide

9

Purpose 1.4

The FATCA XML Schema v2.0 User Guide (Publication 5124) outlines the business and validation rules

to support a Form 8966, FATCA Report filed electronically through the International Data Exchange

Service (IDES). There are reporting differences between filing electronically and filing in paper format with

the IRS. To file a paper Form 8966 please see the filing instructions at www.irs.gov/pub/irs-pdf/f8966.pdf.

All IDES users should be familiar with FATCA regulations, Extensible Markup Language (XML) and the

FATCA XML schemas. These guidelines should be used in conjunction with the most current version of

other FATCA resources and are available on www.irs.gov:

FATCA Online Registration:

Publication 5118

FATCA Online Registration User Guide

Provides instructions to complete the online FATCA Online Registration

System or electronic Form 8957, FATCA Registration

Publication 5147

FFI List Search and Download Tool User Guide

Provides instructions on how to use the FFI List Search and Download Tool to

search for approved GIINs and FINs

FATCA Reporting (IDES, data preparation, transmission and messages):

Publication 5190

FATCA IDES User Guide

Provides instructions on how to use the International Data Exchange Service

to transmit FATCA reporting data

Publication 5188

FATCA Metadata XML Schema v1.1 User Guide

Explains the XML schema and data elements used in the FATCA metadata file

Publication 5189

International Compliance Management Model (ICMM) User Guide

Explains the schema and business rules of a FATCA notification

Publication 5216

International Compliance Management Model (ICMM) Notification XML

Schema

Explains the XML schema and data elements of a FATCA notification

Form 8966

Form 8966, FATCA Report and form instructions.

Provides instructions on how to file paper format with the IRS

Data Security:

Publication 4557

Safeguarding Taxpayer Data: A Guide for Your Business

Provides information on legal requirements to safeguard taxpayer data

Publication 4600

Safeguarding Taxpayer Information Quick Reference Guide for Businesses

Provides information on data safeguard techniques and how to report data

security incidents

Table 1 – FATCA related resources

FATCA XML Schema v2.0 User Guide

10

2 FATCA XML Schema Overview

The FATCA XML schema governs the structure and content of files that define the electronic format for

Form 8966, FATCA Report. It is used to create reports that conform to recommended standards and

provide first level schema validation. The FATCA XML schema is based on an existing reporting schema

and business requirements used by the Organisation for Economic Co-operation and Development

(OECD) and the European Union (EU).

Diagram

Namespace

urn:oecd:ties:fatca:v2

Type

ftc:Fatca_Type

Properties

minOcc

1

maxOcc

unbounded

content

complex

Table 2 – FATCA XML schema overview

The FATCA XML schema v2.0 takes precedence over any information presented in the guide. All schema

and sample files can be viewed with an XML tool, such as XML Notepad. For more information on the

schema library structure, samples and other resources, go to

https://www.irs.gov/Businesses/Corporations/FATCA-XML-Schemas-and-Business-Rules-for-Form-8966.

FATCA XML Schema v2.0 User Guide

11

General terms in the schema are described by the definition, attribute, and constraints as listed below:

Items

Description

Attribute

An attribute describes additional data related to a specific element. If

blank, then there are no associated attributes.

Cardinality

The number of times an element occurs in an XML file.

The ability to repeat information within the schema is the electronic

equivalent of attaching additional forms when there is insufficient space on

the form to include all of the information that must be filed.

If cardinality is not defined, then one and only one instance should be

included (minOccurs=1 and maxOccurs=1).

Where a data element is not used, then the associated attribute(s) are not

used.

Data Type

The data type or classification of a data element value, such as numeric,

string,

Boolean, or time.

XML supports custom data types and inheritance.

Element

XML data elements defined in the FATCA XML schema; elements not

described in the guide are not supported in the schema.

Encoding

The UTF-8 encoding standard must be used in all XML messages. FATCA

XML schema does not support other encoding schemes, such as UTF-16

and UTF-32.

The Latin (extended) character set commonly used in international

communication should be used.

Message

The term message refers to an XML instance based on the FATCA XML

schema.

Namespace/Prefix

XML namespaces provide a simple method for qualifying element and

attribute names used in XML documents by associating it with

namespaces identified by URI references.

A prefix is associated with a namespace in namespace declaration. It can

be used to qualify element s and/or attributes defined under the

namespace. For more information, go to Section 2.4.Namespace.

Requirement:

The requirement column indicates whether the element is required at the

schema level or application level and must be included in the XML file.

Size/Pattern

The minimum and/or maximum character size of the element value.

If size is not defined, assume a limitation default of 200 characters.

FATCA XML Schema v2.0 User Guide

12

Terms used throughout this guide:

Description

The definitions for the message set or element.

Choice

The choice element allows only one of the elements in the <choice>

declaration to be present within the containing element.

In the schema requirement column, “Choice” indicates the element as one

of the options that can be selected when creating an XML file.

File

A file is a collection of reports transmitted to the receiving jurisdiction. A file

may contain one or many records.

Mandatory

The data element is not used for schema validation but is mandatory for

FATCA reporting.

The data element will pass schema validation, but will fail application level

validation if not present.

Null

The data element is not used for FATCA reporting and may be completed

or omitted. If the element is omitted it will not cause an error notification

Optional

The data element is not required for schema validation or FATCA

reporting but may be provided if available.

The use of an optional field may be subject to an intergovernmental

agreement (IGA), and in some scenarios, may be mandatory for application

level validation. For more information consult your local tax authority.

Record

A single Nil Report, Account Report or Pool Report is equivalent to one

paper Form 8966. A record includes information on the ReportingFI,

Sponsor or Intermediary (if any), “No accounts to report” statement in a Nil

Report or the account data in an AccountReport or PoolReport element.

