24 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

ABSTRACT

Spreadsheets are used in almost all businesses, for applications ranging from the mundane to the mission-

critical. Errors in the data, formulas, or manipulation of spreadsheets could be costly, even devastating. The

received wisdom is that about 5% of all formulas in spreadsheets contain errors, and this rate is consistent

across spreadsheets. However, this estimate is based on ve studies, some of which are quite informal, and

a total of only 43 spreadsheets. Our research was designed to deepen our understanding of spreadsheet

errors. Specically, we address three questions about errors in operational spreadsheets: what is the aver-

age cell error rate, how does it differ among spreadsheets, and what types of errors are most prevalent? We

created a spreadsheet auditing protocol and applied it to 50 diverse operational spreadsheets. We found

errors in 0.9% to 1.8% of all formula cells, depending on how errors are dened. We also found that the

error rate differed widely from spreadsheet to spreadsheet. [Article copies are available for purchase from

InfoSci-on-Demand.com]

Keywords: please provide

INTRODUCTION

Errors in software have been a problem since the

beginning of the computer era. The discipline of

software engineering (Sommerville, 2004) was

created in part to develop methods to minimize

errors in software code. Professionally devel-

oped software is now generally created and

debugged using disciplined approaches from

software engineering.

The advent of the personal computer in

the 1980s increased by orders of magnitude

the number of people who worked closely with

computers. Just as professional programmers

were learning to use disciplined approaches to

programming, millions of so-called end-user

programmers began to create their own pro-

grams in the form of spreadsheets. One of the

appealing features of spreadsheet programming

on a personal computer is that the end user

can work independently of the constraints of a

professional programmer or an MIS group. This

allows the end user much more freedom and

speed in completing the business task at hand.

Errors in Operational

Spreadsheets

Stephen G. Powell, Dartmouth College, USA

Kenneth R. Baker, Dartmouth College, USA

Barry Lawson, Dartmouth College, USA

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 25

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

But very few end users have any training for

the programming tasks they attempt, and many

have little appreciation for the risks inherent in

a casual approach to programming.

As spreadsheets have spread throughout

business, they have increasingly been used

for mission-critical applications (Croll, 2005;

Grossman, Mehrotra, & Özluk, 2005). At the

same time, evidence has accumulated that many

spreadsheets have errors (Panko, 2005) and that

sometimes these errors cost the organizations

that use them millions of dollars (EUSPRIG,

n.d.). End users and organizations that rely on

spreadsheets generally do not fully recognize

the risks of spreadsheet errors. In fact, spread-

sheets tend to be somewhat invisible, both as

corporate assets and as sources of risk.

Although the received wisdom holds that

errors are prevalent in spreadsheets, our review

of the literature suggests that this conclusion

is based more on casual empiricism than solid

research. In fact, researchers have produced

only limited information on the types of er-

rors that occur, how frequently they occur on

average, and how the error rate varies from one

spreadsheet to another.

The current study was designed to im-

prove our understanding of spreadsheet errors

by testing a large sample of spreadsheets in

actual use by organizations. We developed a

detailed auditing protocol and trained a group

of researchers to apply it consistently. Using an

explicit protocol is important for two reasons:

(1) it allows other researchers to replicate and

improve on our work; and (2) it contributes to the

development of improved auditing procedures,

which is important in its own right. The audit-

ing procedure is described in detail in Powell,

Baker, and Lawson (2006b).

We begin this article with a summary of pre-

vious work on spreadsheet errors which comes

from eld audits and laboratory experiments.

Then we describe the design of our study and the

sample of spreadsheets we audited. Our results

are summarized in terms of error instances (the

occurrence of a single type of error) and error

cells (the number of cells affected by a single

error instance). We also categorize the errors

as to whether they generate wrong numerical

results. We report the total number of errors we

identied, as well as how they were distributed

across error types and across spreadsheets. This

is the rst data on errors and their distribution

to appear in the research literature that can be

replicated with parallel studies using similar

methods.

PREVIOUS WORK ON

SPREADSHEET ERRORS

Since our interest in this article is primarily

with the classication and frequency of errors,

we will discuss only those questions here. In a

related article (Powell, et al., 2006a), we pro-

vide a review of the literature on all aspects of

spreadsheet errors.

Types of Errors

Before we can productively study spreadsheet

errors, we need to dene and classify the types of

errors we seek. Classication is useful because it

helps us to understand what is common among

errors. It also allows us to compare different

studies of errors, and eventually to understand

the causes of errors and to develop cures.

At the outset, we make a distinction be-

tween errors in the use of a spreadsheet and

errors in the cells of the spreadsheet itself. A

spreadsheet can be perfectly correct but used

to solve the wrong problem, or its results could

be misinterpreted. More concretely, a correct

spreadsheet can lead to an error if sorting is

done improperly, or if formulas are overwritten,

or if incorrect data were entered temporarily.

All of these errors would be difcult or impos-

sible to detect purely from examination of the

spreadsheet itself.

Most classications of spreadsheet errors

have focused primarily on the spreadsheet itself,

not on errors in use. Because spreadsheets es-

sentially consist of data and formulas, an error

in the spreadsheet must arise from erroneous

data or erroneous formulas.

