Reverse mortgages

A discussion guide

Consumer Financial

Protection Bureau

1

About this discussion guide

This guide gives an overview of many key concepts of reverse

mortgages. A qualied reverse mortgage counselor can help you

learn more.

If you’re interested in considering a reverse mortgage, but haven’t spoken

with a counselor yet, call (800) 569-4287 to nd a U.S. Department of Housing

and Urban Development (HUD), hud.gov approved reverse mortgage

counselor today.

A detailed discussion with a counselor will give you important information

to help you decide whether a reverse mortgage is right for you. HUD-

approved reverse mortgage counselors have the latest information on reverse

mortgages. In order to get the most out of your counseling session, come

prepared to talk about:

§ Your nancial needs and goals

§ Your spouse or partner’s future housing and nancial needs

§ Other family members or dependents living with you and their future

housing needs

§ The reasons you’re considering a reverse mortgage

§ The alternatives to a reverse mortgage you may have considered

Alert

Most reverse mortgages today are called Home Equity Conversion

Mortgages (HECMs). HECMs are federally insured by the Federal

Housing Administration (FHA). This guide covers typical features

and requirements for HECM reverse mortgages. Non-HECM reverse

mortgages may have different requirements and features.

REVERSE MORTGAGES: A DISCUSSION GUIDE2

How is a reverse mortgage different from

a traditional mortgage?

Traditional mortgages

With a traditional mortgage, you usually borrow money to pay for the home at

the time of the purchase, and pay it back over time. With each payment, you

build your equity and your loan balance goes down.

Equity

Debt

Home price Loan and

down

payment

Plus monthly

payment

Plus monthly

payment

Increases

equity

3

Reverse mortgages

With a reverse mortgage, you borrow money using your home as a guarantee

for the loan, as you would for a traditional mortgage. Unlike a traditional

mortgage, a reverse mortgage is repaid when the borrowers no longer live

in the home. Although you won’t make monthly mortgage payments, you’ll

need to continue to pay property taxes and homeowners insurance, and keep

your house in good condition. Because interest and fees are added to the loan

balance each month, your loan balance goes up—not down—over time. As your

loan balance increases, your home equity decreases.

Reverse mortgage borrowers must be age 62 or older. Borrowers usually use

the loan to help pay for living expenses.

Home equity Reverse

mortgage

loan

Monthly

interest and

fees

Monthly

interest and

fees

Increases debt

Equity

Debt

Alert

A reverse mortgage is not free money. It is a loan that you, or your heirs,

will eventually have to pay back, usually by selling your home.

Borrowed money + interest + fees each month = rising loan balance.

4

How does a reverse mortgage work if I still have a

traditional mortgage?

Many people interested in a reverse mortgage still owe money on their home. If

this is your situation, you will be trading one loan for another, usually a larger one.

Some of the money you borrow with the reverse mortgage will be used to pay off

your current mortgage. If you owe a lot on your current mortgage, you may not

have much money from the reverse mortgage left over to spend on other things.

However, a reverse mortgage will free up money you have been using to make

monthly mortgage payments.

Existing

mortgage

New reverse

mortgage

loan

Monthly

interest and

fees

Monthly

interest and

fees

Equity

Debt

Alert

If you still owe a lot of money on your existing mortgage, you might not

have enough equity to pay off your current mortgage with a reverse

mortgage—which means you may not be able to get a reverse mortgage.