Report

A group of records assembled into a single XML instance may contain one

or many records.

Required

The data element is required for schema validation and must be included

in the XML file; if not included the file will fail schema validation.

A requirement may be enforced on the schema and/or application level.

Table 3 – FATCA schema terms and descriptions

Schema Versions 2.1

The version of the schema and the corresponding business rules have a unique version number assigned

that consists of two numbers separated by a period sign: major and minor version. The version is

identified by the version attribute on the schema element. The target namespace of the FATCA schema

contains only the major version.

FATCA XML Schema v2.0 User Guide

13

Figure 1 – Schema namespaces

The root element FATCA_OECD version attribute in the XML report file must be set to the value of the

schema version. This will identify the schema version that was used to create the report.

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

FATCA_OECD

version

Max 10

sfa:StringMax10_Type

Required

Schema Validation 2.2

All FATCA XML files should be validated by the sender using FATCA XML Schema v2.0 to identify

potential error conditions before the file is transmitted through IDES. After the file is transmitted and

passes security checks, the FATCA XML file goes through two levels of validation. The first level is for

schema validation and if the file does not pass, it will be rejected. The second level is for application and

business rule validation for data elements; if the file does not pass, you will receive an error notification.

2.2.1 Creating New Reports using Schema v2.0

The XML schema version 2.0 will support FATCA reporting for the current and all previous tax years. The

schema version 2.0 is generally not backward compatible with schema version 1.1. The IRS requires

filers use schema v2.0 for FATCA reporting. A data file formatted using schema v1.1 will not validate

against schema v2.0 and will not pass application validation.

2.2.2 Corrected, Void and Amended Reports using Schema v2.0

Data files created with schema v1.1 can be corrected, voided or amended using schema v2.0. Pool

Reports should not be included in FATCA Report if the pool contains zero accounts. Any file will an empty

pool report will not be validated against schema v2.0. If a Pool report with zero accounts was previously

included in error, the IRS will not require you to void the report. In case additional accounts for the pool

report are discovered later, a new Pool report can be submitted.

Example: In November 2016, a user submits Report2015 and receives a notification to correct record

level errors within 120 days. In February 2017, the user should make all corrections using XML schema

version 2.0.

FATCA XML Schema v2.0 User Guide

14

Prohibited and Restricted Characters 2.3

All XML data files should conform to recommended XML schema best practices. Certain special

characters and patterns are prohibited and if included will cause the file to reject the transmission and

generate an error notification.

Non-Optional Entity Reference

If an XML document contains one of these characters in the XML text content, the data packet will be

rejected and generate an error notification (XML not well-formed). The characters are not allowed by XML

syntax rules and must be replaced with the following predefined entity references. To prevent error

notifications, do not include any of these characters in the XML documents.

Characters

Descriptions

Character

Allowed

Allowed

Entity Reference

&

Ampersand

Rejected

&

<

Less Than

Rejected

<

Table 4 - Non-Optional entity references

Optional Entity Reference

If an XML document contains one of these characters in the XML text content, the use is not restricted by

XML syntax rules. The characters can be replaced by the following predefined entity references to

conform to XML schema best practices.

Characters

Descriptions

Character

Allowed

Replace

Entity Reference

>

Greater Than

Allowed

>

‘

Apostrophe*

Allowed

'

"

Quotation Mark

Allowed

"

Table 5 - Optional entity reference

Note: In all cases, additional pattern matching may be performed on special characters that are directly

followed by a known SQL command and the combination will trigger threat detection and a file level error

notification.

SQL Injection Validation

If an XML document contains one of the following combinations of characters in the XML text content, the

data packet will be rejected and generate a failed threat detection error notification. To prevent error

notifications, do not include any of the combinations of characters.

FATCA XML Schema v2.0 User Guide

15

Characters

Descriptions

Entity Reference

--

Doubled Dash

N/A

/*

Slash Asterisk

N/A

&#

Ampersand Hash

N/A

Table 6 - SQL injection validation

DocRefId and MessageRefId Character Sets

The StringMax200_Type data type is used to define several data elements, such as MessageRefId,

CorrMessageRefId, DocRefId, and CorrDocRefId. A value with a character string not exceeding 200

characters will validate against the schema v2.0. However, the IRS strongly recommends that all

characters in these elements conform to the following:

Upper or lower case letters (“a-z”, “A-Z”)

Numerals (“0-9”)

Special characters including plus (“+”), underscore (“_”), hyphen/dash (“-“), and period (“.”).

Namespace 2.4

The FATCA XML schema v2.0 uses namespaces based on OECD common reporting standards. The

following namespaces are defined:

Prefix

Namespace

Description

sfa

xmlns:sfa="urn:oecd:ties:stffatcatypes:v2

Referenced by the main schema. Defines

common data types specific for FATCA based

on OECD Standard Transmission Format

(STF).

ftc

xmlns:ftc="urn:oecd:ties:fatca:v2

Target FATCA namespace that contains

FATCA data types and data elements.

iso

xmlns:iso="urn:oecd:ties:isofatcatypes:v1

Referenced by the main schema and provides

country codes defined in ISO 3166-1 and ISO

4217 standards.

stf

xmlns:stf="urn:oecd:ties:stf:v4

Contains OECD STF data types.

Table 7 - Namespace and prefix list

Reciprocal Exchange 2.5

The IRS will participate in exchange of information with certain foreign tax administrations under a

bilateral Model 1 IGA. The reciprocal report schema format, encryption method and data preparation are

the same procedures used for FATCA reporting transmission during the applicable tax year. For

additional information, refer to your U.S. Competent Authority Agreement.

