Michigan

Consumer Guide

to Health Insurance

Table of Contents

Employer Group Coverage .......................... 3

Individual Coverage ................................ 7

Costs for Individual Health Plans ................... 12

Types of Health Plans ............................. 16

Filing a Complaint With DIFS ....................... 19

Appealing a Decision Made by Your Health Insurer ... 20

Addional Resources .............................. 23

Glossary of Health Coverage and Medical Terms ... 23

Important Contact Informaon ................... 26

2 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

This guide provides consumers with health insurance basics to assist Michigan

residents in making informed decisions regarding their health coverage.

About DIFS

The mission of the Michigan Department of Insurance and Financial Services is to

ensure access to safe and secure insurance and nancial services fundamental for the

opportunity, security and success of Michigan residents, while fostering economic

growth and sustainability in both industries.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 3

Employer Group Coverage

The Employer Is the Policyholder

The employer is the master policyholder and the employees are cercate holders in an employer

group health plan. The master policyholder:

• Negoates the terms of the group policy with the health insurer.

• May reduce or change the plan’s benets.

• May increase the employees’ premium contribuon.

• Is permied to switch health insurers.

• May allow the employees to choose from more than one plan.

• Can stop providing coverage enrely.

Coverage and rates may change annually. The employee contribuon – what you pay – is

determined by your employer.

Employers with 50 or more employees are

required to provide health coverage to

employees and their dependents. Failure

to oer aordable coverage may subject

an employer to a tax penalty and allow

the employee to obtain a tax credit in the

Health Insurance Marketplace.

Employers with fewer than 50 employees

are not required to provide health

coverage. However, if they choose to oer

health coverage, they may be eligible for a

small business health care tax credit.

The Employer Is the Policyholder

The employer is the master policyholder and the employees are cercate holders in an employer

group health plan. The master policyholder:

• Negoates the terms of the group policy with the health insurer.

• May reduce or change the plan’s benets.

• May increase the employees’ premium contribuon.

• Is permied to switch health insurers.

• May allow the employees to choose from more than one plan.

• Can stop providing coverage enrely.

EMPLOYEE PREMIUMS

4 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Employer Group Coverage

Enrollment

Employees should be aware of the employer’s

group health coverage enrollment policies and

deadlines. Employers can require up to a 90-

day waing period before new employees are

eligible to enroll in coverage.

Employers have an annual open enrollment

period for employees to apply, change or

disenroll in coverage. Any benet changes or

premium adjustments in the group plan are

communicated to employees during the annual

open enrollment period.

Special enrollment periods (SEPs) are allowed

when certain life events occur (i.e., birth/

adopon, marriage/divorce). Check with the

employer’s human resources department for

more informaon about SEPs.

Benets of Employer Group

Health Plans

Employer group health plans typically oer:

• Limits on out-of-pocket maximums.

• No annual or lifeme dollar limits

on essenal health benets.

• Free prevenve services.

• Dependent coverage to age 26.

• Specic minimum benets required

by Michigan law.

Small Business Requirement

Employers with 50 or fewer employees are not

required to provide health coverage; however,

they are required to provide informaon about

the Marketplace to their employees, whether

they oer health coverage or not. If they oer

health coverage to their employees, they must

oer it to all eligible employees within 90 days of

their employment start date.

Small business employers can explore oering

health and/or dental insurance to their employees

through the Small Business Health Opons

Program (SHOP). An employer purchasing SHOP

coverage may be eligible for a small business

health care tax credit. To review plans and enroll

in coverage, contact an insurer or an insurance

agent licensed with DIFS and registered with

SHOP. SHOP health plans can be reviewed at

www.healthcare.gov/Small-Businesses or by

contacng the SHOP Call Center at 800-706-7893.

Wellness Plans

Employers may oer wellness plans to encourage

employee parcipaon in a healthy behavior,

maintenance or improvement program. If a health

insurer bases their health insurance rates on

tobacco use, they must oer a wellness program for

any group policy. For parcipaon in the wellness

plan, the insurer may provide the employees with:

• A rebate or reducon in premium.

• A reducon in co-payments,

co-insurance and deducbles.

• A combinaon of these incenves.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 5

A self-funded plan will not use

the term “insurance” in its

benet informaon package.

Instead, the word “plan” or

“summary plan descripon”

will be used.

Self-Funded Health Plans

If you work for a large employer or a

government agency, there is a good chance your

health plan is self-funded or self-insured. Self-

funded plans may work best for employers that

are large enough to oer substanal coverage

and pay expensive claims for medical services.

As long as claims are being paid, you may not

noce whether your employer has provided

coverage through a self-funded plan.

Employers may contract with insurance compa-

nies and third-party administrators to manage a

self-funded health plan.

DIFS does not have authority over employers

or self-funded plans. DIFS may, however, have

authority over the administrator of a self-funded

plan. Self-funded plans fall under the authority

of the United States Department of Labor’s

Employee Benet Security Administraon. They

can be reached at www.dol.gov/Agencies/EBSA

or 866-444-3272.

Losing Employer

Group Coverage

If you lose group health coverage through your

employer, you may have federal COBRA rights,

be eligible for Medicaid or the Healthy Michigan

Plan or be able to purchase health insurance

through a special enrollment period.

The following opons are available to those

losing employer group coverage:

• Temporarily connue the same group

health plan under COBRA. COBRA is

available to health plans of employers

with more than 20 employees.

• Purchase individual coverage through the

Health Insurance Marketplace, from a

licensed insurance agent or health insurer.

You can sll go to the Marketplace and

check to see if the rates oered there are

more suited for your needs even if your

employer has more than 20 employees.

You may be eligible for a subsidy.

• Enroll in another group health plan

you may be eligible for through a

new employer or a spouse’s plan.

• Purchase a short-term limited duraon plan

to bridge the gap between coverage during

a period of transion. See page 17 for more

informaon regarding short-term plans.

• Enroll in Medicare, Medicaid or the

Healthy Michigan Plan if you are eligible.

6 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Employer Group Coverage

The federal Health Insurance Portability and

Accountability Act (HIPAA) applies when you are

covered by an employer’s group health plan and

you move to a dierent employer also oering

health coverage.