5

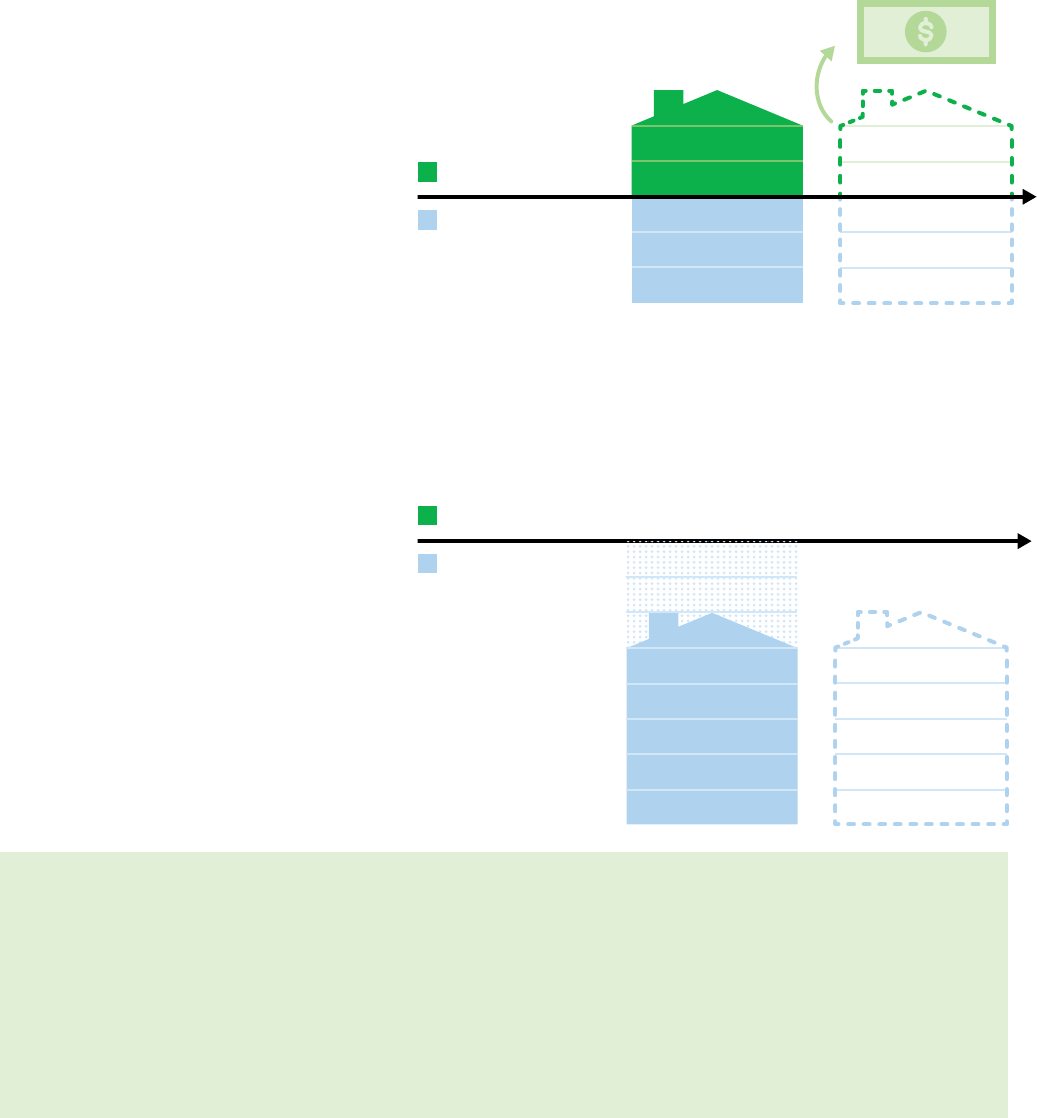

What happens if I want to sell my home?

You might decide to sell your home while you have a reverse mortgage. You

may want to downsize, or move closer to family.

With a reverse mortgage, the money you borrow and the interest and fees

added to the loan balance shrink your equity. However, if home prices rise, you

might gain back some equity. It’s hard to predict how much, if any, equity will

be left when you sell your home.

What if my reverse mortgage balance is less than my home value?

So long as your reverse mortgage loan balance is less than the value of your

home, this works just like selling your house when you have a traditional mortgage:

Reverse

mortgage

loan

Monthly interest

and fees

Monthly interest

and fees

Sell home

to pay loan

and keep

difference

Equity

Debt

Alert

Home price increases are not guaranteed! During the housing crisis

between 2007 and 2012, home prices fell more than 25 percent overall,

and more than 50 percent in some areas.

6

What if I owe more on my reverse mortgage than my home is worth?