FATCA XML Schema v2.0 User Guide

16

2.5.1 Competent Authority Requests (CAR)

The IRS may send U.S. Competent Authority requests to Model 2 HCTAs in response to pooled reports

from reporting Model 2 FFIs on non-consenting U.S. accounts and nonparticipating FFIs. An HCTA that

receives a U.S. Competent Authority request through IDES should use the schema to send the requested

information to the IRS.

Data Preparation and Naming Conventions 2.6

There are specific data preparation guidelines on how to structure and package data files. Filers are

responsible for completing the FATCA XML file as specified by FATCA regulations, IRS forms and

applicable IGAs. During the data preparation process, you should provide information that conforms to

the current schema while also complying by applicable business rules. All recommended file names are

case sensitive and any variation in encryption method, name, extension or format may cause a

transmission failure. For more information on IDES, go to Publication 5190. The IDES User Guide. There

are several online resources to help you prepare and submit a valid FATCA XML document:

Description

Location

Data preparation software sample code

.NET

Java

OpenSSL

UNIX

https://github.com/IRSgov

IDES data preparation summary and sample

files

https://www.irs.gov/Businesses/Corporations/ID

ES-Data-Transmission-and-File-Preparation

Table 8 - IDES data preparation resources

System Testing 2.7

Each year the IRS reviews any new FATCA legal requirements and improvements to assess the impact

on IRS forms and processing procedures. These changes determine updates to the XML schemas and

business rules. IRS notifies all users of schema changes in the testing and production environments.

All enrolled users are eligible to participate during testing. All filers must enroll in IDES with a valid IRS-

issued GIIN, FIN or HCTA Entity ID/username, and a valid certificate. Filers are strongly encouraged to

update their software and to test any schema changes. The test environment configurations may not be

identical to the production system. For more information, go to

https://www.irs.gov/Businesses/Corporations/IDES-Testing-Schedule.

FATCA XML Schema v2.0 User Guide

17

Other Resources 2.8

The FATCA Global IT Forum provides monthly updates on major developments. Technical experts are

available to your answer questions and discuss various topics. The IRS distributes information to FATCA

partners through the FATCA Newsletter. Subscribers receive communications regarding known issues,

processing delays and early notification of upcoming testing sessions. Sign up on the subscription page

at https://www.irs.gov/individuals/international-taxpayers/subscribe-to-the-fatca-news-and-information-list.

For assistance with transmission error notifications, go to the instructions contained in the notification or

visit https://www.irs.gov/businesses/corporations/irs-fatca-report-notifications. You may also provide

feedback on the quality of this publication and submit comments through the IDES FAQ webpage.

FATCA XML Schema v2.0 User Guide

18

3 MessageSpec

The MessageSpec identifies the financial institution (FI), host country tax authority (TA or HCTA) and

non-GIIN filers sending a message. It contains unique message identifiers, references corrected

messages and specifies the date created, calendar year and reporting period.

Diagram

Namespace

urn:oecd:ties:fatca:v2

Type

sfa:MessageSpec_Type

Properties

content complex

Table 9 – MessageSpec

FATCA XML Schema v2.0 User Guide

19

SendingCompanyIN 3.1

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

SendingCompanyIN

19-characters

GIIN format

sfa:StringMax200_Type

Optional

Mandatory

This data element identifies the sender’s 19-character identifying number.

If the sender is an FI, Sponsoring Entity or direct reporting NFFE, enter the assigned GIIN with

appropriate punctuation (period or decimal). The field is mandatory and the report will not be

accepted without a valid IRS-approved GIIN. Example: 98Q96B.00000.LE.250

If the sender is an HCTA, enter the HCTA FATCA Entity ID in GIIN format.

Example: 000000.00000.TA.250.

If the sender is a non-GIIN filer, enter the FATCA Identification Number (FIN). The FIN is entered

in the message header for filing purposes only. Do not use a FIN under FATCA data elements in

the body of the report.

TransmittingCountry 3.1

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

TransmittingCountry

2 characters

iso:CountryCode_Type

Required

This data element identifies the tax jurisdiction as a 2-character alphabetic country code specified in the

ISO 3166-1 Alpha 2 standard. Example: MX (Mexico) or Germany (DE).

If the sender is a HCTA, enter the country code for the jurisdiction of the tax authority.

If the sender is an FI, enter the country code for the jurisdiction where the reporting FI maintained

the reportable financial accounts. Example: The sender is an FI established in Jurisdiction A and

operates branches in Jurisdiction B. The reported financial accounts are maintained by the FI at

its branch in Jurisdiction B. The TransmittingCountry is Jurisdiction B, the jurisdiction where the FI

maintains the reported account.

If the sender is a direct reporting NFFE, enter the country code for the jurisdiction of residence of

the NFFE.

If the sender is a Sponsoring Entity, enter the country code for the jurisdiction where the

Sponsored FFI maintains the account or the jurisdiction where the Sponsored Direct Reporting

NFFE is resident.

If the sender is a withholding agent, enter the country code for the jurisdiction of residence of the

payer.

FATCA XML Schema v2.0 User Guide

20

ReceivingCountry 3.2

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

ReceivingCountry

2 characters

iso:CountryCode_Type

Required

This data element identifies the jurisdiction of the receiving entities’ tax administration (TA) and uses the

2-character alphabetic country code specified in the ISO 3166-1 Alpha 2 standard. Example: When you

send a FATCA Report to the IRS, the receiving country will always be “US” (United States).

MessageType 3.3

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

MessageType

5 characters

sfa:MessageType_EnumType

Required

This data element specifies contents of the message type. The element is an enumeration and the only

value is “FATCA”.