If the new employer’s group health plan oers

dependent coverage, it must oer coverage to

your dependents who were covered under your

previous plan.

The new employer’s group health plan may cost

more and provide dierent coverage. If the new

employer health plan oers dependent cover-

age, it must have a special enrollment period

to add a dependent because of marriage, birth,

adopon or loss of other coverage. As with

individual health plans, group health plans may

not impose pre-exisng condion exclusions.

Employers with 20 or more employees must comply with COBRA, except health

plans sponsored by the federal government and some church-related organizaons.

Consolidated Omnibus

Reconciliaon Act (COBRA)

COBRA is a federal law that allows you the right

to connue employer group health coverage

on a temporary basis aer you, your spouse or

your parent leaves an employer with 20 or more

employees.

The employer must nofy the former employee

of their COBRA rights within 30 days aer

employment has ended. Once noed, the

former employee has 60 days to apply for

COBRA coverage and is responsible for paying

the enre premium, including any part the

employer paid, plus up to an addional 2% for

administrave expenses.

COBRA Coverage Is Available For:

• 18 months.

• 29 months if you became eligible for

Social Security disability during the

rst 60 days of COBRA coverage.

• 36 months if you were insured through

a spouse’s or parent’s employer and

the spouse or parent has become

eligible for Medicare, died, divorced or

separated or if the dependent child has

reached the age beyond eligibility.

COBRA is complicated! The employer’s human

resources oce should have a booklet explain-

ing the details. Addional quesons can be

addressed by the U.S. Department of Labor,

Employee Benets Security Administraon at

866-444-3272 or www.dol.gov/Agencies/EBSA.

Moving From One Employer

Group Plan to Another

Employer Group Plan

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 7

Individual Coverage

The monthly premium is the cost for your

health plan and depends on the following:

• The type of plan chosen.

• Your age.

• Where you live.

• The number of eligible dependents

covered under your plan.

• Tobacco use.

Premiums may increase each plan year to

reect the increasing cost of health care.

If you are a Michigan resident without access

to a group health plan and are ineligible for the

Healthy Michigan Plan, Medicaid or Medicare,

you may purchase an individual major medical

health plan through a licensed agent, directly

from a health insurer or through the Health

Insurance Marketplace (Marketplace).

You are the policyholder on an individual health

plan. The plan can cover you and your eligible

dependents and cannot deny coverage based

on pre-exisng condions.

The annual open enrollment period provides

an opportunity for you to enroll in an individual

health plan. Plans may be purchased outside of

open enrollment through a special enrollment

period under certain qualifying events.

To nd out which opons may be available to

you, call DIFS at 877-999-6442 or visit

www.michigan.gov/HICAP

Individual policies must include specic

minimum health care benets required by

Michigan and federal law. More informaon

regarding these requirements can be found at

www.michigan.gov/HICAP.

Open Enrollment

Required Benets

Premiums

8 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Healthy Michigan Plan

If you are uninsured and looking for coverage, you may be eligible for the Healthy

Michigan Plan. Individuals may be eligible for the Healthy Michigan Plan if they:

• Are age 19-64 years.

• Do not qualify for Medicaid.

• Are ineligible for or enrolled in Medicare.

• Are not pregnant when applying for the Healthy Michigan Plan.

• Earn up to 133% of the federal poverty level (adjusted annually).

• Are residents of Michigan.

Individual Coverage

Visit www.healthymichiganplan.org or call 855-789-5610 for more informaon.

Healthy Michigan Plan

If you are uninsured and looking for coverage, you may be eligible for the Healthy

Michigan Plan. Individuals may be eligible for the Healthy Michigan Plan if they:

• Are age 19-64 years.

• Do not qualify for Medicaid.

• Are ineligible for or enrolled in Medicare.

• Are not pregnant when applying for the Healthy Michigan Plan.

• Earn up to 133% of the federal poverty level (adjusted annually).

• Are residents of Michigan.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 9

Health Insurance

Marketplace

Health Insurance Marketplace (Marketplace)

is a federally operated insurance marketplace

where individuals and families can purchase

and compare health plans. The Marketplace is

primarily accessed at www.healthcare.gov or by

telephone at 800-318-2596.

An individual health plan may be purchased for

you and your family during the annual open

enrollment period with the Marketplace.

For informaon on how to purchase a health

plan outside of the Marketplace, please refer to

www.michigan.gov/HICAP.

CSRs allow you to save money when you

receive health care services. A health plan

with a CSR includes lower out-of-pocket costs,

such as a lower deducble, co-payment, co-

insurance and out-of-pocket maximum. To

qualify for a CSR, you must purchase a silver

level health plan on the Marketplace and

have a household income between 100%

to 250% of the federal poverty level. The

federal poverty level is adjusted annually.

• Advance premium tax credits

• Cost-sharing reducons

• Marketplace parcipaon

Advance Premium

Tax Credits (APTC)

An APTC is a federal tax credit that is used

to lower the monthly cost of a Marketplace

health plan. Eligibility for an APTC is

available for those with a household income

between 100% to 400% of the federal

poverty level. The federal poverty level is

adjusted annually. The Marketplace will

determine your eligibility for an APTC.

Cost-Sharing Reducons (CSR)When purchasing health coverage

through the Marketplace, it’s benecial

to understand the following:

Marketplace Parcipaon

Not all health insurers choose to parcipate in

the federal Marketplace. Prior to selling plans

on the Marketplace, an insurer’s qualied

health plan and rates must be cered

by DIFS and the federal government.

10 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Types of Qualied Health Plans

(QHP) on the Marketplace

QHPs are divided into ve metal levels. Each metal level represents how the cost for

health care services are split between you and the health plan.

The ve metal levels are: planum, gold, silver, bronze, and expanded bronze. Insurers

selling health plans on the Marketplace are not required to oer plans in every metal

level, or in all counes.

• Planum Level – These plans must cover 90% of expected health care costs

and you are nancially responsible for the remaining 10%.

• Gold Level – These plans must cover 80% of expected health care costs and

you are nancially responsible for the remaining 20%.

• Silver Level – These plans must cover 70% of expected health care costs and

you are nancially responsible for the remaining 30%.

