Research and development tax relief

Making R&D easier for small companies

2 Research and development tax relief: Making R&D easier for small companies

Contents

Making R&D easier for small companies 3

Background 4

What is R&D tax relief? 5

Is my company small or large? 7

Does my company have linked or partner companies? 8

Which projects qualify? 10

How to show that your project is R&D within the tax definition 12

The start and end of a project for R&D tax purposes 14

What costs qualify? 16

What costs do not qualify 19

Subcontracted R&D 20

Subcontracting — who can make a claim? 22

Grants and subsidies 23

More on grants and subsidies 24

Why is RDEC important to SMEs? 25

How to claim R&D relief 26

How to calculate your claim 28

Keeping records 31

Advance Assurance 32

Case Studies 34

The Agri-food Sector 35

ICT 36

Advanced materials 37

Advanced engineering 38

Life and health sciences 39

Construction 40

Further help 41

Frequently asked questions 42

Glossary 43

3 Research and development tax relief: Making R&D easier for small companies

Making R&D easier

for small companies

This guidance outlines how tax relief

for Research and Development (R&D)

works for small and medium-sized

enterprises (SMEs).

It provides:

• straightforward definitions and explanations of

the schemes

• details of qualifying costs

• guidance on how to make a claim under the SME

and RDEC schemes

• advice on where to find help and further detailed

information.

This publication provides general guidance on the law, but how the law applies in a particular case is fact-dependent

and where there is doubt you should contact HMRC.

4 Research and development tax relief: Making R&D easier for small companies

Background

In 2000 the government introduced

a scheme to encourage scientific and

technological innovation within the

United Kingdom.

R&D is a Corporation Tax (CT) tax relief that may reduce

your company’s tax bill if your company is liable for

CT or, in some circumstances, you may receive a

payable tax credit. This guidance is designed to help

you make a claim for tax relief if you are an SME.

The Research and Development Expenditure Credit

(RDEC) scheme was introduced in the Finance Act 2013

— it enables companies with no CT liability to benefit

through a cash payment or a reduction of tax or other

duties due.

Specific definitions of R&D can be found at:

gov.uk/hmrc-internal-manuals/corporate-intangibles-

research-and-development-manual/cird81900

Further guidance on RDEC can be found at:

gov.uk/hmrc-internal-manuals/corporate-intangibles-

research-and-development-manual/cird89705

5 Research and development tax relief: Making R&D easier for small companies

What is R&D relief?

6 Research and development tax relief: Making R&D easier for small companies

What is R&D relief?

For tax purposes, R&D takes place when

a project seeks to achieve an advance in

overall knowledge or capability in a field

of science or technology.

R&D relief allows companies that carry out qualifying

R&D related to their trade to claim an extra CT

deduction for certain qualifying expenditure.

The level of relief available depends upon

which scheme the company uses.

The SME scheme

From 1 April 2015, the relief a company can get has

increased to 230% on their qualifying R&D costs.

Loss-making companies can in certain circumstances

surrender their losses in return for a payable tax credit.

Research and Development Expenditure Credit

(RDEC) scheme

From 1 April 2015 a taxable credit is available at

11% of qualifying R&D expenditure. For loss making

companies the tax credit is fully payable (subject to

certain restrictions).

Features of the RDEC scheme

Companies with no CT liability will benefit from RDEC

either through a cash payment or a reduction of tax or

other duties due. The payable credit is limited to the

company’s PAYE/NIC liabilities of the staff engaged

in qualifying activities in the accounting period.

SMEs will be able to claim RDEC if they do subcontracted

or subsidised research. Companies in groups can

surrender the RDEC against another group company’s

CT liability.

Further information on SMEs can be found on page 23.

7 Research and development tax relief: Making R&D easier for small companies

Is my company small or large?

To find out if a company is an SME for R&D tax relief

purposes we look at:

• staff headcount (less than 500)

• either turnover (€100m) or balance sheet total

(less than €86m).

When accounts are prepared in sterling, convert the

turnover and balance sheet totals to euros, using the

exchange rate for the balance sheet date.

Sometimes, a company will have to take into account

its own data, a proportion of a partner enterprise’s data

or the data of a linked enterprise. There’s more about

partner and linked enterprises on the next page. If your

company has no external investors and isn’t in a group,

you only need to count your own company data.

8 Research and development tax relief: Making R&D easier for small companies

Does my company have linked

or partner companies?

If your company has external investors

or is in a group, it’s worth looking at

the detailed guidance. The following is

a summary of the main rules.

Linked companies

If the company is controlled by or controls other

companies it is a linked company, for example if it

has more than 50% of the shareholders’ or members’

voting rights in another company.

The data of the linked companies should be added

to the data from the company that does the R&D.

Partner companies

If 25% or more of a company is owned by another,

or if the company owns 25% or more of another, it is

a partner company.

Certain companies and types of investor are excluded

from consideration as a partner. There is more about

this in the detailed guidance.

Detailed guidance on linked and partner companies

can be found at: gov.uk/hmrc-internal-manuals/

corporate-intangibles-research-and-development-

manual/cird91000

A proportion of the data of the partner companies

should be added to the data from the company that

does the R&D. So if the other company controls 30%

of the R&D company, add 30% of its data.

9 Research and development tax relief: Making R&D easier for small companies

B

owns 60% of

A

A

does the

R&D

D

owns 25% of

B

C

owns 35% of

B

A will add 25% of the accounts figures of D.

So if D has a turnover of €30m,

A will add €7.5m to its totals.

A will add 100% of the accounts figures of B.

So if B has assests of €10m,

A will add €10m to its totals.

A will add 35% of the of the accounts figures

of C. So if C has turnover of €100m, A will

add €35m to its totals

Example of a company being a linked or

partner company

Company A is linked to Company B because B has a

60% holding in A.

B also has two partner companies: C and D,

which own 32% and 25% of B.

A must add 100% of the data of B plus 35% of the

data of C and 25% of the data of D to its own data.

10 Research and development tax relief: Making R&D easier for small companies

Which projects qualify?