Warning 3.4

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Warning

Max 4000

sfa:StringMax4000_Type

Optional

This data element is a free text field for input of specific cautionary instructions about use of the message

content. The field is not required for FATCA reporting and may be omitted.

Contact 3.5

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Contact

Max 200

sfa:StringMax200_Type

Optional

Null

This data element is a free text field for input of specific contact information for the sender. The field is not

used for FATCA reporting and may be omitted.

MessageRefId 3.6

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

MessageRefId

Max 200

sfa:StringMax200_Type

Required

This data element is a free text field to capture the unique identifier number for the sender’s message. It

allows both the sender and receiver to identify and correlate a specific message. The MessageRefId is

created by the sender and must be unique across all FATCA XML files received from the entity identified

FATCA XML Schema v2.0 User Guide

21

in the SendingCompanyIN element. The IRS strongly recommends using a Globally Unique Identifier

(GUID) to help ensure uniqueness of assigned MessageRefId values.

CorrMessageRefId

3.7

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

CorrMessageRefId

Max 200

sfa:StringMax200_Type

Optional

This data element is a free text field to capture the unique identifier of a previously filed report. It is used

to reference the original message when sending a corrected, amended or voided report. It allows the

sender and the receiver to identify and correlate a specific message.

When revising a file, it must reference the previous MessageRefId created for the previous message.

MessageSpec can contain multiple CorrMessageRefId elements. If the file contains corrections for

records from multiple previous files, include the CorMessageRefId element for each original file. Files with

new data (FATCA1) should not contain CorrMessageRefId element. For more information, go to Section

7. Correcting, Amending or Voiding Records.

ReportingPeriod 3.8

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

ReportingPeriod

xsd:date

Required

This data element identifies the reporting year for the current message in YYYY-MM-DD format. Do not

enter future years. Example: If reporting information for accounts or payments made in 2017, enter value

as “2017-12-31”.

Timestamp 3.9

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Timestamp

xsd:dateTime

Required

This data element identifies the date and time the message was created and may be automatically

populated by the host system. The format is YYYY- MM-DD’T’hh:mm:ss and fractions of seconds are not

used. Example: 2017-03-15T09:45:30.

FATCA XML Schema v2.0 User Guide

22

4 FATCA Report Complex Types

FATCA complex types are used to define the content of different elements and attributes in several

structures. The structure of the components and schema validation are the same; however, different

business rules or application requirements may apply based on the filing scenario. These complex types

are used in different parts of the schema.