26 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

There is no generally accepted taxonomy

of spreadsheet errors, possibly because differ-

ent classications are appropriate for different

purposes. The rst researchers who studied

spreadsheet use simply listed examples of

errors without attempting to classify them.

Subsequent authors offered distinctions (but

not complete taxonomies), such as that between

domain errors (lack of knowledge of the ap-

plication area) and device errors (misuse of the

spreadsheet itself).

Panko and Halverson (1996) were the rst

to offer a real taxonomy of errors. They dis-

tinguished qualitative and quantitative errors,

and further decomposed quantitative errors

into mechanical, logic, and omission errors.

Quantitative errors lead to wrong numbers in

the current version of the spreadsheet. The three

types were dened as follows:

• Mechanical errors arise from typing or

pointing errors.

• Logic errors arise from choosing the wrong

function or creating the wrong formula.

• Omission errors arise from misinterpreta-

tion of the situation to be modeled.

Qualitative errors do not lead to wrong

numbers in the current version of the spread-

sheet, but are risky practices that could lead to

errors in subsequent use. This category includes

practices such as hard-coding numbers into

formulas. It can also include long formulas,

poor physical layout, or lack of sufcient

documentation.

Rajalingham, Chadwick, and Knight

(2000) and Purser and Chadwick (2006) have

developed the most elaborate taxonomy of errors

available to date (see Table 1). The rst distinc-

tion in this hierarchy is between application-

identied errors and developer/user-identied

errors. Excel has eight categories of errors

that it displays in a cell when it cannot resolve

a formula; these are application-identied

errors. The remaining errors are developer/

user-identied errors.

Although this taxonomy may be interesting

from a theoretical perspective, it has limitations

as a practical tool for auditing. First, its catego-

ries overlap. For example, an error caused by

lack of domain knowledge could occur during

insertion. Second, it may not be possible in

practice to determine the cause of an error and

A. Application-Identied Errors

B. Developer/User-Identied Errors

1. Qualitative Errors

A. Structural

a. Visible

b. Hidden

B. Temporal

2. Quantitative Errors

A. Reasoning

a. Domain Knowledge

1. Real-World Knowledge

2. Mathematical Representation

b. Implementation

1. Syntax

2. Logic

B. Accidental

a. Insertion

b. Update

1. Modication

2. Deletion

Table 1. Error taxonomy (Rajalingham et al., 2000; Purser & Chadwick, 2006)

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 27

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

therefore to properly categorize it. For example,

a complex formula giving wrong results could

be due to lack of domain knowledge, incorrect

syntax, or an accidental typing mistake.

Powell et al. (2006a) summarized the litera-

ture on classication of errors as follows:

• Classications are offered without specify-

ing the contexts or purposes for which the

classication is intended.

• The existing classications do not include

sufcient examples of specic errors that

satisfy each category.

• Classications are not rigorously tested

to demonstrate that multiple users can

consistently classify actual errors into the

proper categories.

• The boundary between quantitative errors

and qualitative errors remains vague.

• No studies compare the types of errors by

development stage.

Frequency of Errors

Research on the frequency of errors in spread-

sheets comes from a variety of sources, mostly

experiments in the laboratory. One approach is to

observe subjects as they build spreadsheets and

record the number of errors they make. Another

approach is to ask subjects to build a spread-

sheet from a written description and determine

the frequency of errors in the nished product.

However, the approach of most relevance to our

research is the eld audit, in which operational

spreadsheets are examined for errors.

Panko (2005) summarized the results of

seven eld audits in which operational spread-

sheets were examined, typically by an outsider

to the organization. His results show that 94%

of spreadsheets have errors and that the average

cell error rate (the ratio of cells with errors to

all cells with formulas) is 5.2%.

Table 2 summarizes the data behind these

estimates. In total, 88 spreadsheets are repre-

sented in the table. For all 88, the weighted

average percentage of spreadsheets with errors

is 94%. Data on cell error rates were available

on 43 of these spreadsheets, and the weighted

average for this sample is 5.2%.

There are several reasons to question the

reliability of these estimates. First, three of the

seven sources are unpublished (Hicks, 1995;

Lukasic, 1998; Butler, 1992). Second, the major-

ity of the sources gave little or no information

on their denition of errors or on the methods

used to nd errors. Third, Lawrence and Lee

(2004), whose observations account for 70%

of the sample used to estimate the cell error

*Weighted average of 88 spreadsheets in sources 1-7.

**Weighted average of 43 spreadsheets in sources 3-7.

Source

Number

Audited

Percent with

Errors

Cell Error Rate

(% of cells)

1. Coopers and Lybrand (1997) 23 91 N/A

2. KPMG (1998) 22 91 N/A

3. Hicks (1995) 1 100 1.2

4. Lukasic (1998) 2 100 2.2

5. Butler (2000) 7 86 0.4

6. Clermont (2002) 3 100 3.0

7. Lawrence and Lee (2004) 30 100 6.9

Average 94* 5.2**

Table 2. Spreadsheet error rates (Panko, 2005)

28 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

rate, did not actually report a cell error rate of

6.9% on completed spreadsheets. Rather, they

reported that auditors had “issues” concerning

6.9% of the cells on the initial review of mod-

els that they subsequently discussed with the

developers. The authors provided no details on

the denition of an “issue” or its relation to an

actual error. Moreover, the initial model version

that was reviewed was revised an average of six

times before the model was complete. Thus the

estimate of a 6.9% error rate applies only to is-

sues raised by auditors on initial model versions,

not to errors in completed spreadsheets. If, as

seems warranted, we exclude this study from

the calculation of the cell error rate, the average

cell error rate decreases from 5.2% to 1.3% on

a base of only 13 audited spreadsheets.