If your loan balance is more than the value of your home, you may not have to pay

the difference. When you sell your home for the appraised fair market value, the

remaining balance of the loan is paid by mortgage insurance.

Reverse

mortgage

loan

Interest and

fees are added

to the loan each

month

Your loan

balance is more

than the value

of your home

Sell home for

appraised

value to pay

part of the

loan

Remaining

balance is

paid for by

mortgage

insurance

Equity

Debt

Caution

If you don’t meet your responsibilities with a reverse mortgage (see

pages 16-18), your loan could become due for repayment. In this case,

you will usually have to sell your home for the lesser of the loan balance

or 95 percent of its appraised value.

7

What happens to my home when I pass away?

When the last remaining

borrower passes away, the

loan has to be repaid. Most

heirs will repay the loan by

selling the home.

How does it work when

the loan balance is less

than the home value?

Your heirs will use the loan

proceeds to repay the loan

and keep the difference.

How does it work when

the loan balance is more

than the home value?

Your heirs won’t have to

pay more than 95 percent

of the appraised value. The

remaining balance of the

loan is covered by mortgage

insurance.

Inherit home

worth more

than the loan

balance

Sell home

to pay loan

and keep

difference

Equity

Debt

Equity

Debt

Inherit home

worth less than

loan balance

Sell home for

95 percent

of appraised

value

Caution

If you plan to leave your home to heirs, talk to them about their repayment

options. If your heirs want to keep the home, they will have to repay either

the full loan balance or 95 percent of the home’s appraised value—whichever

is less.

8

How much can I borrow?

Your “principal limit”

Your borrowing limit is called the "principal limit." It takes into account your age,

the interest rate on your loan, and the value of your home. In general, loans

with older borrowers, higher-priced homes, and lower interest rates will have

higher principal limits than loans with younger borrowers, lower-priced homes,

and higher interest rates.

Principal limit

Equity

Debt

Lower borrowing limit

§ Younger borrowers

§ Lower-valued homes

§ Higher interest rates

Higher borrowing limit

§ Older borrowers

§ Higher-valued homes

§ Lower interest rates

Question

Whose age is used if I am married or have a co-borrower?

If you are married or co-borrowing with another person, the

principal limit is based on the age of the youngest co-borrower,

or Eligible Non-Borrowing Spouse.

9

What is a credit line growth feature?

Growing credit line

With the credit line growth feature, the less credit you use today, the more

you'll have available for the future. Whatever you don't use in your credit line

will keep growing, allowing you to borrow up to a maximum amount stated in

your mortgage.

The amount of credit line growth is based on the interest rate and mortgage

insurance premium. A credit line growth feature does not apply to the xed

rate payment option.

Example 2: Leaving credit available means your

borrowing limit will actually grow over time,

helping you keep pace with rising expenses

Example 1: If you max out

your credit up front, you

won't be able to borrow

more in the future

10

Principal limit

Equity

Money you'll receive

Upfront costs

How much will it cost?

Reverse mortgages can be expensive. Like traditional mortgage loans, you

will owe not just the money you borrow, but also interest and fees. Unlike

traditional mortgage loans, the amount you owe grows over time.

Upfront costs

Like traditional mortgages, borrowers typically pay some one-time upfront

costs at the beginning of the loan. While you can pay these costs out of pocket,

you can typically choose to pay for them using your loan proceeds. This means

that you don’t have to bring money to the closing. But it’ll reduce the total

amount of money you get to use for other things.

Upfront costs include origination fees paid to the lender, real estate closing

costs paid to third-party professionals, and the initial mortgage insurance

premium paid to the FHA.

11

Ongoing costs

Ongoing costs include interest, mortgage insurance premiums (MIP) and

servicing fees. These costs are charged each month. Interest and the MIP are

calculated as a percentage of your outstanding loan balance.

Ongoing costs are

added to your loan

balance each month.

These costs compound,

meaning each month you are

charged interest and fees

on the interest and fees that

were added to your previous

month’s loan balance.

Month 5

Loan balance

Interest + fees

Month 1 Month 2 Month 3 Month 4

Tip and question

§ The best way to keep your ongoing costs low is to borrow only as

much money as you need.