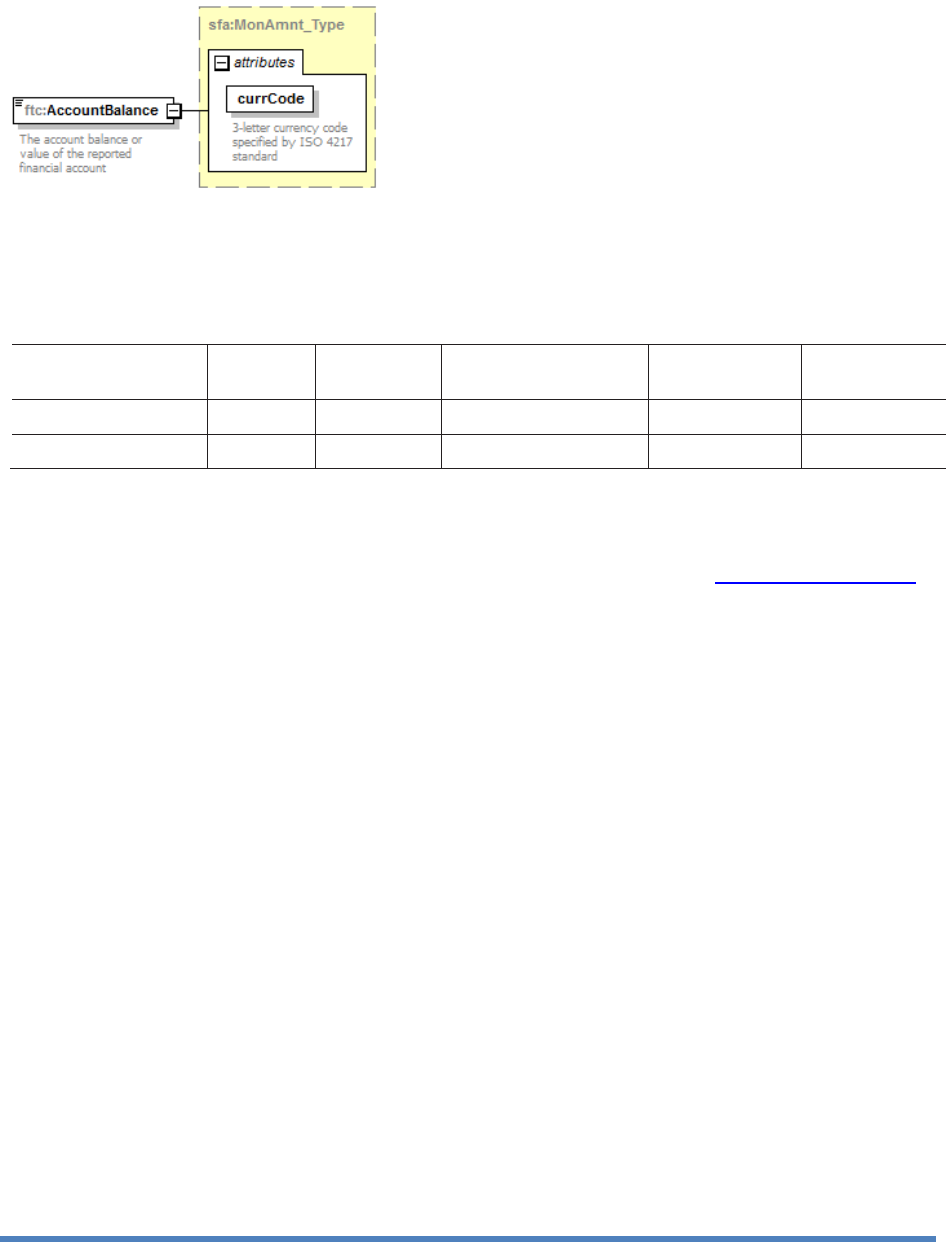

MonAmnt_Type 4.1

Figure 2 - MonAmnt_Type element

DataType

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

MonAmnt_Type

sfa:TwoDigFract_Type

Required

MonAmnt_Type

currCode

iso:currCode_Type

Required

This data type is used to report payments and balances. It allows 2-digit fractional amount in the reported

currency. All amounts must use the currCode attribute, valid three-character ISO 4217 currency code. If

the amounts are not reported in U.S. dollars, enter the code for the reported currency. For amounts in

dollars use the “USD” currency code. For example, fifty-thousand US dollars should be entered as

“50000.00” or “50000 with “USD” currency code attribute.

FATCA XML Schema v2.0 User Guide

23

DocSpec_Type 4.2

Figure 3 - DocSpec_Type

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

DocSpec

ftc:DocSpec_Type

Required

DocSpec_Type is the complex datatype for the DocSpec element. It uniquely identifies the data element,

the type of data, references the record being corrected, amended or voided and associates each record

to a report. The element allows you to manage record level error handling on previously filed reports and

update a specific part of a record without resending an entire report.

The DocSpec element is included in all correctable elements, such as CorrectableAccountReport and

CorrectableNilReport. For more information on how to correct, amend or void a record, go to Section 7.2.

How to Amend, Correct and Void a Record.

Note: A record consists of data on the ReportingFI, Sponsor or Intermediary (if any), plus the account

information from a NilReport or AccountReport or PoolReport.

4.2.1 DocTypeIndic

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

DocTypeIndic

ftc:FatcaDocTypeIndic_EnumType

Required

This data element specifies the type of data being submitted, such as new data or test data. As a best

practice, a message should contain only one DocTypeIndic in a single transmission. Do not combine new,

corrected, void and amended records or any combination within the same message. As a best practice,

send a separate XML file for each type of data.

Application Requirement: The DocTypeIndic codes FATCA11-14 must only be used during testing periods

in the testing environment and must not be used for FATCA reporting to the production environment. The

IRS will notify all users of open testing sessions. Failure to adhere to this restriction will result in f a file

level error notification. For more information on testing, go to Section 2.7 System Testing.

FATCA XML Schema v2.0 User Guide

24

DocTypeIndic

Data Type Description

Production Environment – Use FATCA 1, 2, 3 or 4

FATCA1

New Data

Indicates new records sent to the IRS that has not been previously

processed or voided.

FATCA2

Corrected

Data

Indicates corrected records re-transmitted after the sender received a

record level error notification.

Use FATCA2 in response to a record-level error notification to correct

data. It should not be used in response to file-level errors (Notifications

N1 through N4).

FATCA3

Void Data

Indicates previously filed records that should be voided. To void a

record:

CorrDocRefId and CorrMessageRefId must match the original.

All data fields must match or have the same values as the

original.

Use FATCA3 to void the original transmission.

As a best practice to manage error handling, the following record-level

error notifications require the sender to (1) void the original record as

FATCA3 and then (2) submit new data as FATCA1:

No TIN of Account Holder or Substantial US Owner

Incorrect TIN of Account Holder or Substantial US Owner

Incorrect Name of Account Holder or Substantial US Owner

Incorrect Name and Address for Account Holder or Substantial

US Owner

Note: FATCA3 must match the original record

In addition, certain IGA jurisdictions require the following errors to be

voided:

No TIN or Date of Birth of Individual Account Holder or

Substantial US Owner.

No TIN and Incorrect Date of Birth Individual Account Holder or

Substantial US Owner

See Section 4.4.5 BirthInfo.

FATCA4

Amended

Data

Indicates previously filed records contained errors that should be

replaced or amended. Use FATCA4 if you determine a record that you

previously filed needs to be updated. Do not use in response to an

error notification.

Testing Environment – Use FATCA 11,12,13 or 14

FATCA11

New Test

Similar to FATCA1 and indicates test data.

FATCA12

Corrected

Test

Similar to FATCA2 and indicates test data.

FATCA13

Void Test

Similar to FATCA3 and indicates test data.

FATCA14

Amended

Test

Similar to FATCA4 and indicates test data.

Table 10 - DocTypeIndic enumerated codes

FATCA XML Schema v2.0 User Guide

25

4.2.2 DocRefId

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

DocRefId

Min 21 characters

Max 200 characters

sfa:StringMax200_Type

Required

This data element is an identifier for a specific record and must be unique across all reporting systems

and reporting periods. A unique DocRefId must be generated for each Nil Report or Account Report or

Pool Report and each Reporting FI, Sponsor and Intermediary (if any). The DocRefId cannot be reused

within the scope of FATCA reporting. A message with an invalid or duplicate DocRefId will cause an error

notification. For more information on how to enter a TIN in GIIN format, go to Section 4.4.2

PersonParty_Type TIN or Section 4.5.2 OrganisationParty_Type TIN.

DocRefId Format

The DocRefId data element must conform to recommended best practices for file format and contain a

minimum of 21 characters that include:

Reporting FI GIIN: The GIIN for the reporting FI associated with the reporting group. Some filers

may use a TIN in GIIN format and include an additional zero, such as 123456.78900.SL.840.