Our review of the literature on spreadsheet

errors draws attention to several shortcomings.

First, no generally accepted classication of

errors exists. Second, the classications that

do exist are of more theoretical than practical

value. Third, existing estimates of error rates

are based on extremely limited data. Fourth, no

studies of errors have fully revealed the sources

of spreadsheets tested, how errors were dened,

and the auditing methods that were used.

RESEARCH DESIGN

Our research into spreadsheet errors is predicat-

ed on several guiding principles or constraints.

First, our interest is in errors in completed,

operational spreadsheets, not errors made in

a laboratory setting or errors made during the

development of a spreadsheet. A second prin-

ciple is that we conduct the audit using only the

information in the spreadsheet itself, without

relying on the developer. A third principle is

that we use an explicit auditing protocol that

any moderately experienced user of Excel can

master.

These principles limit our study in certain

ways. When we work without access to the

spreadsheet developers, we are not able to check

our understanding of a model with an expert. In

practice, this means that at times we will accept a

suspicious formula as correct because we cannot

be sure that it is incorrect. It also means that we

cannot hope to uncover errors in formulating

the underlying problem or errors in interpret-

ing spreadsheet results. Detecting these types

of errors requires a much more time-intensive

longitudinal study of how spreadsheets are

used in the broader context of problem solving.

Offsetting these limitations is the fact that we

can audit a much larger volume of spreadsheets

using our protocol than otherwise.

Our procedures almost certainly lead to an

underestimate of the actual error rates in the

spreadsheets we audit. We may occasionally

classify a cell incorrectly as an error, but we

have been conservative in limiting our deni-

tion of errors to cells for which we can have

a high degree of condence that our judgment

is correct. On the other hand, there are entire

classes of errors that we cannot hope to iden-

tify with the procedures used in this study. For

example, most (but not all) errors in input data

are beyond our scope.

Sample Spreadsheets

Our sample of 50 spreadsheets came from a

wide variety of sources. Some were obtained

during site visits to companies. We carried

out site visits at two consulting companies, a

bank, a college, a large energy company, and

a state government agency. We also obtained

spreadsheets from a variety of organizations

through the alumni and faculty networks at

the Tuck School of Business. No single source

contributed more than ve spreadsheets to the

sample of 50 analyzed here.

We also obtained spreadsheets from vari-

ous Web sites. Several software companies post

spreadsheets on their Web site, either to illustrate

how to use their software or to showcase the

results that practitioners have had with their

software. The Web site of Decisioneering Inc.

(http://www.decisioneering.com), makers of the

Crystal Ball add-in for Excel, is typical. This

site lists hundreds of sample models used in

industries ranging from aerospace to utilities.

Each of these spreadsheets has been contributed

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 29

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

by a practitioner, and it can be assumed that these

spreadsheets are carefully engineered and tested

by the time they appear on the Web site.

Our search for sample spreadsheets was not

strictly random. We asked potential contribu-

tors to give us important spreadsheets that were

completed and had been in use for some time.

We eliminated any spreadsheet that contained

only data and no formulas. We also eliminated

spreadsheets that contained a very small number

of cells or that were too simple to warrant audit-

ing (using only a couple of SUM functions, for

example). We eliminated some spreadsheets that

involved broken links to other spreadsheets. We

also eliminated some that used complex macros.

Thus our sample is by design not representative

of the class of very small spreadsheets, which

we believe are very common in practice. It is

also not representative of the most elaborate

spreadsheets in use. (Grossman et al. [2005]

reported on some very large Excel models used

in critical applications.)

While our sample is not strictly random,

it is certainly representative of the general

population of spreadsheets (with the caveats

cited above). The sample includes spreadsheets

from many different types of organizations,

spreadsheets created by both novice and ex-

pert developers, and spreadsheets that span

a broad range from small and simple to large

and complex.

Auditing Software

When we began this research, we were aware of

the auditing and error checking tools available

in Excel, but we knew little about third-party

auditing software. As we learned more, we

realized that many auditing tools are available,

and some research suggests that appropriate

software can make auditing easier. Accordingly,

we decided to include a small number of audit-

ing tools in our protocol. From a list of roughly

50 such tools supplied by Roger Grinde of the

University of New Hampshire, we selected

10 to review in some detail. Eventually we

settled on two to use in our auditing protocol:

XL Analyst (http://www.codematic.net/default.

htm) and Spreadsheet Professional (http://www.

spreadsheetinnovations.com/).

XL Analyst is an Excel add-in that evaluates

28 aspects of a spreadsheet, from “Formulas

evaluating to an error” to “Use of SUMIF.”