11 Research and development tax relief: Making R&D easier for small companies

Which projects qualify?

Work that advances overall knowledge

or capability in a field of science or

technology, and projects and activities

that help resolve scientific or technological

uncertainties, may qualify for R&D relief.

R&D has a specific statutory definition for the

purposes of R&D tax relief which is not the same as

the commercial, engineering or accounting definitions.

To qualify the company must be carrying out research

and development work in the field of science or

technology. The relief is not just for ‘white coat’ scientific

research but also for ‘brown coat’ development work in

design and engineering that involves overcoming difficult

technological problems.

This can include creating new processes, products or

services, making appreciable improvements to existing

ones and even using science and technology to duplicate

existing processes, products and services in a new way.

But pure product development in itself does not qualify.

Some examples of qualifying activities include software

development, engineering design, new construction

techniques, bio-energy, cleantech, agri-food and life

and health sciences. There are case studies at the end

of this guide for these industries.

Things to consider

• Does my company have a project?

• Am I seeking an advance in a field of science

or technology?

• Does the advance extend the overall knowledge

or capability in the field of science or technology

and not just the company’s own state of knowledge

or capability?

• Does the project involve an uncertainty that competent

professionals can’t readily resolve and where solutions

aren’t common knowledge?

Judging which projects and activities will qualify for

R&D tax relief is usually the area where most people

seek help. Experience has shown that companies

can benefit from HMRC’s early involvement. There is

information about our Advance Assurance scheme,

which helps with these issues, later in this guide.

12 Research and development tax relief: Making R&D easier for small companies

How to show that your project

is R&D within the tax definition

When you submit a claim it helps if you

give details of your project. The questions

below will help you decide if your project

is within our definition for R&D. If your

claim clearly sets out how you approach

these questions, it helps HMRC see that

your company really is doing R&D.

1. What is the scientific or technological advance?

Concentrate on the science and technology

Rather than stating the product, process or functionality

being developed, consider what scientific or technological

advance is being sought. This focuses attention on the

project’s aim for an advance. This is important in judging

whether or not R&D for tax relief purposes is being

undertaken.

Some activities aren’t science

Science doesn’t include work in the arts, humanities

and social sciences (including economics).

‘Commercially innovative’ isn’t enough

It’s not enough that a product is commercially

innovative. You can’t claim in respect of projects to

develop innovative business products or services that

don’t incorporate any advance in science or technology.

2. What scientific or technological uncertainties

were encountered?

Did you really encounter ‘uncertainty’?

Scientific or technological uncertainty exists when

knowledge of whether something is scientifically

possible or technologically feasible, or how to achieve

it in practice, isn’t readily available or deducible by a

competent professional working in the field.

Not every problem is an uncertainty

But uncertainties that can be resolved through

relatively brief discussions with peers are routine

uncertainties rather than technological uncertainties.

Technical problems that have been overcome in

previous projects on similar systems aren’t likely to

be technological uncertainties.

Set out what happened

In your claim, you should set out at a high level, in a

way that can be understood by someone who’s not

an expert, what the uncertainties were and when they

started and ended.

13 Research and development tax relief: Making R&D easier for small companies

3. How and when were the uncertainties overcome?

Describe the methods used to overcome the

uncertainties and the investigations and analysis

undertaken. This shouldn’t be in great detail,

but enough to show it wasn’t straightforward.

Describe the successes and failures and the impact of

these on the overall project. If the uncertainties weren’t

overcome, explain what happened.

Remember that the commercial failure of the product

or project does not mean that R&D was not present.

And if the scientific uncertainties weren’t overcome,

that can still mean that the work to address the

uncertainties can be R&D.

4. Why wasn’t the knowledge being sought readily

deducible by competent professionals?

Explain the uncertainty in the context of the known

state of the field of research

It might be publicly known that others have tried to

resolve the uncertainties and failed. Or maybe others

have resolved the uncertainties, but precisely how it

was done isn’t in the public domain. In either case a valid

technological uncertainty can still exist.

What if there’s limited available information about the

state of the field of research?

If there’s little public information available about the

project, you’ll need to show that the people leading

it are competent professionals working in the relevant

field. This might be done by outlining their relevant

background, professional qualifications and recent

experience and then have them explain why they

consider the uncertainties are scientific or technological

uncertainties rather than routine uncertainties.

Whichever is appropriate, set out the details and have

evidence available if needed.

14 Research and development tax relief: Making R&D easier for small companies

The start and end of a project

for R&D tax purposes

It’s important to know when an R&D

project starts and ends, because that

makes sure your company claims the

right amount of relief.

When a project starts

The project starts when work to resolve the uncertainty

starts. This is when you have identified the technical

issues that need to be resolved, and the current state

of knowledge within that field of science or technology

has not provided a solution to those uncertainties.

When a project ends

A project ends when that uncertainty is resolved or

the work to resolve it ceases. This is when you have a

working prototype or material device/product or process

ready to be tested or go into production, or if you decide

not to take the project forward.

R&D can take place even after production starts

If any new problems arise involving scientific or

technological uncertainty after the product has been

put into production or into use then the R&D process

may start again. There is a distinction between

such problems involving science and technological

uncertainties and routine fault fixing or design tweaks.

It is particularly important that the people doing the

work are involved when considering whether the project

is R&D for tax purposes as they are the ones who

understand best the scientific or technological problems

involved. They should focus on what advances the

project is seeking to achieve and the uncertainties to

be faced rather than on the eventual product aspiration,

specification or design.

15 Research and development tax relief: Making R&D easier for small companies

Possible commercial project timeline —

defining R&D for tax purposes

This illustrates the qualifying and non-qualifying

activities within a ‘whole life’ project plan.

The parts of a project that require R&D activity to

resolve scientific or technological uncertainties qualify

for tax relief. The qualifying work starts when work to

resolve the uncertainty starts, and ends when the new

knowledge is codified in a usable form, or when work

to resolve the uncertainty ceases.