§ What is mortgage insurance and why do I have to pay for it?

If you or your heirs sell your home to pay off a reverse mortgage,

your loan balance may be more than your home is worth. Mortgage

insurance covers the remaining loan balance so you won’t owe more

than your home is worth. It also protects you in case your lender has

nancial difculty and can’t make payouts to you as agreed. Borrowers

pay for mortgage insurance as a requirement of a HECM loan.

12

How do I receive my money?

You have three main options for receiving your money:

Line of credit (adjustable interest rate)

§ Higher mortgage insurance costs if you withdraw more than 60 percent in

the rst year.

§ Lower cost: pay interest and fees only on the money you’re ready to use.

§ Credit line growth feature*: unused credit continues to grow.

§ Can be combined with monthly payout.

Monthly payout (adjustable interest rate)

§ Higher mortgage insurance costs if you withdraw more than 60 percent in

the rst year

§ Get a set monthly payout to supplement income.

§ Two choices: Term (xed monthly payouts for a set number of years) or

Tenure (xed monthly payouts as long as you maintain the reverse mortgage).

§ Lower cost: pay interest and fees only on the money you’ve drawn so far.

§ Credit line growth feature is factored into monthly payout amount.*

§ Can be combined with a line of credit.

Lump sum (xed interest rate)

§ Withdraw all available funds at once. Amount available is usually lower

compared to other options.

§ Higher cost: pay interest and fees on entire loan amount.

§ No credit line growth feature.*

§ Higher risk for younger borrowers of outliving their loan funds.

*See page 9 for information on the credit line growth feature.

13

How can a reverse mortgage affect the people living

with me?

Do you live with a spouse

or partner?

It is a good idea to make

your spouse or partner a

co-borrower.

When your spouse or partner

is a co-borrower, you are both

responsible for the loan and

both receive benets from

the reverse mortgage.

§ When your spouse or

partner is a co-borrower,

they will be able to remain

in the home after you no

longer live in the home.

§ A co-borrower will also

continue to receive benets

from the reverse mortgage

after you no longer live in

the home.

You and a co-borrower

may live in your

home with a

reverse mortgage

When you pass away or

move, the co-borrower

may remain in the

home and continue to

receive money from the

reverse mortgage

14

What if your spouse isn’t a co-borrower on the reverse mortgage?

§ Only co-borrowers and some non-borrowing spouses have the right to remain

in the home after you pass away.

§ If your spouse is not on the reverse mortgage, but was married to you at the

time you took out the reverse mortgage, they may be able to remain in the

home after you move into a health care facility or pass away, if they qualify

under HUD's rules.

§ From the time you get a reverse mortgage, your non-borrowing spouse must

continue to live in the house as their principal (meaning primary) residence.

§ If you get married after you already have a reverse mortgage, your spouse can’t

stay in the home when you pass away unless they are your heir and are able to

pay off your loan.

§ Non-borrowing spouses do not receive money from a reverse mortgage after

the borrower dies.

Anyone may live with

you in your home with

a reverse mortgage

When you die or move

into a healthcare facility

for 12+ consecutive

months, your non-

borrowing spouse will

not receive loan money

and may have to move

out if they don't meet

certain requirements

Non-eligible spouses

will need to make other

living arrangements

after you die

15

Do you live with someone age 62 or older who is not your spouse?

§ If this person wishes to remain in the home after you move or pass away,

consider making them a co-borrower.

§ If the person you live with isn’t a co-borrower, they will have to move out

when you move out or die, unless they are an heir and can either pay the

reverse mortgage debt or 95 percent of the appraised value with cash or a

new loan.

§ Make plans for the people you live with for where they will move after the last

borrower no longer lives in the home.

Anyone can live in

your home with you

when you have a

reverse mortgage

When the last co-borrower

or eligible spouse no longer

lives in the home, the loan

comes due for repayment

and others need to move out

16

What are my responsibilities?

There are several requirements that HECM reverse mortgage borrowers

must follow. If you don’t meet these requirements, you could lose your home

to foreclosure.