Spreadsheet Professional is a collection of

tools for building, testing, analyzing, and using

spreadsheets. In our auditing protocol we made

use of two features of this tool: maps and calcu-

lation tests. The mapping tool creates a coded

version of each worksheet in a workbook. Each

non-blank cell is coded as a label, a number, or

a formula. It also shows which formulas have

been copied from an original formula. The

calculation test tool checks a workbook for 25

conditions such as “Blank cell referenced.” For

each of these categories it gives the number of

cells involved and their cell addresses.

Selection and Training of Auditors

Our spreadsheet auditors were undergradu-

ates, graduate students, or recent alumni from

business or engineering schools. All had sev-

eral years of experience with Excel, usually

in a business setting. None were professional

programmers or professional spreadsheet de-

velopers.

For an auditor, the rst step in training was

to study the auditing protocol, which describes

in detail the stages an audit goes through and

the data to be gathered at each stage. Then an

auditor was given two or three spreadsheets to

audit. The nished audited workbooks were then

reviewed by the researchers for adherence to

the auditing protocol and for the quality of the

audit. In total, auditor training took an average

of 10 hours.

Auditing Protocol

The auditing protocol we used in this research

is a highly detailed document that species

the steps to take in auditing a spreadsheet for

size, complexity, several types of qualitative

features, and errors. (A complete description

of the protocol is available at http://mba.tuck.

dartmouth.edu/spreadsheet/index.html.)

30 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

The auditing protocol involves the follow-

ing 11 steps:

1. Run the two software tools XLAnalyst and

Spreadsheet Professional.

2. Transfer selected results from the software

tools to a data record sheet.

3. Record the purpose of the workbook and

each worksheet.

4. Examine workbook for use of Excel func-

tions.

5. Review the results of XL Analyst and use

them to locate errors.

6. Review the Spreadsheet Professional maps

and use them to locate errors.

7. Review the Spreadsheet Professional

calculation tests and use them to locate

errors.

8. Review all formulas not already reviewed

for errors.

9. Conduct sensitivity analyses to uncover

errors.

10. Rate the workbook on various aspects

of spreadsheet design (e.g., use of mod-

ules).

11. Record the total time taken by the audit and

record comments on any special situations

encountered.

This particular sequence of steps evolved

over several months of testing. During this

time we trained auditors and tested the protocol

ourselves and through our assistants on dozens

of operational spreadsheets. More details on

the auditing protocol are available in Powell

et al. (2006b).

Error Taxonomy

One of the challenges of spreadsheet error re-

search is how to categorize errors. As we pointed

out earlier, many different error classications

have been offered. Most of these suffer from

the same aw: errors that arise from different

causes cannot be distinguished by an auditor.

For example, when we encounter an error in

a formula, we rarely can determine whether

the error was due to sloppy typing, lack of

domain knowledge, lack of Excel knowledge,

a subsequent user changing the formula, or

some other cause. We can, however, easily

detect some formulas that give the wrong result.

With somewhat more effort we can sometimes

identify formulas that would give a wrong

result with a different set of numerical inputs.

An example of the latter error is an IF formula

whose True condition is active in the current

version and is correct, but whose False condition

can be activated with a different set of inputs

and is incorrect. We can also identify many

practices that are likely to cause errors as the

spreadsheet is used or that simply will make it

harder than necessary to use the spreadsheet

productively. The most common of these poor

practices is placing numerical inputs directly

into formulas. Other poor practices include

limited or nonexistent documentation, dupli-

cation of inputs, illogical physical layout, and

so on. A fundamental question in spreadsheet

error research is where to draw the line between

errors and poor practices.

Initial Error Taxonomy

Recall that our study required our auditors to

detect errors in the spreadsheets themselves,

without access to external information or to the

spreadsheet developer. Thus the types of errors

we sought had to be observable by our audi-

tors. A second requirement for our taxonomy

was consistency: a single error must with high

probability be placed in the same category by

different auditors.

Our rst attempt to dene an operational

taxonomy used three categories:

1. wrong result with current inputs,

2. wrong result with different but allowable

inputs, and

3. poor practice.

After some experience with this clas-

sication, we discovered that the category of

poor practices was so ill-dened that no two

auditors could agree in specic instances. As

a result we eliminated this category from our

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 31

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

protocol. We also discovered that the second

category, wrong result with different inputs, was

ambiguous because it forced us to decide which

numerical inputs were allowable or plausible.

For example, most spreadsheets can be made

to generate errors with unlikely inputs, such as

text instead of numbers.

Interim Error Taxonomy

Eventually we settled on the following six error

types that our experience with auditing sug-

gested were well dened in theory and could be

identied with high reliability in practice:

1. Logic Errora formula is used incorrectly,

leading to an incorrect result.

2. Reference Errora formula contains one or

more incorrect references to other cells.

3. Placing Numbers in a Formulaone or

more numbers appear in formulas.

4. Copy/Paste Errora formula is wrong

due to inaccurate use of copy/paste.

5. Data Input Erroran incorrect data input

is used.

6. Omission Errora formula is wrong

because one or more of its input cells is

blank.