Beginning End

RESOLUTION of scientific

or technological uncertainty

RESOLUTION of scientific

or technological uncertainty

Commercial/

scientific

Idea

Technological

or Scientific

Uncertainty

ascertained

Technological

or Scientific

Uncertainty

ascertained

Market/

feasibility

Research

Technological

or Scientific

Uncertainty

resolved or

work to resolve

it stops

Technological

or Scientific

Uncertainty

resolved or

work to resolve

it stops

Patents

or other

IP protection

sought

Pre-production

design

Industrial

upscaling

Patents

or other

IP protection

sought

Commercial

application

Prototypes Prototypes

Non-Qualifying Non-QualifyingNon-QualifyingQualifies Qualifies

Examples of how this may apply to some of the

industry sectors can be found on page 35 onwards.

16 Research and development tax relief: Making R&D easier for small companies

What costs qualify?

17 Research and development tax relief: Making R&D easier for small companies

What costs qualify?

Direct and externally provided staff,

subcontracted R&D, consumables,

software, trials, prototyping and

independent research costs may all

qualify for R&D relief. Capital expenditure

does not qualify under this scheme,

nor does expenditure on the production

and distribution of goods and services.

Direct R&D staff costs

Your company can claim for salaries, wages, class 1 NIC

and pension fund contributions for staff directly and

actively engaged in the R&D project.

This covers employees who undertake ‘hands on’ R&D

work and the proportion of supervisory and managerial

time spent specifically directing such employees in those

activities.

Support staff costs, for example administrative or

clerical staff, do not qualify, except when they relate to

qualifying indirect activities. These can be activities like

maintenance, clerical, administrative and security work.

A more detailed definition of support staff costs at:

hmrc.gov.uk/manuals/cirdmanual/CIRD81900.htm

Your company cannot claim for employment-related

benefits.

Externally provided R&D staff

These are the staff costs paid to an external agency for

staff who are directly and actively engaged in the R&D

project — these are not employees and subcontractors.

Relief is usually given on 65% of the payments made to

the staff provider. Special rules apply if the company and

staff provider are connected or elect to be connected.

Further information on externally provided R&D staff

can be found at: hmrc.gov.uk/manuals/cirdmanual/

cird84000.htm

18 Research and development tax relief: Making R&D easier for small companies

Subcontracted R&D

SME Scheme

Your company can generally claim for 65% of

the payments made to unconnected parties.

The subcontracted work may be further subcontracted

to any third party. Special rules apply where the parties

are connected or elect to be connected.

RDEC Scheme

R&D expenditure subcontracted to other persons is

generally not allowable unless it is directly undertaken

by a charity, higher education institute, scientific research

organisation or health service body — or by an individual

or a partnership of individuals.

Further information on SME/RDEC schemes can be found

at: hmrc.gov.uk/manuals/cirdmanual/cird84250.htm

Consumable items

Your company can claim for the cost of items that are

directly employed and consumed in qualifying R&D

projects. These include materials and the proportion

of water, fuel and power consumed in the R&D process.

From 1 April 2015, the costs of materials incorporated

in products that are sold are not eligible for relief.

Further information on consumable items can be found at:

hmrc.gov.uk/manuals/cird82300.htm

Software directly used in the R&D

Your company may claim for the cost of software that

is directly employed in the R&D activity. Where software

is only partly employed in direct R&D, an appropriate

apportionment should be made.

Further information on software directly used in the

R&D can be found at:

hmrc.gov.uk/manuals/cirdmanual/cird82500.htm

Clinical trial volunteers

Pharmaceutical companies and research organisations

often make payments to volunteers taking part in clinical

trials. These are allowable for relief, but read

the guidance first.

Further information on payments to volunteers taking

part in clinical trials can be found at:

hmrc.gov.uk/manuals/cirdmanual/cird84400.htm

Contributions to independent research

Only large companies may claim R&D relief on

contributions they make towards funding relevant

independent R&D. This R&D must be carried out by

the recipient and be related to the company’s trade.

Contributions must be made to a qualifying body —

a charity, higher education institute, scientific research

organisation or health service body — or to an individual

or a partnership of individuals.

Further information on contributions to independent

research can be found at:

hmrc.gov.uk/manuals/cirdmanual/cird82200.htm

hmrc.gov.uk/manuals/cirdmanual/cird82250.htm

Prototypes

Where a prototype is created to test the R&D being

undertaken, the design, construction and testing costs

will normally be qualifying expenses.

However, if the prototype is also built with a view to

selling the prototype itself (such as the construction

of a bespoke machine), HMRC considers that to be

production and outside the R&D scheme, even if R&D

was undertaken to create the prototype.

In that case you need to work out the split between

R&D expenditure and production costs. For example,

the construction costs and materials consumed would

not be qualifying expenses, but design, modelling and

testing costs could still qualify.

Collaborative working

In general, where two companies collaborate on a R&D

project, each can claim relief on the qualifying costs they

have incurred.

Where a company and a university or other research

institute collaborate, only the company can claim relief

on the qualifying costs it has incurred.

Collaborative arrangements are governed by their

contracts and you should seek advice from HMRC

where it’s unclear which company gets the relief.

19 Research and development tax relief: Making R&D easier for small companies

What costs do not qualify

Not all costs qualify, and you cannot receive R&D

relief for:

• The production and distribution of goods and services

• Capital expenditure under either of the R&D relief

schemes. However, a generous 100% Research and

Development Allowance may be due on capital assets,

such as plant, machinery and buildings used for R&D

activity.

Further information on capital assets used for R&D

activity can be found at: gov.uk/hmrc-internal-

manuals/capital-allowances-manual/ca60000

• The cost of land

• Payments for the use and creation of patents and

trademarks, as these are the cost of protecting the

completed R&D. This also includes the staff costs

in relation to the time spent by all staff on the

preparation and submission of such applications.

However, the Patent Box enables companies to apply

a 10 per cent rate of Corporation tax to profits earned

from their patented inventions after 1 April 2013.