Period character: (.)

Unique Value: The value for the referenced record that is unique within the reporting FI for all

time.

Recommended globally unique identifier (GUID).

Example: S519K4.99999.SL.392.12291cc2-37cb-42a9-ad74-06bb5746b60b

4.2.3 CorrMessageRefId

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

CorrMessageRefId

Min 1 char

sfa:StringMin1Max200_Type

Optional

This data element identifies a message that contained a record to be voided, amended or corrected. It

references the MessageRefId from a previously filed report and ensures the proper records are updated.

The value must match the MessageRefId from the MessageSpec element. The CorrMessageRefId

element is used in combination with DocTypeIndic codes, FATCA2, FATCA3 or FATCA4 (or FATCA12,

FATCA13, FATCA14, if test data). Note: Do not use CorrMessageRefId when submitting new data

(FATCA1).

19-character GIIN

format

Unique value

Period (.)

FATCA XML Schema v2.0 User Guide

26

4.2.4 CorrDocRefId

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

CorrDocRefID

Min 1 char

sfa: StringMin1Max200_Type

Optional

This data element identifies a record to be voided, amended or corrected. It references the DocRefId from

a previously filed report and ensures the proper records are updated. The value must match the

DocRefId. The CorrDocRefId element is used in combination with DocTypeIndic codes, FATCA2,

FATCA3 or FATCA4 (or FATCA12, FATCA13, FATCA14, if test data). Note: Do not use CorrDocRefId

when submitting new data (FATCA1).

Address_Type 4.3

The Address_Type allows free text input of the address for any individual or organization included in the

report (e.g., reporting FI, account holder, substantial owner). There are two available options,

AddressFree or AddressFix with supplemental optional AddressFree.

AddressFix should be used for all FATCA reporting; however, you may select AddressFree to enter the

data in a less structured format.

Diagram

Namespace

urn:oecd:ties:stffatcatypes:v2

Type

sfa:Address_Type

Properties

minOcc

1

maxOcc

unbounded

content

complex

Table 11 - Address_Type

FATCA XML Schema v2.0 User Guide

27

The OECDLegalAddressType_EnumType datatype for an address indicates the legal character of that

address as residential or business. The attribute is not used for FATCA reporting and may be omitted.

Value

Description

OECD301

Residential or Business

OECD302

Residential

OECD303

Business

OECD304

Registered Office

OECD305

Unspecified

4.3.1 CountryCode

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

CountryCode

2 characters

iso:CountryCode_Type

Required

This data element provides the country code associated with the address. The country code is a 2-

character alphabetic country code specified in the ISO 3166-1 Alpha 2 standard.

4.3.2 Address Free

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

AddressFree

Max 4000

sfa:StringMax4000_Type

Optional

This data element allows free text input of the address for the individual or organization. AddressFree

should only be used if the data cannot be presented in the AddressFix format and the sender cannot

define the various parts of the address.

The address shall be presented as one string of bytes, blank, slash (/) or carriage return line feed

used as a delimiter between parts of the address.

AddressFree can be used as a supplemental element after the AddresFix element and when the

AdressFix format is selected for address.

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Address

sfa:Address_Type

Required

AddressType

legalAddressType

stf:OECDLegalAddressType_

EnumType

Optional

Null

FATCA XML Schema v2.0 User Guide

28

4.3.3 AddressFix

Figure 4 – AddressFix element

This data element allows input in fixed format for the address for the individual or organization.

In AddressFix element, enter the address and if additional information is needed, use the

supplemental AddressFree element. In this case, the city, subentity, and postal code information

should be entered in the appropriate data elements.

All elements are optional, except the City element which is required for schema validation.

Element(s)

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Street

sfa:StringMax200_Type

Optional

BuildingIdentifier

sfa:StringMax200_Type

Optional

SuiteIdentifier

sfa:StringMax200_Type

Optional

FloorIdentifier

sfa:StringMax200_Type

Optional

DistrictName

sfa:StringMax200_Type

Optional

POB

sfa:StringMax200_Type

Optional

PostCode

sfa:StringMax200_Type

Optional

City

sfa:StringMax200_Type

Required

CountrySubentity

sfa:StringMax200_Type

Optional

FATCA XML Schema v2.0 User Guide

29

PersonParty_Type 4.4

The PersonParty_Type is a correctable party type that identifies the account holder or substantial owner

that is a natural person. The Name and Address data elements are mandatory. The business rules and

structure of each subelement may be defined elsewhere in the schema. For more information, review

Section 6.4.4.2. AccountHolder – OrganisationParty_Type.

Diagram

Namespace

urn:oecd:ties:stffatcatypes:v2

Used by

elements

AccountHolder_Type/Individual

SubstantialOwner_Type/Individual

Table 12 - PersonParty_Type

4.4.1 ResCountryCode

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

ResCountryCode

2-characters

iso:CountryCode_Type

Optional

This data element describes the tax residence country code for the reported individual account holder or

substantial owner. The country code is a 2-character alphabetic country code specified in the ISO 3166-

1 Alpha 2 standard.

FATCA XML Schema v2.0 User Guide

30

4.4.2 TIN

Figure 5 - TIN - PersonParty

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

TIN

Min 1 char

sfa:TIN_Type

Optional

Mandatory

TIN

issuedBy

2-digit

iso:CountryCode_Type

Optional

This data element identifies the U.S. Tax Identification Number (TIN) for the individual account holder or

substantial owner and the attribute identifies the jurisdiction that issued the TIN. A U.S. TIN may be a

U.S. social security number (SSN) or an individual taxpayer identification number (ITIN) issued by the

IRS. For FATCA reporting a blank issuedBy attribute field will be assumed to indicate the issuing

jurisdiction is the United States (US). For detailed information on TIN values and organisations, go to

Section 4.5.2 OrganisationParty_Type TIN.