More details on this taxonomy, including

examples of situations in which a cell would or

would not be classied as an error, are available

in Powell et al. (2006b). Not surprisingly, we

found that we had to test our categorization

extensively before we could be condent that

our auditors could implement it effectively.

Even after auditing dozens of spreadsheets, we

found it necessary for the senior researchers

to review each audited workbook and to make

judgments as to which of the errors cited would

be included. (In the end, our overall inter-rater

reliability was on the order of 90%).

Our experience has been that errors come

in hundreds of subtle variations, many of which

do not t neatly into any classication scheme.

If nothing else, this suggests that we should

be skeptical of drawing rm conclusions from

previous studies of errors in which both the

errors themselves and the procedures used to

nd errors are not clearly spelled out.

Final Error Taxonomy

After completing our audits of 50 spread-

sheets using the taxonomy described above,

we returned to the question that motivated our

initial taxonomy: which of these errors actu-

ally give wrong results and which are merely

poor practices?

In order to investigate this distinction, we

reviewed all the instances of errors we found and

categorized each one as either a wrong result or

a poor practice. While this distinction may ap-

pear to be objective, there are many subtle cases

that require interpretation. For example, simply

embedding a number in a formula is usually a

poor practice, not a wrong result. However, we

encountered situations in which one number was

embedded in a formula and a related but different

number was included elsewhere among inputs.

For example, an input module might contain

the number 4% next to the heading “Ination,”

but the actual ination rate used in a formula

was 3.5%. We categorized this case as a wrong

result, even though the actual spreadsheet may

have been numerically correct. Again we stress

that determining whether a particular cell is an

error (or gives a wrong result) is not a purely

objective task.

ERRORS FOUND DURING

AUDITS

We audited 50 spreadsheet workbooks and in

three of them were unable to nd any errors

of the types included in our auditing protocol.

This implies a spreadsheet error rate of 94%,

which is identical to the spreadsheet error rate

estimated by Panko (2005).

In the remaining 47 spreadsheets, we found

a total of 483 instances of errors involving a

total of 4,855 error cells. (An error instance is a

single occurrence of one of the six errors in our

taxonomy. Typically a single instance involves

32 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

more than one cell.) Thus, on average each

error instance involved 10.05 error cells. The

average cell error rate over all 270,722 formulas

audited was 1.79%. This is considerably lower

than the 5.2% cell error rate cited by Panko

(2005), although somewhat higher than the

corrected estimate of 1.3% we derived earlier

from Panko’s data.

Table 3 shows how the error instances and

error cells were distributed by error type.

Hard-coding errors were the most common

(37.7% of instances and 43.5% of cells), fol-

lowed by reference errors (32.9% of instances

and 22.1% of cells) and logic errors (21.9% of

instances and 28.6% of cells). The remaining

three categoriescopy/paste, omission, and

data input errorstogether accounted for less

than 5% of instances and cells.

As explained earlier, not all of the 483 error

instances we identied involved wrong results.

In fact, roughly 40% of these were hard-coding

errors, in which a number was included in a

formula rather than a cell reference; most of

these did not produce wrong results. In order to

determine how many errors actually gave rise to

wrong results, we categorized each instance as a

wrong result or a poor practice. With this more

restrictive denition, we found that 7 of the 50

spreadsheet workbooks we audited were error-

free, for a spreadsheet error rate of 86%.

In the remaining 43 spreadsheets, we

found a total of 281 instances of wrong results

involving a total of 2,353 cells. Using this

denition, the average cell error rate over all

270,722 formulas audited was 0.87%. This is,

of course, substantially lower than the 1.79%

cell error rate we estimated using our more

inclusive denition of error, and much less than

Panko’s estimate of 5.2%.

Table 4 shows how wrong results break

down by type of error. Most, but not all, hard-

coding errors were categorized as poor practice.

Most, but not all, of the other error categories

were labeled wrong result. In total, 58% of

error instances and 48% of error cells were

categorized as wrong result.

Our results suggest that the average cell

error rate across all spreadsheets is in the range

of 1% when we use a restrictive denition and

2% when we use an inclusive denition. But

the average error rate does not tell us how

the error rate varies across spreadsheets. The

received wisdom is that errors are unavoidable

in spreadsheets, as they are in most facets of

life. In fact, Panko (2005) cites an error rate

of 5% as the norm for many different activi-

ties. This suggests that we should expect most

spreadsheets to have a cell error rate close to

the average.