Further information on Patent Box be found at:

gov.uk/guidance/corporation-tax-the-patent-box

20 Research and development tax relief: Making R&D easier for small companies

Subcontracted R&D

21 Research and development tax relief: Making R&D easier for small companies

Subcontracted R&D

SMEs that subcontract qualifying R&D

activities can claim tax relief on 65%

of the payment to the subcontractor.

SMEs undertaking qualifying R&D for

large companies may claim under the

RDEC Scheme.

Your company as the contractor

Under the SME Scheme the subcontractor does not

need to be a UK resident and there is no requirement

for the subcontracted R&D to be performed in the UK.

There are special rules where the parties are connected

or elect to be connected. The diagrams below help

explain what you may claim.

Further information and guidance on connected

and unconnected companies can be found at:

gov.uk/hmrc-internal-manuals/corporate-intangibles-

research-and-development-manual/cird91000

Your company as the

subcontractor

Generally, if an SME or large company carries out an

R&D project under contract to a large company or

person not chargeable to tax in the UK as a trade,

profession or vocation, they are likely to be able to

make a claim under the RDEC scheme.

Further information and guidance on your company

as the subcontractor can be found at:

hmrc.gov.uk/manuals/cirdmanual/cird81470.htm

Unconnected Subcontractors

SME

Scheme

Company can

claim 65% of

the qualifying

R&D payment

made to a

subcontractor

RDEC

scheme

Generally the

expenditure

contracted to

other persons is

not allowable

However

100% of the R&D

expenditure can

qualify if the

subcontractor falls

within Note 1

Connected Subcontractors

SME

Scheme

The lesser of

100% of the R&D

payment made to

the subcontractor

or the relevant

expendature in

the connected

party’s accounts

See

Note 2

RDEC

scheme

Generally the

expenditure

contracted to

other persons is

not allowable

However

100% of the R&D

expenditure can

qualify if the

subcontractor falls

within Note 1

Note 1:

An individual, a partnership

made up wholly of individuals,

or a qualifying body. Further

information can be found at:

hmrc.gov.uk/manuals/

cirdmanual/cird82250.htm

Note 2:

Definitive rules can be found at:

hmrc.gov.uk/manuals/

cirdmanual/cird84200.htm

22 Research and development tax relief: Making R&D easier for small companies

Subcontracting —

who can make a claim?

Contracting company Relief Subcontractor Relief

SME Yes SME No

SME Yes Large company No

SME Yes

Qualifying body, individual or

partnership

No

Large company No

SME (even if the SME further

subcontracts to qualifying body

individual or partnership)

Yes (under RDEC scheme)

Large company No Large company Yes

Large company Yes

Qualifying body, individual or

partnership

No

Large company No Another group company Yes

23 Research and development tax relief: Making R&D easier for small companies

Grants and subsidies

Grants or subsidies that your company

receives for your R&D project may make

a difference to your R&D claim.

The SME scheme is a notifiable State Aid, and a company

can’t get the SME relief if is receiving any other notifiable

State Aids for the same R&D project.

So if you are thinking of claiming for a project that has

already received a grant, it is essential that you establish

whether that grant was a notifiable State Aid. The grant

provider will be able to tell you that.

If you have received a grant which is notifiable State Aid,

for an R&D project, you can’t get relief under the SME

scheme, but eligible expenditure will qualify under the

RDEC scheme.

You don’t need to reduce the RDEC eligible expenditure

by the value of the grant received.

If the company has a number of projects it may

make RDEC claims for projects that have had State Aid,

and SME claims for non-grant funded project(s).

24 Research and development tax relief: Making R&D easier for small companies

More on grants and subsidies

You may have received a grant which

is not a notifiable State Aid — examples

include de minimis State Aid, Horizon

2020 or Framework Programme funding.

If you have received a grant which is not a notifiable

State Aid, or have received any other type of subsidy for

one of your R&D projects, you may be eligible to claim

under both the RDEC and the SME scheme.

You can claim under the RDEC scheme for eligible

expenditure which has been subsidised by the grant or

subsidy. In addition, if there is eligible expenditure on

the project which has not been covered by the subsidy,

you can make a claim for the balance of the expenditure

under the SME scheme.

Example

Expenditure on project:

£125,000 — staff and consumables

Amount of grant received:

£80,000 — potentially eligible for RDEC claim

Balance of expenditure:

£45,000 — potentially eligible for SME Claim

25 Research and development tax relief: Making R&D easier for small companies

Why is RDEC important to SMEs?

SMEs may also claim relief under the

RDEC scheme if they cannot claim under

the SME scheme because of a grant or

subsidy, or because they are carrying out

subcontract R&D for a large company.

SME worked example

Profit and Loss

Account (£)

Sales

1,000

Cost of sales (500)

Gross profit 500

R&D qualifying expenditure (100)

Other expenses (150)

Total operating costs (250)

Net profit before tax 250

Tax due (see below)

24

Total tax 24

Profit after tax

226

Corporation Tax

Computation (£)

Net profit before tax

250

Less R&D relief (130%) (130)

Adjusted profit before tax 120

Corporation Tax due at 20%

24

Corporation Tax

payable (£)

Corporation Tax 24

RDEC worked example

Profit and Loss

Account (£)

Sales 1,000

Cost of sales (500)

Gross profit 500

R&D qualifying expenditure (100)

11% RDEC on expenditure 11

Other expenses (150)

Total operating costs (239)

Net profit before tax 261

Tax due at 20% 52.2

Total tax 52.2

Profit after tax

208.8

Corporation Tax

Computation (£)

Net profit before tax

261

Corporation Tax due at 20%

52.2

Tax payable (£)

Corporation Tax due 52.2

Less tax credit (11)

Corporation Tax payable 41.20

26 Research and development tax relief: Making R&D easier for small companies

How to claim R&D relief

27 Research and development tax relief: Making R&D easier for small companies

How to claim R&D tax relief

Making a claim

CT600

You can claim R&D relief by entering the total qualifying

expenditure on the full Company Tax Return form,

CT600.