• Bronze Level – These plans must cover 60% of expected health care costs and

you are nancially responsible for the remaining 40%.

• Expanded Bronze Level – These plans must cover between 56% and 62% of

expected health care costs.

If an expanded bronze plan covers and pays for at least one major

service, other than prevenve services, before the deducble or meets the

requirements to be a high deducble health plan, it must cover between 56%

and 65% of expected health care costs.

Qualied Health Plan (QHP): a health plan

that’s cered by the Health Insurance

Marketplace and DIFS. QHPs provide essenal

health benets, follow established limits on

cost-sharing (i.e., deducbles, co-payments,

and out-of-pocket maximum amounts), and

meet other requirements under the ACA.

Individual Coverage

Types of Qualied Health Plans

(QHP) on the Marketplace

QHPs are divided into ve metal levels. Each metal level represents how the cost for

health care services are split between you and the health plan.

The ve metal levels are: planum, gold, silver, bronze, and expanded bronze. Insurers

selling health plans on the Marketplace are not required to oer plans in every metal

level, or in all counes.

• Planum Level – These plans must cover 90% of expected health care costs

and you are nancially responsible for the remaining 10%.

• Gold Level – These plans must cover 80% of expected health care costs and

you are nancially responsible for the remaining 20%.

• Silver Level – These plans must cover 70% of expected health care costs and

you are nancially responsible for the remaining 30%.

• Bronze Level – These plans must cover 60% of expected health care costs and

you are nancially responsible for the remaining 40%.

• Expanded Bronze Level – These plans must cover between 56% and 62% of

expected health care costs.

If an expanded bronze plan covers and pays for at least one major

service, other than prevenve services, before the deducble or meets the

requirements to be a high deducble health plan, it must cover between 56%

and 65% of expected health care costs.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 11

Catastrophic Health Plans

In addion to the metal level plans described, catastrophic health plans are also

available on the Marketplace. However, these plans are available only to those

under age 30 or of any age who have received certain hardship exempons

through the Marketplace. Eligibility for a hardship exempon can be obtained

through www.healthcare.gov.

Catastrophic plans purchased through the Marketplace generally:

• Have lower premiums and higher deducbles.

• Cover three annual primary care visits prior to the deducble being met.

• Cover prevenve services at no cost.

• Are not eligible for federal tax credits.

12 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Costs for Individual Health Plans

There is more to shopping for health insurance

than just nding the lowest premium.

Considering your nancial status and family

needs, the boom line on your health insurance

may not be the monthly premium you pay.

A policy with a lower monthly premium may

seem like a beer deal, but a lower monthly

premium could mean you’ll have less coverage

– or that you’ll pay more out-of-pocket when

you need health care services.

Premiums for individual health plans on and

o the Marketplace are rated based on:

• Type of plan chosen

• Age

• Gender

• Geographic locaon

• Family size

• Tobacco use

Each year, DIFS publishes the names of the

insurers selling on the Marketplace, along with

their rates and changes in the rates. To view the

health plans available in your area and review

ancipated costs, visit www.michigan.gov/DIFS.

By compleng an applicaon through the

Marketplace, you can review plans and rates

available to you. Assistance signing up for a

Marketplace plan is available from navigators,

cered applicaon assisters and licensed

health insurance agents who have completed

training and registraon with the Marketplace.

Health insurance agents must also be licensed

with DIFS. These individuals cannot charge you

for their assistance. Visit localhelp.healthcare.

gov to nd assistance in your area. You may

also visit www.michigan.gov/DIFS to locate a

licensed agent.