TIN Format

A value for a TIN data element must be either in a GIIN format or in one of the following formats for a

US TIN:

Nine consecutive digits without hyphens or other separators (e.g., 123456789)

Nine digits with two hyphens (e.g., 123-45-6789)

Nine digits with a hyphen entered after the second digit (e.g., 12-3456789)

Note: If the TIN field is omitted or the value is not in a valid format, the system will generate a record level

error notification.

Direct Reporting NFFE

If the filer is a direct reporting NFFE the TIN element under the AccountHolder element should be

omitted.

FATCA XML Schema v2.0 User Guide

31

4.4.3 Name

Diagram

Namespace

urn:oecd:ties:stffatcatypes:v2

Type

sfa:NamePerson_Type

Properties

minOcc

1

maxOcc

unbounded

content

complex

Table 13 – Name

This data element contains the components to identify an individual by name. The FirstName and

LastName elements are mandatory and cannot be omitted. The attribute nameType is not used for

FATCA reporting and should be omitted.

FATCA XML Schema v2.0 User Guide

32

Titles 4.4.3.1

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

NamePerson_Type

nameType

stf:OECDNameType_Enum

Type

Optional

Null

PrecedingTitle

sfa:StringMax200_Type

Optional

Null

Title

sfa:StringMax200_Type

Optional

Null

NamePrefix

sfa:StringMax200_Type

Optional

Null

NamePrefix

xnlNameType

sfa:StringMax200_Type

Optional

Null

GenerationIdentifier

sfa:StringMax200_Type

Optional

Null

Suffix

sfa:StringMax200_Type

Optional

Null

GeneralSuffix

sfa:StringMax200_Type

Optional

Null

These data elements and attributes are not required for FATCA and may be omitted; however if included

will not cause an error notification.

First Name 4.4.3.2

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

FirstName

sfa:StringMax200_Type

Required

FirstName

xnlNameType

sfa:StringMax200_Type

Optional

Null

This data element allows for the individual’s first name. It is required for FATCA reporting and cannot be

omitted.

If the sender does not have complete information or no first name for an individual account holder or

substantial owner, you may use an initial here, such J.T. or enter “NFN” (No First Name). The attribute

xnlNameType is not required for FATCA reporting and may be omitted.

Middle Name 4.4.3.3

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

MiddleName

sfa:StringMax200_Type

Optional

MiddleName

xnlNameType

sfa:StringMax200_Type

Optional

Null

This data element allows for the individual’s middle name. If the account holder or substantial owner has

a middle name or initial it may be included. The data is optional and the attribute xnlNameType is not

used for FATCA and may be omitted.

FATCA XML Schema v2.0 User Guide

33

Last Name 4.4.3.4

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

LastName

sfa:StringMax200_Type

Required

LastName

xnlNameType

sfa:StringMax200_Type

Optional

Null

This data element allows for the individual’s last name. This field may include any prefix or suffix legally

used by the account holder or substantial owner. This element is required for FATCA reporting and

cannot be omitted. The xnlNameType attribute is not used for FATCA reporting and may be omitted.

4.4.4 Nationality

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Nationality

2-digit

iso:CountryCode_Type

Optional

Null

This data element is not required for FATCA and may be omitted.

4.4.5 BirthInfo

This data element identifies the date of birth of the individual account holder or substantial owner and

may be used by HCTA and tax administrations that are permitted to provide date of birth information in

lieu of a TIN for the account holder or substantial owner of a preexisting account, in circumstances

described in an applicable IGA.

Diagram

Namespace

urn:oecd:ties:sfafatcatypes:v2

Properties

minOcc

0

maxOcc

1

content

complex

Table 14 – BirthInfo

FATCA XML Schema v2.0 User Guide

34

BirthDate 4.4.5.1

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

BirthDate

xsd:date

Optional

This data element is used only when the message sender is another tax administration that is permitted

to provide a date of birth in lieu of a TIN for a preexisting account under an applicable IGA. It may be

omitted if the tax administration has not received date of birth information from the financial institution or if

a US TIN (if the sender is an HCTA) or a foreign TIN (for reciprocal reports) is provided for the account

holder or substantial owner. The data format is YYYY-MM-DD.

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

City

sfa:StringMax200_Type

Optional

Null

CitySubentity

sfa:StringMax200_Type

Optional

Null

CountryInfo

sfa:StringMax200_Type

Optional

Null

CountryCode

2-characters

iso:CountryCode_Type

Optional

Null

FormerCountryName

sfa:StringMax200_Type

Optional

Null

The data elements above identify the account holder’s place of birth.

The CountryInfo data element

provides a choice between the current country (identified by 2-character country code or a former country

(identified by name). The elements are not used for

FATCA reporting and should be omitted; however, if

included will not cause an error notification.

FATCA XML Schema v2.0 User Guide

35

OrganisationParty_Type 4.5

The OrganisationParty_Type identifies information about any entity included in the report (e.g., an entity

account holder or payee, an entity substantial owner, Reporting FI, Sponsor and Intermediary (if any)).

The Name and Address data elements are required components and each can be presented more than

once. One or more identifiers, such as the TIN, should be added as well as a residence country code.

The element has been extended by adding two categories. The structures of the sub-elements are

described Section 4.6. CorrectableReportOrganisation_Type.