Payable Tax Credit

Under the SME scheme, SMEs that prepare their accounts

on a going concern basis may be able to claim a payable

tax credit - up to 14.5% of the R&D loss surrendered from

1 April 2014.

Backdated claims

If your company has been undertaking qualifying R&D

and has not yet claimed R&D relief, you may make a

backdated claim within the anniversary of your filing

date — generally two years after the end of the

accounting period.

28 Research and development tax relief: Making R&D easier for small companies

How to calculate your claim

There are three stages to making your

claim. Using an example, we explain

how to take your figures and turn them

into a claim.

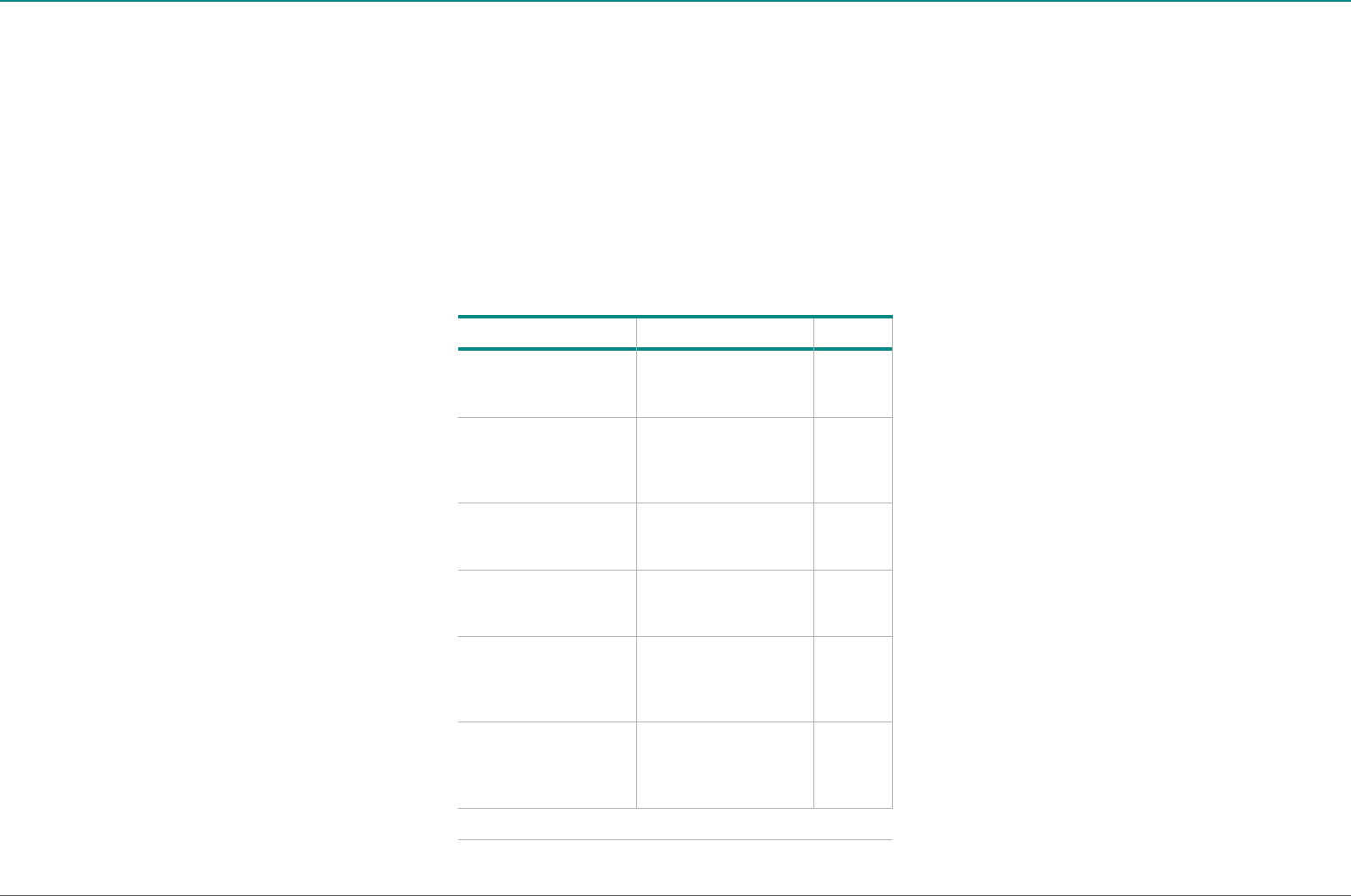

1. Work out your allowable

expenditure

Your total costs What is allowable Total

R&D staff (x3) with total

costs £150,000 and 80%

time directly on R&D.

£150,000 x 80% allowable

as staff costs

£120,000

R&D manager’s costs

£100,000 with 20% of

time directly managing

the R&D activity.

£100,000 x 20% allowable

as staff costs

£20,000

Heat and light £5,000

with 25% consumed in

R&D project

£5,000 x 25% allowable

as consumable items

£1,250

Disposable laboratory

equipment consumed

£200

£200 allowable as

consumable items

£200

£80,000 payments

to an unconnected

subcontractor for R&D

work

£80,000 x 65% of

payments allowable as

subcontracted R&D

£52,000

£70,000 payments to

an unconnected staff

provider for staff directly

engaged on R&D.

£70,000 x 65% allowable

as an externally provided

worker (EPW).

£45,500

£238,950

In this example, we’ve worked out that the total

qualifying expenditure is £238,950.

The next thing to do is to turn this into a figure for

the amount of R&D tax relief that the company wants

to claim.

29 Research and development tax relief: Making R&D easier for small companies

2. Turn the allowable

expenditure into an

R&D tax relief figure

Total allowable costs £238,950

Multiply by 130% £310,635

Add these together to get the total R&D tax relief:

‘enhanced expenditure’

£549,585

3. Put the R&D tax relief into

the right box on the company

tax return

Now that we have worked out the R&D tax relief, this can

be entered onto the company tax return

For accounting periods that start on or after 1 April

2015, use version 3 of the company tax return. Version 2

is for periods before this. The two versions have different

box numbers, so we provide guidance on both. Check the

front page of the tax return to see which version you are

using.