DIFS’ role in the Health Insurance Marketplace

includes reviewing health plan rates and poli-

cies prior to the policies being available to sell

in the Marketplace.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 13

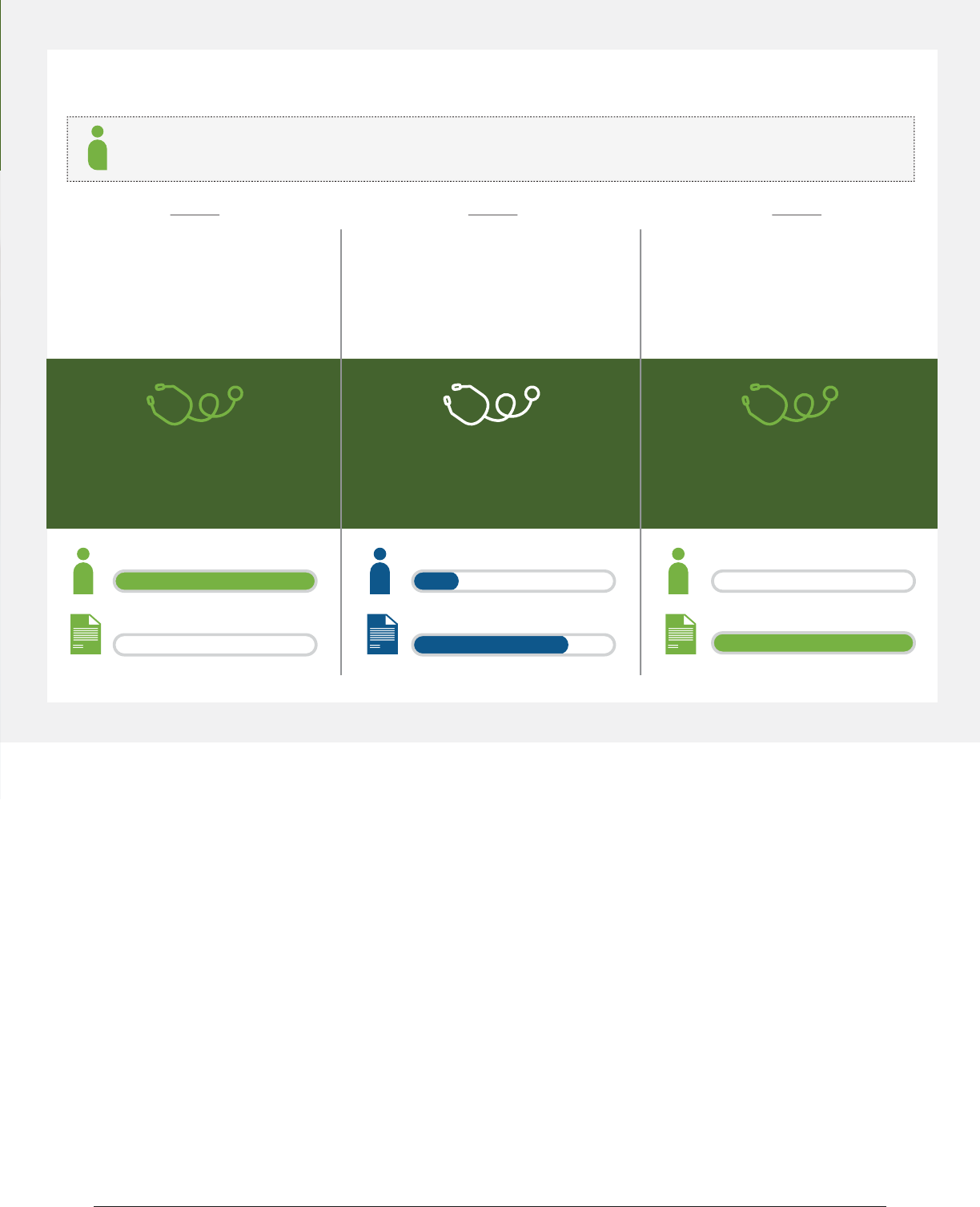

Example: How You and Your Insurer Share Costs Annually

Your Plan Deducble: $1,500 | Co-insurance: 20% | Out-of-Pocket Limit: $5,000

You have not reached your

$1,500 deducble yet.

Your plan does not pay

any of the costs.

You pay 100%

Your plan pays 0%

Office visit cost: $125

You pay: $125

Your plan pays: $0

You have reached your

$5,000 out-of-pocket limit.

You have seen the doctor oen and

paid $5,000 total. Your plan pays the

full cost of your covered health care

services for the rest of the year.

You pay 0%

Your plan pays 100%

Office visit cost: $200

You pay: $0

Your plan pays: $200

You have reached your $1,500

deducble; co-insurance begins.

You have seen a doctor several mes

and paid $1,500 total. Your plan pays

some of the costs of your next visit.

You pay 20%

Your plan pays 80%

Office visit cost: $75

You pay: 20% of $75 = $15

Your plan pays: 80% of $75 = $60

Plan year starng Jan. 1 and ending Dec. 31

1 2 3

What’s Covered

Health insurance helps pay for provider visits, hospital services and medicaons.

But remember, insurance isn’t just for when you get sick – it can also help you stay

healthy. Most plans cover prevenve services like immunizaons, annual visits,

screenings and more for free.

For more informaon on what your plan covers, review the “Summary of Benets

and Coverage.” If you don’t have one, ask your insurance company for a copy. The

Summary of Benets and Coverage explains the plan’s key features like:

• Covered health care services.

• Your share of the costs for a covered service.

• Health care services the plan does not cover.

14 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Costs for Coverage

Paying Medical Bills

Both the insured and insurer share the nancial

responsibility of health care services covered by a

health plan, otherwise known as cost-sharing. The

health plan explains exactly who pays for what.

It is the insured’s responsibility to understand

the benets of the health plan and how the plan

works. Contact the insurer’s customer service

department if there are quesons about the

plan’s benets. The insurer’s customer service

number can be located on the back of the

insurance card.

To beer understand the basics of health insur-

ance, review the following example of how an

insured would use their health plan:

• The insured person gives their insurance

card to the provider at the me

health care services are received.

• The co-payment is paid to the provider at

the me health care services are received.

• Usually, the provider submits a claim to

the health plan to receive payment for

the health care services. The insured

is responsible for subming the claim

if the provider doesn’t do it. This

typically occurs if services are received

from an out-of-network provider.

• The insurer sends an Explanaon of

Benets (EOB) to the insured if there

is a nancial responsibility for the

treatment received. The EOB lists the

date of service, the amount the provider

charged, the amount the insurer will

pay for the service(s) and your nancial

responsibility (deducble, co-payment,

co-insurance, non-covered benet).

The individual is responsible for their poron of

the bill when an invoice is received from the pro-

vider. It is important to keep a copy of the EOB

from the insurer to compare what the EOB says

you owe and what the provider is billing you.

Paying Medical Bills

Both the insured and insurer share the nancial

responsibility of health care services covered by a

health plan, otherwise known as cost-sharing. The

health plan explains exactly who pays for what.

It is the insured’s responsibility to understand

the benets of the health plan and how the plan

works. Contact the insurer’s customer service

department if there are quesons about the

plan’s benets. The insurer’s customer service

number can be located on the back of the

insurance card.

To beer understand the basics of health insur-

ance, review the following example of how an

insured would use their health plan:

• The insured person gives their insurance

card to the provider at the me

health care services are received.

• The co-payment is paid to the provider at

the me health care services are received.

• Usually, the provider submits a claim to

the health plan to receive payment for

the health care services. The insured

is responsible for subming the claim

if the provider doesn’t do it. This

typically occurs if services are received

from an out-of-network provider.

• The insurer sends an Explanaon of

Benets (EOB) to the insured if there

is a nancial responsibility for the

treatment received. The EOB lists the

date of service, the amount the provider

charged, the amount the insurer will

pay for the service(s) and your nancial

responsibility (deducble, co-payment,

co-insurance, non-covered benet).

The individual is responsible for their poron of

the bill when an invoice is received from the pro-

vider. It is important to keep a copy of the EOB

from the insurer to compare what the EOB says

you owe and what the provider is billing you.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 15

Specic quesons about coordinaon of benets may be directed to

DIFS at 877-999-6442.

Coordinaon of Benets (COB)

If you are covered by two or more

comprehensive health insurance policies, you

may be familiar with the term “coordinaon

of benets” (COB). Comprehensive health

insurance was designed to help cover the cost

of health care treatment; however, it was never

intended to pay more than 100% of that cost.

For this reason, COB rules were established to

address situaons where an individual has more

than one health plan and makes sure insurance

companies don’t duplicate or pay benets that

exceed 100% of the cost for treatment.

For policies issued In Michigan, the

COB Act of 1984 species how benets are

to be coordinated.

How Does COB Work?