Diagram

Namespace

urn:oecd:ties:stffatcatypes:v2

Used by

elements

AccountHolder_Type/Organisation

SubstantialOwner_Type/Organisation

complexType

CorrectableReportOrganisation_Type

Table 15 - OrganisationParty_Type

4.5.1 ResCountryCode

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

ResCountryCode

2-digit

iso:CountryCode_Type

Optional

This data element describes the tax residence country code for the organization. The country code is a 2-

character alphabetic country code specified in the ISO 3166-1 Alpha 2 standard.

FATCA XML Schema v2.0 User Guide

36

4.5.2 TIN

Figure 6 - TIN - OrganisationParty

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

TIN

Min 1 char

sfa:TIN_Type

Optional

Mandatory

TIN

issuedBy

2-digit

iso:CountryCode_Type

Optional

This element identifies the receiving tax administration or U.S. Tax Identification Number (TIN) for the

organization. The attribute describes the jurisdiction that issued the TIN and reporting a blank issuedBy

attribute field indicates the issuing jurisdiction is the United States (US). The data element can be

repeated if a second TIN is present.

Based on the IGA and FI filing scenarios certain business rules may apply. See Sections 5, 6.1, 6.2,

6.4.4.2.1, and 6.4.5 for the applicable business rules for the TIN for reporting FI, sponsor, intermediary,

entity account holder, and entity substantial owner.

TIN Format

A value for a TIN data element must be either in a GIIN format or in one of the following formats for a

U.S. TIN:

Nine consecutive digits without hyphens or other separators (e.g., 123456789)

Nine digits with two hyphens (e.g., 123-45-6789)

Nine digits with a hyphen entered after the second digit (e.g., 12-3456789)

Note: The FIN should be entered in the message header for filing purposes only. Do not use a FIN for any

TIN elements outside of the MessageSpec element or in the body of the FATCA XML report. If the TIN

field is omitted or the value is not in a valid format, the IRS will generate a record level error notification.

FATCA XML Schema v2.0 User Guide

37

4.5.3 Name

Figure 7 - NameOrganisation_Type

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Name

sfa:NameOrganisation_Type

Required

Name

nameType

stf:OECDNameType_EnumType

Optional

Null

The organization element can have multiple names, but FATCA reporting requires only one name

element. The value of the element should be the legal name of the entity or organization. The attribute

nameType is not required for FATCA reporting and may be omitted. If included the value should be from

the list below:

Value

Description

Value

Description

OECD201

SMFAlias or other

OECD205

AKA (also known as)

OECD202

Individual

OECD206

DBA (doing business as)

OECD203

Alias

OECD207

Legal

OECD204

Nick (Nickname)

OECD208

At Birth

4.5.4 Address

This data element is described elsewhere in the schema. For more information, go to Section 4.3.

Address_Type.

CorrectableReportOrganisation_Type 4.6

This data type transmits data for Reporting FI, Sponsor, and Intermediary organizations and was

extended from the OrganisationParty_Type by adding two elements: FilerCategory and DocSpec. The

structures of the sub-elements are described Section 4.5. OrganisationParty_Type.

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

Address

sfa:Address_Type

Required

FATCA XML Schema v2.0 User Guide

38

4.6.1 FilerCategory - New

Figure 8 - FilerCategory

Element

Attribute

Size

Data Type

Schema

Requirement

Application

Requirement

FilerCategory

ftc:FatcaFileCategory_EnumType

Optional

See rules below *

This data element identifies the filer category codes and may be required based on specific filing status,

such as direct reporting NFFE and Sponsoring Entities filing on behalf of direct reporting NFFEs. The

element or code may not be presented more than once. Note: This element should not be included for tax

years 2014 and 2015, but is required for 2016 and later years.

* Application Requirement:

Member of

Reporting FI

Group

Business Rule for 2016 and Later Tax Years

Reporting FI

Should be included or omitted based on the filing scenario:

The element should be included, if the reporting FI is not a Sponsored FFI,

Sponsored Direct Reporting NFFE, or Trustee-Documented Trust.

The element should be omitted, if the reporting FI is a Sponsored FFI,

Sponsored Direct Reporting NFFE, or Trustee-Documented Trust.

The only allowable values are described in Table 16. Filer category list.

Intermediary

Should not be included and if present, will cause a record level error notification:

The element is not allowed under the element Intermediary.

Sponsor

Should be included based on filing scenario:

The element must be included if the report contains a Sponsoring Entity. The

filer category element should be under the Sponsor element.

This element will be validated by the application and if not present, will

generate a record level error notification.

The only allowed values are FATCA 607, FATCA 608 or FATCA 609.

See additional business rules in Section 6.1. Sponsor.

Note: The FilerCategory element is reported under either the ReportingFI or the Sponsor element. It

should never to be included in an Intermediary element. The values and rules for inclusion of

FilerCategory are provided in Table 16. Filer category list.

FATCA XML Schema v2.0 User Guide

39

Filer Category Types:

If the financial institution reporting the account is a:

FilerCategory

for element

FilerCategory

Value

PFFI (other than a Reporting Model 2 FFI and including a U.S.

branch of a PFFI not treated as a U.S. person)

Reporting FI

FATCA601

RDC FFI (including a Reporting Model 1 FFI)

Note: If an HCTA in a Model 1 IGA jurisdiction is sending

information on accounts maintained by a Reporting Model 1

FFI, use filer category FATCA602 (RDC FFI).

Reporting FI

FATCA602

Limited Branch or Limited FFI

Reporting FI

FATCA603

Reporting Model 2 FFI

Reporting FI

FATCA604

Qualified Intermediary (QI), Withholding Foreign

Partnership (WP), or Withholding Foreign Trust (WT)

Reporting FI

FATCA605

Direct Reporting NFFE

Reporting FI