1. Property taxes and homeowners insurance must be paid on time.

With a reverse mortgage, the way you pay your property taxes and

homeowners insurance could change. A lender will do a nancial assessment

to determine your options for paying your property taxes and homeowners

insurance. Your options may include:

§ You make direct payments to the insurance company and tax authority.

§ You make direct payments, but have some of your loan set aside to help you

with these payments.

§ The lender takes care of it for you by using your loan proceeds in a

set-aside account.

Question

What is a “set-aside?”

A “set-aside” is a portion of your loan that is reserved to pay some

repairs, taxes, homeowners insurance, and fees. Set-asides help make

sure you’ll have the funds to make these payments in the future.

17

2. Your home must be kept in good repair.

You must make repairs as needed to keep your home well maintained. With a

reverse mortgage, your lender will let you know what repairs you may need to

make. Which situation applies to you?

Your current mortgage Reverse mortgage

repairs.

I routinely maintain my home and

make repairs, hiring professionals

when necessary.

That’s good. This is required with a

reverse mortgage.

My roof is missing a couple of shingles,

and my water heater is getting old.

These may not be emergency issues, but

they may require attention before they

become worse and cause damage to

your home.

My home is in good condition, but my

yard has become overgrown.

You will need to keep your entire

property maintained. A neglected yard

can eventually damage property.

My home needs major repairs. You may be required to make repairs

as a condition of getting a reverse

mortgage. Your lender may withhold

some of your loan proceeds to make the

required repairs.

Caution

Beware of scams! Beware of contractors who approach you about

getting a reverse mortgage to pay for repairs to your home. Learn

all your options. Do not let yourself be pressured into getting a

reverse mortgage.

18

3. Your home must be your primary residence.

Every calendar year, you will be required to certify in writing that you occupied

your home as your primary residence. Which situation applies to you?

Your current mortgage Reverse mortgage

hs.

I live in my home year-round. You are already meeting this

requirement.

I split my time between my home and

another location.

OK, but you can only get a reverse

mortgage on the home where you spend

the majority of the year. Let your lender

know if you are going to be away for

more than two months.

19

Have you explored other borrowing and housing options?

Homeowners interested in a reverse mortgage may nd that other loans or

housing choices are a better t for their nancial situation or personal needs.

Be sure to look at all of your borrowing and housing options before making

your nal decision. Consider alternatives to a reverse mortgage, such as:

Waiting

If you take out a reverse mortgage when you are too young, you may run out

of money when you’re older and more likely to have less income and higher

health care bills.

Other home equity options

A home equity loan or a home equity line of credit might be a cheaper way to

borrow cash against your equity. However, these loans carry their own risks and

usually have monthly payments. Qualifying for these loans also depends on

your income and credit.

Renancing

By renancing your current mortgage with a new traditional mortgage, you may be

able to lower your monthly mortgage payments. Pay attention to the term of your

new mortgage, as it can affect your retirement plan. For example, taking on a

new 30-year mortgage when you are nearing retirement can become a hardship

later. Consider choosing a shorter-term mortgage, such as 10 or 15 years.

Downsizing

Consider selling your home. Moving to a more affordable home may be your

best option to reduce your overall expenses.

Lowering your expenses

There are state and local programs that may provide assistance with utilities

and fuel payments as well as home repairs. Many communities also have

programs to help with property taxes: check with your county or town tax

ofce. Information about these and other benet programs is available through

the Administration for Community Living, acl.gov.

To learn more about reverse mortgages, visit consumernance.gov/

reversemortgage.

20

About the Consumer Financial

Protection Bureau (CFPB)

The Consumer Financial Protection Bureau (CFPB) is a 21st century

agency that helps consumer nance markets work by making rules

more effective, by consistently and fairly enforcing those rules,

and by empowering consumers to take more control over their

economic lives.

The CFPB Ofce for Older Americans develops initiatives, tools,

and resources to help protect older consumers from nancial

harm and help older consumers make sound nancial decisions

as they age.

For more information about the CFPB, visit consumernance.gov.

21