The most common queson when two

or more comprehensive health insurance

policies are involved is “Who pays rst?” The

COB Act provides guidelines for the general

order by which the primary plan, the plan

that pays rst, and the secondary plan, the

plan that pays second, is determined.

The primary plan pays its share of the costs

rst, then the secondary plan pays up to

100% of the total cost of care. The plans

will not duplicate benets or pay more

than 100% of the cost for treatment.

It is important to note that COB rules for an

employee/subscriber/member dier from the

rules for dependent children.

The most common queson when two

or more comprehensive health insurance

policies are involved is “Who pays rst?” The

COB Act provides guidelines for the general

order by which the primary plan, the plan

that pays rst, and the secondary plan, the

plan that pays second, is determined.

The primary plan pays its share of the costs

rst, then the secondary plan pays up to

100% of the total cost of care. The plans

will not duplicate benets or pay more

than 100% of the cost for treatment.

It is important to note that COB rules for an

employee/subscriber/member dier from the

rules for dependent children.

How Does COB Work?

16 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Types of Health Plans

It is important to know the dierent types

of health plans to make the best use of your

benets and money.

Not all plans oer Minimum Essenal Coverage

(MEC), as dened under the Aordable Care

Act. MEC may be an individual or group health

plan, Medicaid, the Healthy Michigan Plan and

Medicare. The most common major medical

plans providing MEC are described below.

For more informaon related to MEC health

plans, visit www.healthcare.gov.

Health Plans

Minimum Essenal Coverage

• Health Maintenance Organizaon (HMO)

An HMO is a type of health plan that usually

limits coverage to their network of providers.

It generally won’t cover out-of-network care

except in an emergency. An HMO may require

you to live or work in the service area to be

eligible for coverage. All care is coordinated

through the member’s primary care physician

(PCP); therefore, you must designate a PCP.

• HMO Point-of-Service Plan

An HMO Point-of-Service plan oers in-network

and out-of-network benets. There may be

higher out-of-pocket costs for health care

services received outside the HMO’s network.

• Preferred Provider Organizaon (PPO)

A PPO is a contract between an insurer and

a network of providers agreeing to provide

health care services at a negoated rate. PPOs

may be less restricve than HMOs because

they do not require a referral to see other

providers. There are also out-of-network

benets with a higher nancial responsibility.

• Preferred Provider Arrangement (PPA)

A PPA is an oponal feature of a health plan.

The plan includes a network of parcipang

providers available to the insured to

obtain cost-eecve medical services.

• High Deducble Plans

These major medical plans are oen sold in

conjuncon with Health Savings Accounts.

They pay the cost of inpaent hospital

care and outpaent medical bills with high

deducbles. The nancial responsibility under

these plans changes annually and is paid from

a federally tax-exempt Health Savings Account.

Visit www.michigan.gov/HICAP for more infor-

maon on the annual limits under this plan.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 17

Health Plans

Limited Benets

• Short-Term Limited Duraon Plan

In Michigan, short-term limited duraon

plans are limited to a coverage period of

185 days out of any 365-day period. These

policies are not required to cover pre-exisng

condions, cannot be renewed or extended

for more than 185 days and do not sasfy

the requirement to have health insurance.

They also do not have to comply with

Aordable Care Act protecons, including

prohibions on annual or lifeme limits,

essenal health benets, protecons against

rescissions and cost-sharing limitaons.

• Limited Benet Plans

Limited benet plans provide reduced benets

intended to supplement comprehensive

health insurance, not to be an alternave

to them. These types of plans limit the

amount of coverage the company will

pay per episode of injury or illness.

» Accident Only

Accident only plans provide a cash

payment in the event of injury or death

resulng from a covered accident. For

example, the policy may pay a $200 benet

for each covered accident.

» Hospital Indemnity

Hospital indemnity plans pay a cash benet

in the event of hospitalizaon and/or surgery

resulng from a covered illness or injury. For

example, the policy may pay a $100 per-day

benet while the insured is hospitalized.

• Specied (Dread) Disease Plan

A specied disease plan provides benets

for specied causes of illness, disease or

injury, such as a heart aack, stroke or

cancer diagnosis. For example, the policy

may pay a $30,000 benet for an inial

cancer diagnosis while the policy is in force.

• Incidental Policies

Individual policies for dental and/or vision

benets pay for care not covered by typical

comprehensive health insurance and may be

available on a limited basis. Stand-alone dental

plans can be purchased through the Health

Insurance Marketplace during open enrollment

and o the Marketplace directly from an

insurer at any me throughout the year.

18 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Types of Health Plans

Health Plans

Medical Expense Reimbursement

• Health Savings Account (HSA)

HSAs are tax-exempt accounts set up by

an employer or individual to pay expenses

including deducbles, co-payments and other

out-of-pocket prescribed medical expenses.

An HSA must be established with a high

deducble health plan. The HSA is used to

pay roune expenses and the health plan is

used to pay more signicant expenses. HSAs

allow employers and consumers to set aside

funds on a tax-free basis to pay health care

expenses, including expenses that may not

be covered by tradional health coverage.

For example, HSAs may be used for vision and

dental services, prescripon drugs, over-the-

counter drugs (if you have a prescripon for

them), long-term care services and certain

health insurance premiums during rerement.

• Health Reimbursement Account (HRA)

HRAs are employer-funded group health

plans from which employees are reimbursed

tax-free for qualied medical expenses up

to a xed dollar amount per year. Unused

amounts may be rolled over to be used in

subsequent years. The employer funds and

owns the account. Health Reimbursement

Accounts are somemes called Health

Reimbursement Arrangements.

• Individual Coverage Health

Reimbursement Account (ICHRA)

Eecve January 1, 2020, employers can

begin oering employer funded ICHRAs as

an alternave to tradional group health

plan coverage. ICHRAs are arrangements

under which employees are reimbursed

tax-free for qualied medical care expenses

and premiums paid for individual health

insurance you’ve chosen, up to a certain

dollar amount for the plan year. Unused

funds can be rolled over to be used in

subsequent years. If you enroll in an ICHRA,

you must also be enrolled in an individual

health insurance plan purchased on or o the

Exchange, or Medicare (Part A and B, or C)

for each month you’re enrolled in the ICHRA.