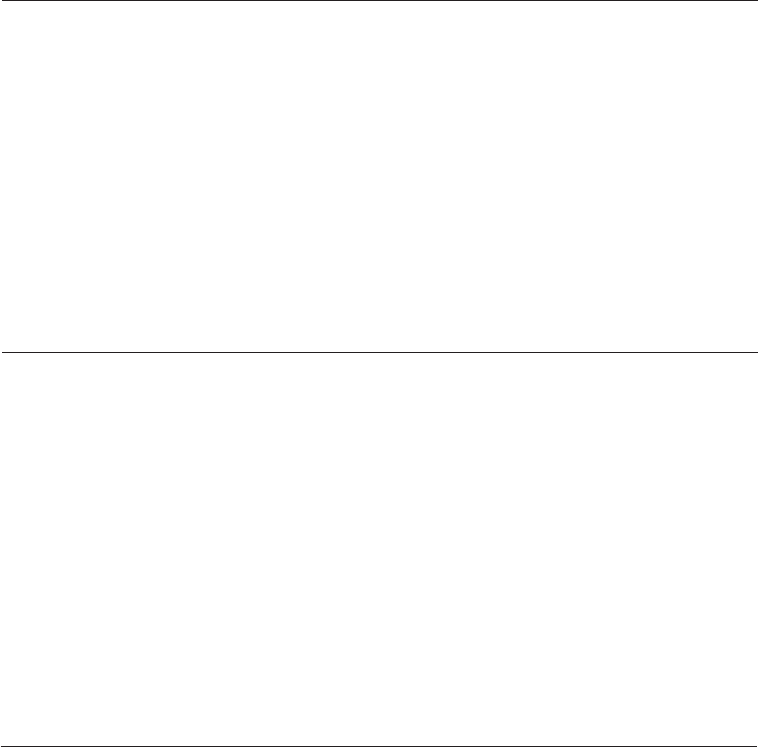

Figure 1 shows the distribution of cell error

rates using our original, inclusive denition.

Using that denition, 46% of our sample

spreadsheets had error rates below 2%; 70%

had error rates below 5%. However, several

spreadsheets had error rates above 10%; in fact

one had a cell error rate of 28%. Figure 2 shows

Error Type Instances Cells

Hard-Coding 182 (37.7% of total) 2,111 (43.5% of total)

Reference 159 (32.9%) 1,074 (22.1%)

Logic 106 (21.9%) 1,389 (28.6%)

Copy/Paste 17 (3.4%) 206 (4.2%)

Omission 13 (2.7%) 65 (1.3%)

Data Input 6 (1.2%) 10 (0.2%)

Total 483 4,855

Table 3. Errors categorized by type

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 33

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

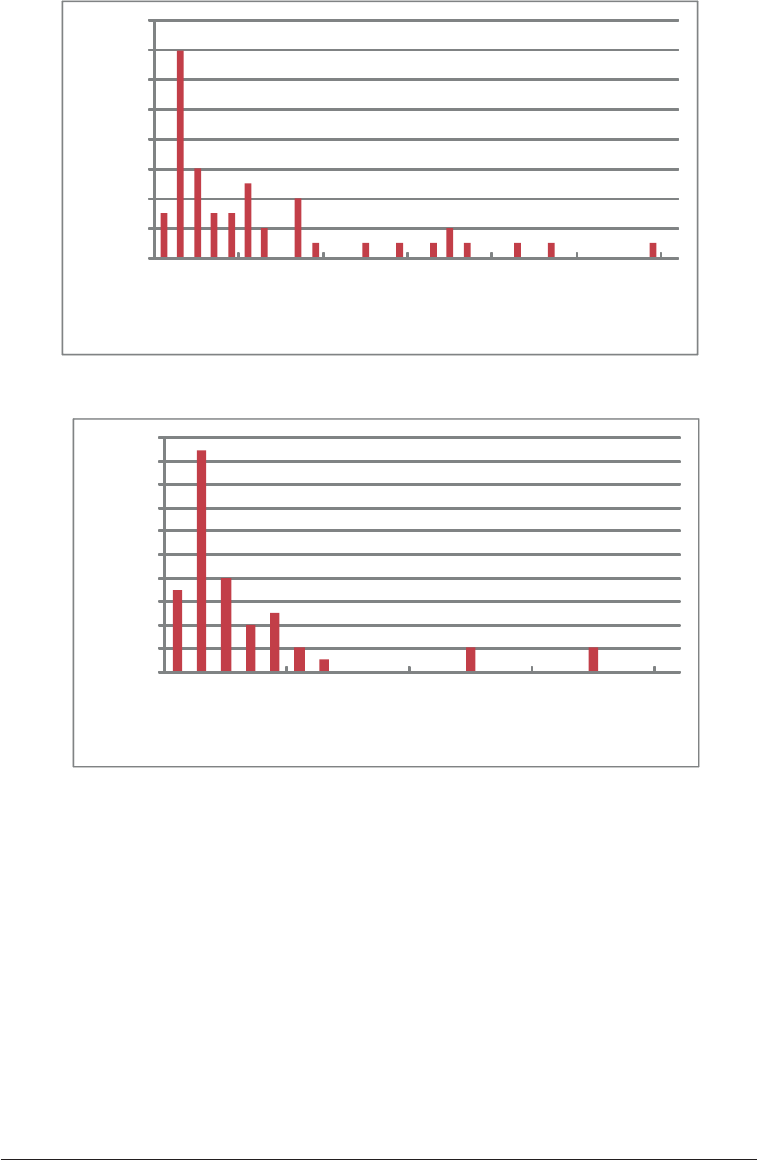

the distribution of cell error rates using the more

restrictive denition. In this case 68% had cell

error rates below 2% and 90% were below 5%.

The highest single error rate was 17%.

We began this article by noting that the

received wisdom on spreadsheet errors main-

tains that errors average 5% of cells and this

rate is consistent across spreadsheets. Our

results give a very different impression. The

average cell error rate appears to be closer to

1% or 2%, depending on how errors are dened.