Using version 3 of the company tax return

Put an X in the box at box 650.

Enter the enhanced expenditure figure in box 660

— in this example you would enter £549,585.

30 Research and development tax relief: Making R&D easier for small companies

Using version 2 of the company tax return

Put an X in the box at box 99.

Enter the enhanced expenditure figure in box 101

— in this example you would enter £549,585.

Claiming the payable tax credit?

If your company wants to claim a payable tax credit,

there are a couple more steps to carry out before you

fill in the tax return.

First you need to know how much tax you are due to

pay in this period.

Second, you need to calculate the amount of the

payable tax credit. In the simplest cases, this figure will

be (‘enhanced expenditure’ x payable tax credit rate).

Using 2016 rates and the example above, the payable

tax credit will be:

£549,585 x 14.5% = £79,690.

Guidance on how to calculate the amount of the payable

tax credit can be found at: gov.uk/hmrc-internal-manuals/

corporate-intangibles-research-and-development-

manual/cird90500

Now you are ready to enter the figures.

Using version 3 of the company tax return

Enter the company’s Self Assessment figure in box 525.

Enter the tax credit figure in box 530 — in this example

you would enter £79,690.

Complete box 545 — in this example, you would enter

£79,690.

Complete box 570 — that’s box 545 minus box 525.

Put an X in the box at box 650.

Enter the enhanced expenditure figure in box 660

— in this example you would enter £549,585.

Enter the payable tax credit figure at box 875 — in this

example, you would enter £79,690.

Using version 2 of the company tax return

You need to complete boxes 86, 87, 89, 99, 101 and 143.

Claiming the RDEC?

Using version 3 of the company tax return.

You need to calculate the expenditure credit due to the

company. Using 2016 rate, and for this example, it would

be £238,950 x 11% = £26,285.

Enter the expenditure credit figure at box 530 — in this

case, it is £26,285.

Complete box 570.

Check box 650, and for box 660 enter £549,585.

Complete box 880 — in this case it will be £26,285.

31 Research and development tax relief: Making R&D easier for small companies

Keeping records

There is no additional record keeping

requirement specifically for the purposes

of claiming R&D relief.

You should be able to give a summary of the R&D

project undertaken and explain how the project is R&D

within the tax relief definition. It would be helpful if you

provide this information in a short report at the time of

making your claim.

Focus on the advances being sought and the

uncertainties faced rather than just a description of

the finished product. Include a breakdown of the

expenses that qualify for relief.

32 Research and development tax relief: Making R&D easier for small companies

Advance Assurance

33 Research and development tax relief: Making R&D easier for small companies

Advance Assurance

In November 2015, HMRC introduced

Advance Assurance for companies that

claim R&D tax relief in November 2015.

If your company carries out R&D for itself or other

companies, it could qualify for Advance Assurance.

This means that for the first three accounting periods

of claiming for R&D tax relief, HMRC will allow the claim

without further enquiries.

Applying for Advance Assurance is voluntary and you

can do this at any time before the first claim for R&D

tax relief. Your company can still apply for R&D tax relief

without Advance Assurance.

Further information, help and advice can be found at:

gov.uk/guidance/research-and-development-tax-relief-

advance-assurance

34 Research and development tax relief: Making R&D easier for small companies

Case Studies

35 Research and development tax relief: Making R&D easier for small companies

The Agri-food Sector

The Agri-food sector is increasingly

exploiting new science and technology.

A project to develop a new feed or to grow crops that

have substantially increased vitamin content, produce

better or more reliable yields, or are more tolerant to

weather conditions and resistant to blight, would be

qualifying R&D.

The scientific and technological advance is in resolving

the uncertainty in the creation of a new improved strain.

However, work to protect this new strain with plant

breeding rights does not qualify as it is regulatory,

not scientific or technological activity.

Not every change advances overall knowledge and

capability. Creating new Vitamin C rich confectionery

simply by adding Vitamin C to the ingredients does

not qualify. A competent professional could carry out

the process without uncertainty in either combining the

ingredients or their reaction in the body when consumed.

Creating an innovative chilled food container

that provides a substantially longer shelf life than

currently available, would also qualify. The scientific

or technological uncertainties to be addressed are in the

interactions between the food, gas content and container

to keep the food fresh for longer. By contrast, the work

in dealing with authorities to comply with extended

use-by date regulation would not qualify.

Not all innovation qualifies. A project to create a food

container where the innovation lies in the artistic

design or presentation of the packaging to encourage

prospective customer purchases would not qualify.

The uncertainty here is in design or marketing, not

in science or technology.

36 Research and development tax relief: Making R&D easier for small companies

ICT

The computer games industry provides

particularly good examples of innovative

projects that do meet the requirements

of the R&D schemes and also examples

of projects which do not.

No matter how original and inventive the game

storylines are, these are not scientific or technological

advances. The important criterion is not ‘what’ is

produced but ‘how’.

A company realised that each object on a game’s screen

had to be programmed in respect of its interaction

with all the other objects. As the game became more

complex, more objects were introduced and the amount

of code required rose exponentially. The solution was

to programme the properties of each object. When

the objects interacted, a separate code was no longer

required as the inherent properties produced the

outcomes. The qualifying expenditure on developing this

innovative code qualified for R&D relief.

The ICT sector is so fast-moving that further advances

overtake new and ground breaking developments very

quickly. What is important is that a project represents

an advance at the time of development.

New encryption and security techniques are being

developed regularly and in many cases give rise to

further advances. Even if the technique is quickly

rendered redundant it will probably qualify for relief.

The same applies to new search engines using new

search methods.

Many advances are in the software field but advances

in hardware are not unusual and will qualify for R&D

relief if they are designed to overcome a scientific or

technological uncertainty. Equally, very small companies

dealing in subcontracted work may qualify if the work

undertaken is sufficiently innovative, even if the larger

contractor’s project does not qualify.