• Excepted Benet Health

Reimbursement Account (EBHRA)

Eecve January 1, 2020, employers can

begin oering employer-funded EBHRAs

in conjuncon with a tradional group

health plan. The annual EBHRA employer

contribuon is limited to $1,800 (indexed for

inaon beginning in 2021). Employees may

enroll in the EBHRA even if they do not enroll

in the tradional group health plan or any

other coverage. EBHRAs are arrangements

under which employees are reimbursed

tax-free for qualied medical care expenses

and premiums paid for excepted benets,

such as dental and vision coverage, as well

as for short-term limited duraon insurance

(STDLI). EBHRAs cannot be used to reimburse

individual health insurance premiums, group

health plan premiums (other than COBRA),

or Medicare premiums. Unused funds can be

rolled over to be used in subsequent years.

For more informaon on HSAs and HRAs,

visit www.irs.gov.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 19

Filing a Complaint With DIFS

DIFS regulates the business of insurance

transacted in Michigan. Our authority pertains

to contracts issued in Michigan. DIFS accepts

complaints from pares involved in the contract,

such as the insured, policyholder or cercate

holder. Because a health care provider is usually

not a party to the health plan, DIFS generally

does not accept complaints from providers.

There are some excepons to this rule.

DIFS will pursue appropriate complaints from

providers acng as the authorized representave

of a paent; however, wrien authorizaon from

the paent or their legal representave must be

included with the complaint.

DIFS will accept complaints from providers

having problems with receiving timely

payment for submitted claims without any

errors or other issues. These claims are

referred to as “clean claims” and must be paid

within 45 days after they are received by the

health plan. For more information on clean

claims and to obtain the Clean Claim Report

form, visit www.michigan.gov/DIFS.

If you have a provider-related billing dispute,

these complaints can be submied to the

Michigan Aorney General Consumer Protecon

Division for review. The oce

can be reached toll-free at 877-765-8388 or

www.michigan.gov/AG.

You do not always need an aorney to resolve most

claim disputes with an insurer. Start with contacng

the insurer’s customer service department. Most

insurers have toll-free telephone numbers located

on the back of your insurance card.

If a sasfactory resoluon is not received, ask

about the insurer’s appeal process or le a

wrien complaint with the Michigan Department

of Insurance and Financial Services (DIFS).

DIFS will send the insurer a copy of the

complaint and ask them to explain its posion.

Insurers are required by law to respond to

DIFS. We will review the facts to ensure the

health insurer has complied with your contract

language and all rules and regulaons.

How to File a Complaint With DIFS

Complaints can be submied as follows:

• Online: www.michigan.gov/DIFScomplaints

• Email: DIFSc[email protected]

• Fax: 517-284-8837 or 517-284-8853

• Mail: The Department of Insurance

and Financial Services

Oce of Consumer Services

PO Box 30220

Lansing, MI 48909

• Contact DIFS toll-free at

877-999-6442 to request a complaint

form be sent to you via mail, email or fax.

Health Care Provider Complaints

20 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Michigan law provides you the right to le an

internal appeal if you disagree with your health

Appealing a Decision

Made by Your Health Insurer

Internal Grievance Process

If you disagree with a decision your health

insurer made regarding your health care claim,

you have the right to appeal the decision. There

are two levels of appeal – an internal appeal

with your health insurer and an external review

with the Department of Insurance and Financial

Services (DIFS).

The external review process should be

iniated only if:

1. The covered person has exhausted the

health carrier’s internal grievance process.

2. The health carrier fails to provide

a determinaon within the

meframe dictated by law.

Internal Appeal Process

insurer’s claim determinaon, also known as an

adverse determinaon.

An adverse determinaon means that an admis-

sion, availability of care, connued stay or other

health care service that is a covered benet has

been denied, reduced, or terminated. Failure

to respond in a mely manner to a request

for a claim determinaon is also an adverse

determinaon.

When you receive an adverse determinaon

noce, you must nofy your health insurer in

wring that you want to appeal its decision.

The adverse determinaon noce will provide

the meframe in which you are required to

submit your wrien appeal. Once you le an

appeal, the health insurer is required to com-

plete the internal grievance process within:

• 30 calendar days for a pre-service denial.

• 60 calendar days for a post-service denial.

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 21

You have the right to request an expedited

external review in situaons where the normal

PRIRA review meframe would seriously

jeopardize your life, health, or ability to regain

maximum funcon. An expedited external

review is conducted within 72 hours and

requires your treang physician to verify, orally

or in wring, the necessity of an expedited

review. You are not eligible for an expedited

external review if it concerns a health care

service that has already been received.

External Review Process

If you do not agree with the health insurer’s

nal adverse determinaon, you have 127 days

to le an external review under the Paent’s

Right to Independent Review Act (PRIRA).

To request an external review, you or your

authorized representave must complete the

Health Care Appeals-Request for External Review

form. In addion to the form, the external review

request should include a copy of the nal adverse

determinaon from your health insurer, the

reason(s) why you are appealing the decision and

any documentaon to support your posion.

If the external review concerns a denial based on

an experimental and/or invesgaonal service,

your treang provider must complete the

Treang Provider Cercaon for Experimental/

Invesgaonal Denials form and submit it with

your request.

For addional informaon related to DIFS’ external

review process and to access the required forms,

visit www.michigan.gov/DIFS or contact DIFS at

877-999-6442. Upon receipt, DIFS will examine

your external review request to determine if it

meets the requirements under PRIRA.

If your request is accepted and involves a

contractual dispute, the external review is

conducted by DIFS. If your request is accepted

and involves issues of medical necessity or

clinical review, it is referred for review to an

independent review organizaon. In both

instances, the Director of DIFS will issue an order

with the decision of the review.

Appointment of Authorized

Representave

Expedited External Review

You may authorize in wring any person, such

as a doctor, aorney, parent or spouse, to

represent you in the internal grievance process

and/or the PRIRA external review process.

In the PRIRA external review process, this

person is called an authorized representave.

The Health Care Appeals-Request for External

Review form provides space to authorize a

representave, who will be DIFS’ sole contact in

the PRIRA external review process.