Perhaps even more important, roughly half of

the spreadsheets we tested had rates below

these levels, although a few had astonishingly

high rates. These results suggest that errors are

not a constant factor, but presumably depend

on the situation being modeled and the devel-

oper’s skills. Finally, we document for the rst

time in the published literature the sources of

errors. Thirty to forty percent of errors are due

to embedding numbers in formulas. The next

most common error type is reference errors,

followed by logic errors. The remaining error

types are far less common.

SUMMARY AND DIRECTIONS

FOR FUTURE RESEARCH

We have audited 50 operational spreadsheet

workbooks and discovered 483 error instances

involving 1.79% of all formulas. This study is

unique in several ways. First, this is the larg-

est published sample of spreadsheets that has

been audited for errors. In fact, our sample of

50 operational spreadsheets exceeds the total

number of spreadsheets (43) cited in Panko’s

(2005) meta-study to estimate cell error rates.

Second, we have been explicit about our deni-

tion of errors. Our work in this area has shown

that errors manifest themselves in a wide variety

of guises, so estimated cell error rates may be

highly sensitive to how one denes errors. In

Instances

Error Type Wrong Results Poor Practices

Hard-Coding 31 (11.0% of total) 151 (74.8% of total)

Reference 137 (48.8%) 22 (10.9%)

Logic 89 (31.7%) 17 (8.4%)

Copy/Paste 14 (5.0%) 3 (1.5%)

Omission 7 (2.5%) 6 (3.0%)

Data Input 3 (1.1%) 3 (1.5%)

Totals 281 202

Cells

Error Type Wrong Results Poor Practices

Hard-Coding 191 (8.1% of total) 1,920 (76.7% of total)

Reference 857 (36.4%) 217 (8.7%)

Logic 1,073 (45.6%) 316 (12.6%)

Copy/Paste 203 (8.6%) 3 (0.1%)

Omission 26 (1.1%) 39 (1.6%)

Data Input 3 (0.1%) 7 (0.3%)

Totals 2,353 2,502

Table 4. Wrong results and poor practices

34 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

fact, our own estimates range from 0.87 to

1.79% of cells, depending on the denition

of error. Finally, the method we used to detect

errors is fully documented and available to

other researchers. In most previous studies

the methods used to search for errors were

not documented at all; in others only a brief

summary of the methods is offered. Our study

involves an explicit, detailed auditing protocol.

It also used two types of auditing software to

assist in the search for errors.

Our results conrm the general belief

among those who have studied spreadsheets

that errors are commonplace. The specic

estimates we have made are somewhat lower

than what has become received wisdom, but

we note that previous studies of spreadsheet

errors cannot easily be compared since they

use different (and generally undocumented)

auditing methods and denitions of errors. We

now have sound evidence for the hypothesis

that around 1% of all formulas in operational

spreadsheets are in error.

Figure 1. Distribution of cell error rates across spreadsheets

Figure 2. Distribution of cell error rates across spreadsheets (wrong results)

0

2

4

6

8

10

12

14

16

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

Number of Spreadsheets

Cell Error Rate

0

2

4

6

8

10

12

14

16

18

20

0.00% 5.00% 10.00% 15.00% 20.00%

Number of Spreadsheets

Cell Error Rate -Wrong Results

Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009 35

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

Obtaining reliable estimates of cell error

rates is only a rst step toward understanding

the fundamental question of the impact that

spreadsheets have on the quality of decision

making in organizations. Errors in formulas

should be avoided, of course, but by themselves

they do not necessarily translate into signicant

errors in the outcomes of spreadsheet use. The

next step we envision in this line of research

is to estimate the numerical impact of errors in

spreadsheets. This investigation would require

working closely with the developers of the

spreadsheet to determine which outputs are

most important and to determine the impact on

those outputs of correcting errors.

Errors in spreadsheet data and formulas

are not the only possible causes of errors in

spreadsheet use. In fact, many of the press ac-

counts reported by EUSPRIG involve misuse of

spreadsheets. For example, spreadsheet results

can be sorted incorrectly, or an out-of-date ver-

sion of a spreadsheet may be used. More gener-

ally, poor decisions based on spreadsheet models

can arise by modeling the wrong problem or by

misinterpreting the results. These types of errors

cannot be identied by auditing the data and

formulas of the spreadsheet itself. To determine

how frequent and damaging these types of errors

are to decision making would involve a kind

of ethnographic research, in which spreadsheet

users were closely observed in their natural

surroundings over months or years.

Finally, very little research (and none

outside the laboratory) has been conducted to

identify methods for avoiding or mitigating the

impacts of errors in operational spreadsheets.

One promising approach would be to audit a

sample of spreadsheets from different organiza-

tions and attempt to correlate error rates with

corporate or individual practices around spread-

sheet use. Many practitioners have offered

advice on what constitutes good spreadsheet

practice, but there is no scientic evidence from

the eld yet to back up these claims.

ACNOWLEDGMENT

This work was performed under the sponsor-

ship of the U.S. Department of Commerce,

National Institute of Standards and Technology.

Reproduction of this article, with the customary

credit to the source, is permitted.