37 Research and development tax relief: Making R&D easier for small companies

Advanced materials

Whilst some companies specialise in the

design and production of new materials,

other companies find they become

involved in this area as an adjunct

to their main activities.

A company, specialising in agricultural engineering,

used a probe to provide information on the quality of

cereals which were transported in sacking. Measurements

could only be taken at the top, as anywhere else would

damage the sacking. This however did not produce

representative samples.

The company designed a material which allowed a

probe to enter the sacking and which reverted to

a sealed surface once the probe was removed.

Although the market for this material was limited,

it proved extremely successful in overseas markets.

For R&D purposes the company incurred qualifying

expenditure in overcoming the uncertainty in

developing the material.

A further development arose when the company

received orders from Eastern European countries,

where the material did not react in the required way

in sub-zero temperatures. The company undertook

further research to amend the material to meet the

requirements of the extreme conditions. The additional

expenditure on manufacturing the material was not

qualifying but the research costs of amending the

material to meet ‘cold weather’ issues again qualified.

In many projects involving advanced materials, the

scientific and/or technological uncertainty can be readily

identified. However, the use of ‘new’ materials in existing

processes may also qualify if it can be shown that the

outcome has or was intended to significantly improve

efficiency, for example, significantly reduce waste.

38 Research and development tax relief: Making R&D easier for small companies

Advanced engineering

R&D is increasingly providing an

important competitive edge in this sector.

A project is commissioned to produce a prototype

(not to be sold) that will test a design for a new

eco-petrol engine and exhaust. The goal is to achieve

a substantial reduction in eco-unfriendly emissions with

a performance at least as good as a comparable engine.

This appears to competent professional engineers to

offer hope of achieving a real advance by way of an

improvement in vehicle technology. The uncertainty

in science and technology is whether this substantial

reduction with the comparable performance sought is

possible. Even if unsuccessful, this and the construction

of the prototype is still a qualifying R&D project.

On the other hand, an innovative in-bus eco-waste bin,

where the innovation is in the attractive and appealing

presentation of different compartments designed

specifically to encourage the usage and promotion of

recycling, does not qualify. The uncertainty of persuading

people to put their litter in the bin is in the field of social

science, not in the field of technology. The technology

required would be obvious to a competent engineer.

A project for a new standard bus engine which is

substantially lighter, cheaper, or faster to produce

than any currently available or known to be possible

(for example patented), whilst maintaining performance

levels (for example in power, robustness and life) can all

qualify as R&D. However, a minor and routine adjustment

such as one to incorporate slightly better spark plugs,

already designed and used in another vehicle, would

not qualify.

39 Research and development tax relief: Making R&D easier for small companies

Life and health sciences

The creation of new drugs is an obvious

example of qualifying R&D in this sector.

Creating a new drug, up to and including Phase III trials,

to more effectively and safely reduce the risk of a stroke,

is a qualifying project. The salaries of both the scientists

and their laboratory assistants doing this hands-on R&D

can qualify. However, their work to achieve important

regulatory FDA approvals does not qualify, because any

uncertainty in achieving these is in regulation,

not science or technology.

A project to create a new artificial bladder system for

patients with urinary difficulties, substantially more

comfortable, safe and leak-proof than any other

designed, qualifies as R&D. The advance sought and

uncertainty addressed is how to bio-engineer the

materials to achieve these qualities, enabling safe

insertion and avoiding rejection.

However, where a competitor reverse-engineers this

product, for markets not covered by any intellectual

property protection, this does not qualify. The advance

in science or technology worldwide has already been

overcome and the competitor’s uncertainty is not an

uncertainty at industry sector level, rather an uncertainty

in their own state of knowledge.

A project for newly-diagnosed diabetes patients to

provide details of their blood sugar to the hospital via

a simple internet web form is innovative. It allows the

hospital to monitor their condition in real time and

advise the patient immediately on how best to manage

their condition.

Although this achieves an advance in patient care,

any uncertainty associated with the patient’s use of

the software is not an uncertainty in the technology

itself. As such, this is not a qualifying R&D project.

The design of the web-based system would be obvious

to a competent professional.

40 Research and development tax relief: Making R&D easier for small companies

Construction

In general, this is a traditional and

well-proven industry. However an

increasing number of companies

undertake R&D to exceed the traditional

methods in terms of life expectancy of

buildings, durability or robustness.

A company created a cladding system which had the

appearance of ‘normal’ brickwork but incorporated the

capacity for off-site fabrication, improved fire protection

and suitability to fast-track production. Mechanical fixing

rather than wet mortar provided strength and durability,

which together with the capacity to construct in all

weather conditions provided significant cost savings.

The uncertainty of the materials in the cladding system

and the technological uncertainties surrounding fixing

were qualifying R&D projects.

Another company specialised in constructing laboratories.

To combat contamination the company designed some

new buildings with removable sections. Exterior walls

could be slid away and a unit could be removed in total

and replaced by a new unit before the exterior walls

were slid back into place.

The technological uncertainties surrounding the

mechanisms to achieve this had to be overcome

before the concept proved viable, making this a

qualifying project.

A further example of innovation is a company which

used wood in part of a project. Traditionally the wood

needed to be of a certain age but the company was able

to modify a coating so that younger and cheaper wood

could be used whilst still having the required qualities.

Significantly this development was a small element of

an overall conventional project. Only after discussion

with the site foreman did the company directors realise

that the modification and application of the coating

qualified for R&D relief.

41 Research and development tax relief: Making R&D easier for small companies

Further help

Further information on about Research and Development

relief can be found at: gov.uk/guidance/corporation-tax-

research-and-development-rd-relief

Further information on Advance Assurance can be

found at: gov.uk/government/publications/research-

and-development-tax-relief-application-for-advance-

assurance-for-research-and-development-tax-relief-ct-

rd-aa

Department for Business, Energy and Industrial Strategy

(BEIS) guidelines can be found at:

gov.uk/hmrc-internal-manuals/corporate-intangibles-

research-and-development-manual

42 Research and development tax relief: Making R&D easier for small companies

Frequently asked questions

Can I claim R&D relief and a grant?