22 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Appeal process is complete. If you or the health insurer disagrees with DIFS’ order,

an appeal can be filed in circuit court in Ingham County or the county in which you reside.

Send your appeal in

wring to health insurer

The health insurer agrees

to reverse its decision

Does your health insurer

have a second-level appeal?

File external review with DIFS

Director’s order is issued

The service or payment is

provided to you

Iniate second-level appeal

Do you sll disagree with the

health insurer’s decision?

The health insurer agrees

to reverse its decision

YES

YES

YES

Appeal Process Flow Chart

Receive adverse

determinaon

NO

NO

NO

!!!

22 • Michigan Consumer Guide to Health Insurance • michigan.gov/DIFS

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 23

This glossary has many commonly used terms but isn’t a full list. These glossary terms and denions are

intended to be educaonal and may be dierent from the terms and denions in your plan. Some of these

terms also might not have the same meaning when used in your policy or plan and, in any such case, the policy

or plan governs. (See your Summary of Benets and Coverage for informaon on how to get a copy of your

policy or plan documents.)

Allowed Amount

Maximum amount on which

payment is based for covered

health care services. This may

be called “eligible expense,”

“payment allowance” or

“negoated rate.” If your provider

charges more than the allowed

amount, you may have to pay the

dierence (see Balance Billing).

Appeal

A request for your health

insurer or plan to review a

decision or a grievance again.

Balance Billing

When a provider bills you for

charges not paid by your health

insurance because the charges are

higher than the allowed amount.

For example, if the provider's

charge is $100 and the allowed

amount is $70, the provider may

bill you the $30 dierence.

Co-Insurance

Your share of the costs of a

covered health care service,

calculated as a percent (for

example, 20%) of the allowed

amount for the service. You pay

co-insurance plus any deducbles

you owe. For example, if the

health insurance or plan’s allowed

amount for an oce visit is $100

and you’ve met your deducble,

your co-insurance payment of

20% would be $20. The health

insurance or plan pays the

rest of the allowed amount.

Complicaons of Pregnancy

Condions due to pregnancy,

labor, and delivery that require

medical care to prevent serious

harm to the health of the

mother or the fetus. Morning

sickness and non-emergency

caesarean secon aren’t

complicaons of pregnancy.

Co-Payment

A xed amount (for example,

$15) you pay for a covered

health care service, usually when

you receive the service. The

amount can vary by the type of

covered health care service.

Deducble

The amount you owe for covered

health care services before

your health insurance or plan

begins to pay. For example,

if your deducble is $1,000,

your plan won’t pay anything

unl you’ve met your $1,000

deducble for covered health

care services. The deducble

may not apply to all services.

Durable Medical

Equipment (DME)

Equipment and supplies ordered

by a health care provider

for everyday or extended

use. Coverage for DME may

include oxygen equipment,

wheelchairs, crutches or blood

tesng strips for diabecs.

Emergency Medical Condion

An illness, injury, symptom,

or condion so serious

that a reasonable person

would seek care right away

to avoid severe harm.

Emergency Medical

Transportaon

Ambulance service for an

emergency medical condion.

Emergency Room Care

Treatment you receive in

an emergency room.

Emergency Services

Evaluaon of an emergency

medical condion and

treatment to keep the condion

from geng worse.

Addional Resources

Glossary of Health Coverage

and Medical Terms

24 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Excluded Services

Health care services that

your health insurance or plan

doesn’t pay for or cover.

Grievance

A complaint that you communicate

to your health insurer or plan.

Habilitave Services

Health care services that help a

person keep, learn or improve skills

and funconing for daily living.

Examples include therapy for a child

who isn’t walking or talking at the

expected age. These services may

include physical and occupaonal

therapy, speech-language pathology

and other services for people with

disabilies in a variety of inpaent

and/or outpaent sengs.

Health Insurance

A contract that requires your

health insurer to pay some or

all of your health care costs in

exchange for a premium.

Home Health Care

Health care services a

person receives at home.

Hospice Services

Service to provide comfort

and support for persons in

the last stages of a terminal

illness and their families.

Hospitalizaon

Care in a hospital that requires

admission as an inpaent and

usually requires an overnight stay.

An overnight stay for observaon

could be outpaent care.

Hospital Outpaent Care

Treatment in a hospital that usually

doesn’t require an overnight stay.

In-Network Co-Insurance

The percent (for example, 20%)

you pay of the allowed amount

for covered health care services

to providers who contract

with your health insurance or

plan. In-network co-insurance

usually costs you less than out-

of-network co-insurance.

In-Network Co-Payment

A xed amount (for example,

$15) you pay for covered health

care services to providers

who contract with your health

insurance or plan. In-network

co-payments usually are less than

out-of-network co-payments.

Medically Necessary

Health care services or

supplies needed to prevent,

diagnose, or treat an illness,

injury, condion, disease or

its symptoms and that meet

accepted standards of medicine.

Network

The facilies, providers and

suppliers your health insurer

or plan has contracted with to

provide health care services.

Non-Preferred Provider

A provider who doesn’t have a

contract with your health insurer

or plan to provide services to

you. You’ll pay more to see a

non-preferred provider. [Check

your policy to see if you can

go to all providers who have

contracted with your health

insurance or plan or if your

health insurance or plan has a

“ered” network and you must

pay extra to see some providers.]

Out-of-Network Co-Insurance

The percent (for example, 40%)

you pay of the allowed amount

for covered health care services

to providers who do not contract

with your health insurance or

plan. Out-of-network co-insurance

usually costs you more than

in-network co-insurance.

Out-of-Network Co-Payment

The xed amount (for example,

$30) you pay for covered health

care services from providers who

do not contract with your health

insurance or plan. Out-of-network

co-payments usually are more

than in-network co-payments.

Out-of-Pocket Limit

The most you pay during a policy

period (usually a year) before your

health insurance or plan begins to

pay 100% of the allowed amount.

This limit never includes your

premium, balance-billed charges or

health care your health insurance

or plan doesn’t cover. Some health

insurance or plans don’t count all

of your co-payments, deducbles,

co-insurance payments, out-

of-network payments or other

expenses toward this limit.

Physician Services

Health care services a licensed

medical physician (M.D. – doctor

of medicine or D.O. – doctor

of osteopathic medicine)

provides or coordinates.