REFERENCES

Butler, R.J. (1992). Personal communication to

Ray Panko.

Clermont, J.M. (2002). A spreadsheet auditing tool

evaluated in an industrial context. Proceedings of the

European Spreadsheet Risk Interest Group Annual

Conference, Cardiff, Wales.

Coopers and Lybrand. (1997). Retrieved from http://

www.planningobjects.com/jungle1.htm

Croll, G.J. (2005). The importance and criticality

of spreadsheets in the city of London. Proceedings

of the European Spreadsheet Risks Interest Group

Conference, Greenwich, UK.

EUSPRIG. (n.d.). European Spreadsheet Risks

Interest Group stories. Retrieved from http://www.

eusprig.org/stories.htm

Grossman, T.G., Mehrotra, V., & Özluk, Ö. (2005).

Spreadsheet information systems are essential to

business. Working paper, University of San Fran-

cisco, USA.

Hicks, L. (1995). Personal communication to Ray

Panko.

KPMG. (1998). Supporting the decision makera

guide to the value of business modeling. Retrieved

from http://www.kpmg.co.uk/uk/services/manage/

press/970605.html

Lawrence, R.J., & Lee, J. (2004). Financial modelling

of project nancing transactions. Institute of Actuar-

ies of Australia Financial Services Forum, 19.

Lukasik, T. (1998). Personal communication to

Ray Panko.

Panko, R. (2005). What we know about spreadsheet

errors. Retrieved September 2, 2006, from http://

panko.cba.hawaii.edu/ssr/Mypapers/whatknow.

htm

36 Journal of Organizational and End User Computing, 21(3), 24-36, July-September 2009

Copyright © 2009, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global

is prohibited.

Panko, R., & Halverson, R. (1996). Spreadsheets

on trial: A survey of research on spreadsheet risks.

Proceedings of the 29th Annual Hawaii International

Conference on Systems Sciences (pp. 326-335).

Powell, S., Baker, K., & Lawson, B. (2006a). A criti-

cal review of the literature on spreadsheet errors.

Spreadsheet Engineering Research Project working

paper, Dartmouth College, USA.

Powell, S., Baker, K., & Lawson, B. (2006b). An

auditing protocol for spreadsheet models. Spread-

sheet Engineering Research Project working paper,

Dartmouth College, USA.

Purser, M., & Chadwick, D. (2006). Does an

awareness of differing types of spreadsheet errors

aid end-users in identifying spreadsheet errors?

Proceedings of the European Spreadsheet Risk

Interest Group Annual Conference (pp. 185-204),

Cambridge, UK.

Rajalingham, K., Chadwick, D., & Knight, B. (2000).

Classication of spreadsheet errors. Proceedings of

the European Spreadsheet Risks Interest Group An-

nual Conference (pp. 23-34), Greenwich, England.

Sommerville, K. (2004). Software engineering (7

th

ed.). Boston: Addison-Wesley.

Steve Powell is a Professor at the Tuck School of Business at Dartmouth. His primary research interest lies

in modeling production and services processes, but he has also been active in research in energy econom-

ics, marketing, and operations. At Tuck, he has developed a variety of courses in management science,

including the core Decision Science course and electives in the Art of Modeling, Business Process Redesign,

and Applications of Simulation. He originated the Teacher's Forum column in Interfaces, and has written

a number of articles on teaching modeling to practitioners. He is the academic director of the INFORMS

Annual Teaching of Management Science Workshop. In 2001 he was awarded the INFORMS Prize for the

Teaching of Operations Research/Management Science Practice. He is the co-author with Kenneth Baker

of The Art of Modeling with Spreadsheets (Wiley, 2004).

Ken Baker is a faculty member at Dartmouth College. He is currently Nathaniel Leverone Professor of

Management at the Tuck School of Business and also adjunct professor at the Thayer School of Engineer-

ing. At Dartmouth, he has taught courses relating to decision science, manufacturing management, and

environmental management. Over the years, much of his teaching and research has dealt with production

planning and control, and he is widely known for his textbook Elements of Sequencing and Scheduling, in

addition to a variety of technical articles. He has served as the Tuck School's associate dean and directed

the Tuck School's management development programs in the manufacturing area. In 2001 he was named a

Fellow of INFORMS's Manufacturing and Service Operations Management (MSOM) Society, and in 2004

a Fellow of INFORMS. He is the co-author with Stephen Powell of The Art of Modeling with Spreadsheets

(Wiley, 2004).

Barry Lawson is a research associate at the Tuck School of Business at Dartmouth and is also a visiting

scholar in the geography department of the college. He founded and has served as president of Barry Lawson

Associates, a consulting rm, since 1978. As visiting scholar, he coordinates the development of an atlas

of the upper Connecticut River Watershed in New Hampshire and Vermont. As research associate at Tuck

he serves as the program manager for the Tuck Spreadsheet Engineering Research Project. Lawson has

taught in graduate programs at Boston University and Wayne State University as well as in short courses

at Bentley College. He has moderated a host of public hearings for local, state and federal governments

on controversial environmental and energy- and waste-related projects, and has considerable experience

in group facilitation, conict resolution and simulation design.