Yes, however the EU notification status of the grant

will affect under which R&D scheme you can claim.

Most grants are ‘notifiable’ therefore both SMEs and

large companies can claim under the Large Company

Scheme or the RDEC scheme on the gross qualifying

expenditure.

How do I know if a grant is notified?

Your grant provider will be able to tell you whether

or not the grant/subsidy is notified.

Can I claim patent costs?

The costs of preparing and registering a patent are not

R&D — they are the costs of protecting the completed

R&D. However, the Patent Box enables companies to

apply a 10% rate of Corporation Tax to profits from its

patented inventions after 1 April 2013.

Further information on claiming patent costs can be

found at: gov.uk/corporation-tax-the-patent-box

What is the difference between a subcontractor

and an externally provided worker?

A subcontractor is a person paid by the R&D company to

carry out a specific R&D activity. An externally provided

worker is an individual who provides or is under an

obligation to provide their services personally to the

R&D company under the terms of a contract between

them and the staff provider. The individual will be paid

by the staff provider but work under the R&D company’s

direction. The company pays the staff provider.

How do I treat R&D losses?

Under the SME scheme, for expenditure incurred on

or after 1 April 2014, the company may surrender the

R&D loss for a payable tax credit of 14.5% (previously

11% from 1 April 2012). Any unsurrendered or unutilised

losses under either the SME or RDEC schemes may be

carried forward to be set against future years trading

profits under the normal corporation tax rules.

How long will it take to receive an R&D tax credit

repayment?

HMRC aims to deal with 95% of payable tax credit claims

within 28 days of receiving the claim.

43 Research and development tax relief: Making R&D easier for small companies

Glossary

Appreciable improvement — to change or adapt the

scientific or technological characteristics of something

to the point where it is ‘better’ than the original. The

improvement should be more than minor or routine

upgrading and should represent something that would

generally be acknowledged by a competent professional

in that field as a genuine and non-trivial improvement.

Appropriate proportion — the expenditure claimed

by the company for R&D must be representative of

the amount of time spent carrying out qualifying R&D

activity. The company must be able to demonstrate that

costs have been calculated to remove any elements that

were not incurred during the R&D process.

Competent professional — an expert working within

the field of science or technology in which the advance

is being sought.

Consumable items — Where R&D activity results in

items being wholly used up or transformed within the

process these are consumable items and may be eligible

for relief. However, from expenditure incurred on or after

1 April 2015 where those items are incorporated into the

final product and sold then the costs of those items will

not be eligible for relief.

Corporation Tax — A limited company must pay

Corporation Tax on profits from doing business, however

the amount of Corporation Tax you pay may be reduced

if you are undertaking relevant R&D activity.

Externally provided workers (EPW) — Workers are

provided through a staff provider. The staff provider is

required to operate PAYE in relation to individual workers

supplied to a client.

The conditions to be satisfied can be found at:

gov.uk/hmrc-internal-manuals/corporate-intangibles-

research-and-development-manual/cird84100

Filing date — The date by which a company has to

submit its tax return to HMRC. The date will be shown

on the notice issued to the company. Any amendment to

a tax return must be submitted no later than 12 months

after the filing date.

Notifiable State Aid — State Aid is granted by public

authorities through state resources to provide assistance

to an organisation. Many companies receive State Aid as

a contribution towards their research and development

activity. If your company receives State Aid then HMRC

needs to know as it can affect the amount you can claim

in R&D tax relief. Your grant notification documents will

say it the grant is notifiable State Aid or not.

Prototype — An original model constructed to include

all the technical or scientific characteristics of the new

product or process determined by the R&D undertaken

within a project.

44 Research and development tax relief: Making R&D easier for small companies

R&D — Research and Development for tax purposes

takes place when a project seeks to achieve an advance

in science or technology. The work is undertaken on a

systematic basis in order to resolve technical or scientific

uncertainty and aims to advance the level of knowledge

in a particular field of science beyond the level known

before the research and development took place.

R&D project — The R&D project is not the project

to develop the product. See paragraph 19 of the

Department for Business, Energy and Industrial

Strategy (BEIS) guidelines (formerly Business Innovation

and Skills {BIS}) which defines the “project” for R&D

purposes. We very often see claims stating that the

advance is the creation of a project which does x, y,

or z (and where the claim is based on the costs of

creating that product).

That is not the correct test. The specific advances in

science and technology with that (commercial) project

must be identified. Each such specific advance will be

a separate R&D project. Only the costs of resolving the

scientific or technological uncertainties linked to each

of those advances will qualify.

RDEC — Research and Development Expenditure Credit.

A stand-alone credit to be brought into account as a

receipt in calculating the profits of large companies for

research and development expenditure incurred on or

after 1 April 2013. Companies with no corporation tax

liability will benefit from RDEC either through a cash

payment or a reduction of tax or other duties due.

Readily deducible — Where the knowledge or capability

is publicly available or known by competent professionals

working in the field.

Science — Science is the systematic study of the nature

and behaviour of the physical and material universe.

Work in the arts, humanities and social sciences, including

economics, is not science for the purpose of these

guidelines. Mathematical techniques are frequently

used in science but mathematical advances in and of

themselves are not science unless they are advances in

representing the nature and behaviour of the physical

and material universe.

SME — A small or medium sized enterprise.

SME scheme — You can only claim under the scheme

for SMEs if your company meets the definition of a SME

for R&D tax relief purposes. You can only claim R&D tax

relief as a SME if your company is a going concern and

not in administration or liquidation when you make your

claim. If you’ve made a claim and the company then

ceases to be a going concern you can’t get a tax credit.

Technology — Technology is the practical application

of scientific principles and knowledge, where ‘scientific’

is based on the definition of science above.

Webinar — HMRC have a number of seminars and

presentations which take place on the internet. You can

register your interest to view these on the HMRC website.

Issued by

HM Revenue & Customs

November 2016 © Crown Copyright 2016