Plan

A benet your employer,

union or other group sponsor

provides to you to pay for

your health care services.

Addional Resources

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 25

Preauthorizaon

A decision by your health insurer

or plan that a health care service,

treatment plan, prescripon drug,

or durable medical equipment is

medically necessary. Somemes

called prior authorizaon, prior

approval, or precercaon.

Your health insurance or plan

may require preauthorizaon

for certain services before you

receive them, except in an

emergency. Preauthorizaon isn’t

a promise your health insurance

or plan will cover the cost.

Preferred Provider

A provider who has a contract

with your health insurer or

plan to provide services to

you at a discount. Check your

policy to see if you can see all

preferred providers or if your

health insurance or plan has a

“ered” network and you must

pay extra to see some providers.

Your health insurance or plan

may have preferred providers

who are also “parcipang”

providers. Parcipang providers

also contract with your health

insurer or plan, but the discount

may not be as great, and you

may have to pay more.

Premium

The amount that must be paid for

your health insurance or plan. You

and/or your employer usually pay

it monthly, quarterly or yearly.

Prescripon Drug Coverage

A health insurance benet

that helps pay for prescripon

drugs and medicaons.

Prescripon Drugs

A drug that by law requires

a medical prescripon.

Primary Care Physician

A physician (M.D. – doctor of

medicine or D.O. – doctor of

osteopathic medicine) who directly

provides or coordinates a range of

health care services for a paent.

Primary Care Provider

A physician (M.D. – doctor of

medicine or D.O. – doctor of

osteopathic medicine), nurse

praconer, clinical nurse

specialist or physician assistant,

as allowed under state law,

who provides, coordinates or

helps a paent access a range

of health care services.

Provider

A physician (M.D. – doctor of

medicine or D.O. – doctor of

osteopathic medicine), health care

professional or health care facility

licensed, cered or accredited

as required by state law.

Reconstrucve Surgery

Surgery and follow-up treatment

needed to correct or improve

a part of the body because

of birth defects, accidents,

injuries or medical condion.

Rehabilitaon Services

Health care services that help a

person keep, get back or improve

skills and funconing for daily

living that have been lost or

impaired because a person was

sick, hurt or disabled. These

services may include physical

and occupaonal therapy,

speech-language pathology

and psychiatric rehabilitaon

services in a variety of inpaent

and/or outpaent sengs.

Skilled Nursing Care

Services from licensed nurses

in your own home or in a

nursing home. Skilled care

services are from technicians

and therapists in your own

home or in a nursing home.

Specialist

A physician specialist focuses on

a specic area of medicine or a

group of paents to diagnose,

manage, prevent or treat certain

types of symptoms and condions.

A non-physician specialist is a

provider who has more training

in a specic area of health care.

UCR (Usual, Customary and

Reasonable)

The amount paid for a medical

service in a geographic area based

on what providers in the area

usually charge for the same or

similar medical service. The UCR

amount somemes is used to

determine the allowed amount.

Urgent Care

Treatment for an illness, injury

or condion that is serious

enough that a reasonable

person would seek care right

away but not so severe as to

require emergency room care.

Addional Resources

Updated Contact Information 6/2022

Important Contact Information

Michigan Department of Insurance and Financial

Services (DIFS)

• Michigan.gov/DIFS

• Phone: 877-999-6442

______________________________________

Health Insurance Marketplace

• Healthcare.gov

• Phone: 800-318-2596

______________________________________

SHOP Marketplace

The Small Business Health Options Program

(SHOP) Marketplace is a federally operated

insurance marketplace where small businesses

may shop for and compare group health coverage.

• Healthcare.gov/Small-Business

• Phone: 800-706-7893

______________________________________

Michigan Department of Health & Human

Services (MDHHS)

Apply for Michigan health care programs like

Medicaid, Healthy Michigan Plan and MiChild at:

• Michigan.gov/MiBridges

• Phone: 855-276-4627

• Michigan.gov/MDHHS

• Phone: 855-789-5610

• Michigan.gov/HealthyMiPlan

• Phone: 855-789-5610

Free Health Clinics

Free Clinics of Michigan (FCOM) is a network of

volunteer-staffed free clinics that provide health

care services to the uninsured or medically

underserved in Michigan.

• FCOMi.org

• Phone 248-635-8695

______________________________________

U.S. Department of Labor – Employee Benefits

Security Administration (USDOL)

The USDOL regulates self-funded health plans and

the Consolidated Omnibus Budget Reconciliation

Act (COBRA).

• DOL.gov/Agencies/EBSA

• Phone: 866-444-3272

______________________________________

Michigan Attorney General – Consumer

Protection

Handles complaints and answers questions

regarding provider billing issues.

• Michigan.gov/AG

• Phone: 877-765-8388

Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS • 27

28 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

Don’t Know Where to Turn?

Health Insurance Consumer Assistance Program (HICAP)

The Health Insurance Consumer Assistance Program is operated by the

Department of Insurance and Financial Services to help Michigan consumers with

health insurance issues

• www.michigan.gov/HICAP

• Telephone: 877-999-6442

Medicare

Medicare provides health insurance for people age 65 or older, some under age 65 with

disabilies, and those experiencing kidney failure.

• www.medicare.gov

• Telephone: 800-MEDICARE (800-633-4227)

Michigan Medicare/Medicaid Assistance Program (MMAP)

MMAP provides free educaon and personalized assistance to people with Medicare

and Medicaid, their families and caregivers.

• www.mmapinc.org

• Telephone: 800-803-7174

MMAP provides free educaon and personalized assistance to people with Medicare

and Medicaid, their families and caregivers.

• www.mmapinc.org

• Telephone: 800-803-7174

30 • Michigan Consumer Guide to Health Insurance • www.michigan.gov/DIFS

www.michigan.gov/DIFS

This Consumer Guide was created by the State of Michigan, Department of Insurance and

Financial Services (DIFS) and supported by Funding Opportunity Number

PR-PRP-18-001 from the U.S. Department of Health & Human Services, Centers for

Medicare & Medicaid Services. The contents provided are solely the responsibility of the

authors and do not necessarily represent the ocial views of HHS or any of its agencies.